Contingency: a last word

Having refuted (here, here, and here) a lot of folk wisdom about increased volatility in the job market, I’d to file a postscript on the meaning of it all. The folk wisdom exaggerates the prevalence of contingent and temporary work, but that doesn’t mean the working class is living in ease and comfort. It’s not.

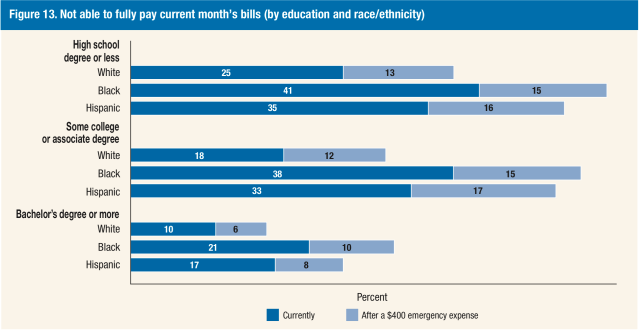

For evidence we can turn to a very orthodox source—the Federal Reserve’s survey of economic well-being (and data appendix). A third of respondents, 33%, report themselves “living comfortably”; 40% are “doing okay,” 19% are “just getting by,” and 7% are “finding it difficult to get by.” Given people’s predilections toward giving upbeat answers, these are not impressive figures. Just 42% “always” or “often” have money left over at the end of the month. Almost half—47%—owe money on their credit cards; 29% report their credit card debt growing, and only 20% have paid any of it off. Over half, 51%, always or frequently make only the minimum payment. Almost a quarter, 22%, wouldn’t be able to pay their bills in the month the survey was taken. (There are large demographic disparities in that count: 25% of whites with a high school degree or less fall into that category—not all that much more than the 21% of blacks with bachelor’s degrees or more. See graphic below.) Half have less than $100,000 saved for retirement; 20%, less than $10,000. Almost one in ten, 9%, received food stamps in the previous year. Well over half, 57%, could not cover their regular living expenses should they lose their job with saving or even borrowing. Half couldn’t cover an emergency expense of $400 without borrowing or selling something. One in ten had to forego a doctor visit or skip on prescription drugs because they lacked the money; one in five skipped visits to the dentist. All together, about a quarter skipped some form of medical care because they couldn’t pay. Over a third, 37%, have some form of lingering medical debt that wasn’t covered by insurance.

The Fed assembled responses into measures of financial well-being. They found that 42% of Americans have a “high likelihood of material hardship”: 38% of whites, 46% of blacks, and 52% of Hispanics/Latinos.

While most of these measures have improved over the last few years as the Great Recession recedes into the past, they’re still awfully high. And because most people have so little in the way of savings, and because our welfare state is so brutally minimal, even a modest shock like an illness or a temporary spate of unemployment can throw people who thought they were solidly middle-income into penury and despair. (A striking example: in the 1970s, about two-thirds of the unemployed were collecting unemployment insurance benefits, a minimal standard of decency; that’s now down to about a third.) And this doesn’t even address the level of stress—visible in soaring antidepressant and opioid use and sagging life expectancy—that the increased competitiveness of the neoliberal era routinely produces, even among the employed.

So while the gig economy is mostly a fantasy produced by publicists (and leftists who take the publicity too seriously), there’s plenty of entirely preventable economic misery around.