Fresh audio product: what made the GOP what it is today?

Just added to my radio archive (click on date for link):

November 20, 2025 Paul Heideman, author of Rogue Elephant, on how the Republican party went from a staid vehicle of American business to the frothy lunacy of today

Fresh audio product: Sudan, Japan

Just added to my radio archive (click on date for link):

November 13, 2025 Mosaab Baba, author of this article, on what’s behind the horrendous civil war in Sudan • Jake Adelstein, an American journalist who’s been living in Japan for almost 40 years, on that country’s reactionary new Prime Minister

Fresh audio product: tech moves right, South American politics

Just added to my radio archive (click on date for link):

October 30, 2025 Jacob Silverman, author of Gilded Rage, on the rightward move of the Silicon Valley elite • Forrest Hylton conducts a political tour d’horizon of South America

Fresh audio product: the Zoomer tech bros, the new arms merchants

Just added to my radio archive (click on date for link):

October 23, 2025 Margaux MacColl, co-author of a series of articles in the SF Standard, on the Zoomer tech bros • Susannah Glickman on the new arms makers who want to disrupt the legacy prime contractors (NYRB article here)

Fresh audio product

Just added to my radio archive (click on date for link):

October 16, 2025 Ilan Pappé, author of Israel on the Brink, on the ceasefire and how the deepening crisis of Israeli society could lead to something better • Jennifer Berkshire on the appalling Trump educational agenda

Fresh audio product: China, Chairman Bill

Just added to my radio archive (click on date for link):

October 9, 2025 Jake Werner on Trump’s creeping softness on China, and how that country sees its role in the world • Jeet Heer, author of this review, on the slick but odious William F. Buckley Jr.

Fresh audio product: public monuments, Trump’s Gaza scheme, Mamdani’s run for NYC mayor

Just added to my radio archive (click on date for link):

October 2, 2025 Erin Thompson on the politics of public monuments as Trump talks of restoring Confederate statues • Mouin Rabbani returns for a look at Trump’s dubious Gaza peace scheme • Ted Hamm, author of Run Zohran Run!, on Mamdani’s campaign for NYC mayor

fresh audio product: recognizing Palestine, bailing out Milei

Just added to my radio archive (click on date for link):

September 25, 2025 Mouin Rabbani explains what behind all these fresh diplomatic recognitions of Palestine and speculates on the future of Gaza • Ernesto Semán on the Argentine situation, and the US bailout of the libertarian Javier Milei (see NYRB article here)

Fresh audio product: neoliberalism, eugenics branch • stablecoins, and the Trump/UAE deal

Just added to my radio archive (click on date for link):

September 18, 2025 Quinn Slobodian, author of Hayek’s Bastards, on the eugenics/race science tendencies within High Church Neoliberalism • Molly White on stablecoins, and the Trump–UAE deal

Fresh audio product: transhumanism, fiscal politics

Just added to my radio archive (click on date for link):

September 11, 2025 Émile Torres on the tech moguls’ dream of transcending the merely human (article written with Timnit Gebru here) • Daniel Wortel-London, author of The Menace of Prosperity, on the fiscal history of NYC, and how we could do better than subsidizing the rich

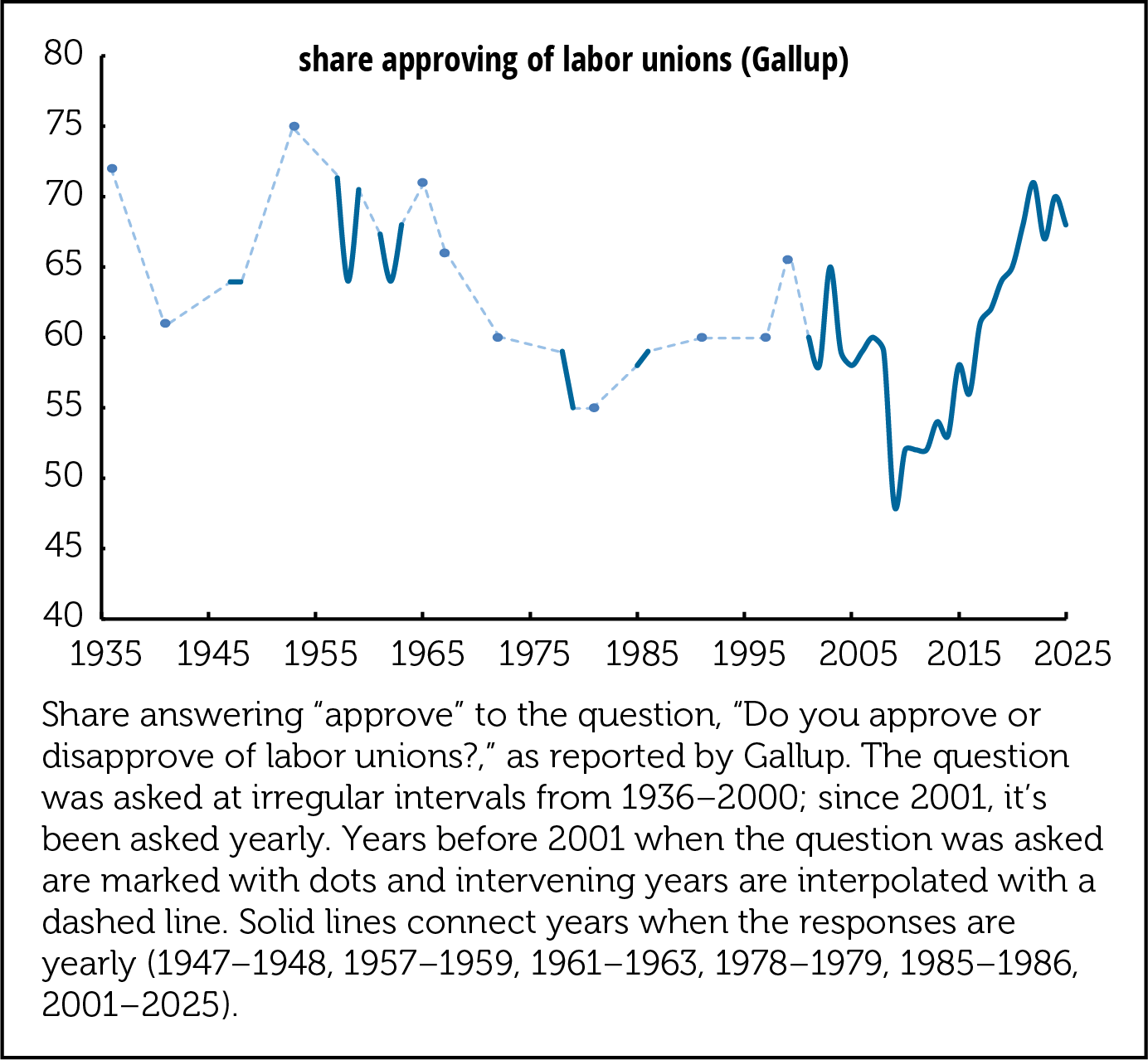

Union approval near 60-year high

To observe Labor Day—the holiday invented by conservative politicians and their friends in the labor movement to draw attention away from the militant history of May Day—Gallup released a poll on public attitudes towards unions.* For the fifth consecutive year, it shows approval close to the highest levels in 60 years—68%. It’s ranged between 68% and 71% since 2021. The graph below tells the history.

When Gallup first asked the question in 1936±the year of the Flint sit-down strike—72% approved. Positive feelings sagged some during the 1940s, but rose back above 70% in the 1950s and stayed close to that level in the 1960s. Approval fell during the inflationary years of the 1970s and the concessionary years of the 1980s, and (paradoxically) plunged during the financial crisis and Great Recession, hitting an all-time low of 48% in 2009 (the only time it fell below 50%). From that trough it’s risen steadily and has hovered around 70% or just below since 2021. You could mourn its refusal to rise further but holding just below historical peaks in what seem like reactionary times is encouraging.

Partisan differences are huge; as Gallup puts it, “90% of Democrats, 69% of independents and 41% of Republicans express approval.” Though we’ve heard a lot about how the GOP is now the workers’ party, that 41% rating is actually down from 56% in 2022, and the D–R gap is almost 20 points wider than it was in 2001. Josh Hawley may cynically show up at a picket line now and then, but his party isn’t even offering gestural support.

Gallup also finds that 8% of all respondents are in a labor union, and 13% of the employed. Just 1% of coupled households report that both members are in a union. (According to the BLS, 10% of the labor force is unionized.)

High approval ratings are marvelous, but turning those into higher union density is very hard work. Could be a lot worse though.

*In the US, May 1 is celebrated as Loyalty Day and Law Day, holidays created during the Eisenhower administration in the spirit of the Red Scare. For a comparison of Labor Day and May Day, see Olive Johnson’s 1936 pamphlet.

Fresh audio product: Bill Buckley—his life, thought, and influence

Just added to my radio archive (click on date for link):

August 28, 2025 Sam Tanenhaus, author of Buckley: The Life and the Revolution that Changed America, on Bill, his thought, and his influence

Fresh audio product

Just added to my radio archive (click on date for link):

August 21, 2025 Osita Nwanevu, author of The Right of the People, on the flaws of American democracy—and some cures • Derek Guy on the evolution of upper-class men’s dress over the decades