Employment report

As the job market loses steam, and Congress dithers over a new bailout package, Americans are having a harder time paying their bills.

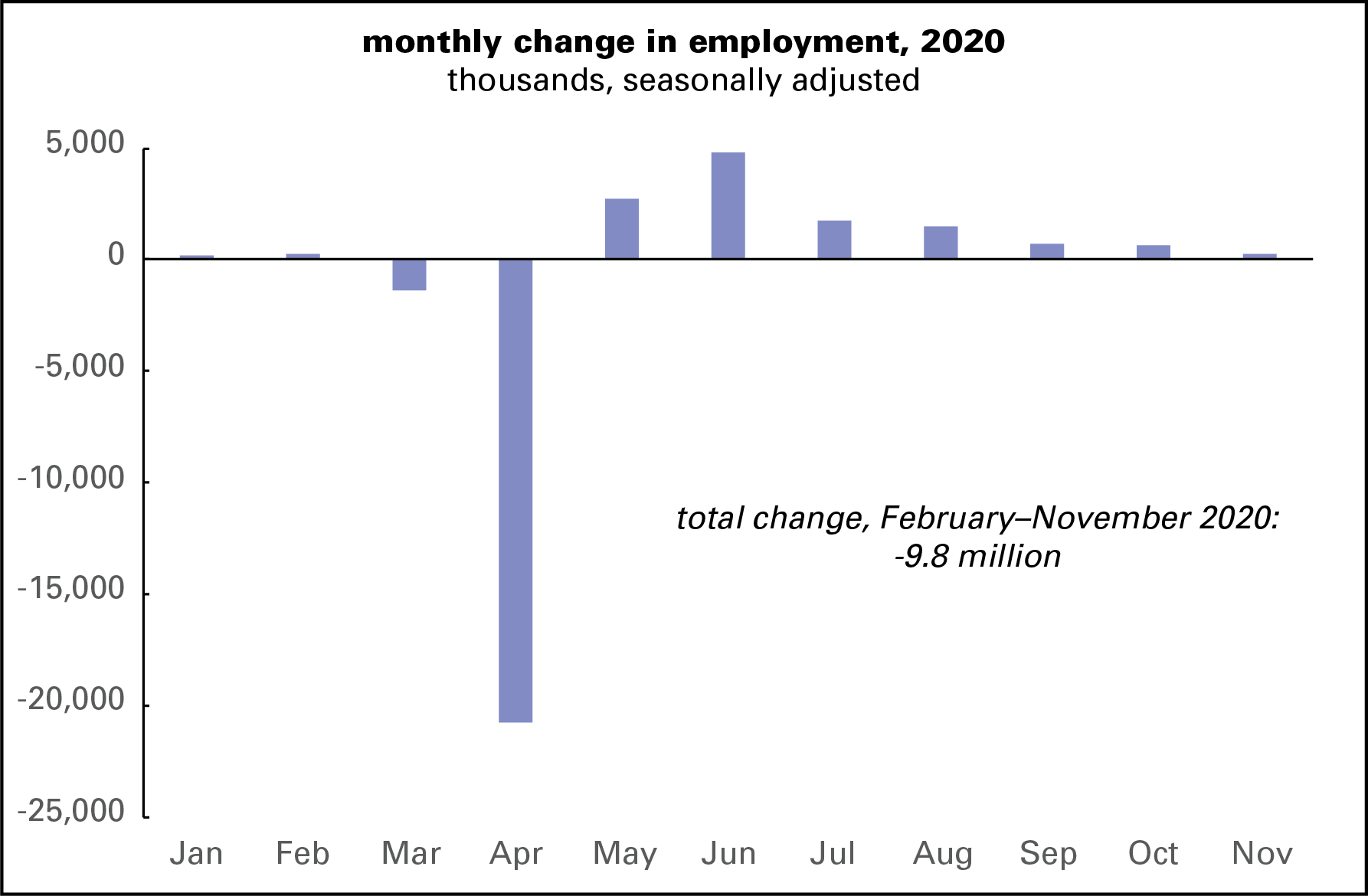

First the job market. Employers added 245,000 jobs in November, the least since the recovery from the March–April crash. As the graph below shows, that recovery has been losing momentum since June, when employment rose by 4.8 million. What looks to be happening is that the easy recalls after the initial shutdown have happened, and with the giant stimulus of the CARES Act receding, there’s not much fuel for more. It would not be a surprise to see some minus signs starting early next year, as sickness and death march across our great land.

Of the 22.2 million jobs lost between February and April, we’ve now regained 12.3 million, or not quite 56% of the loss. Despite the recovery, November employment was still 6.4% below February’s, which would qualify as a savage recession in itself. At the low point in the aftermath of the Great Recession, February 2010, employment was 6.3% below the its pre-recession peak in January 2008. Public employment has not seen any recovery; governments at all levels shed 969,000 workers in March and April, and another 344,000 since, for a total of 1.3 million. More than half those losses come from local government education, and another quarter from state government education. COVID-19 is ravaging our schools, and the state and local fiscal crises have yet to bite fully.

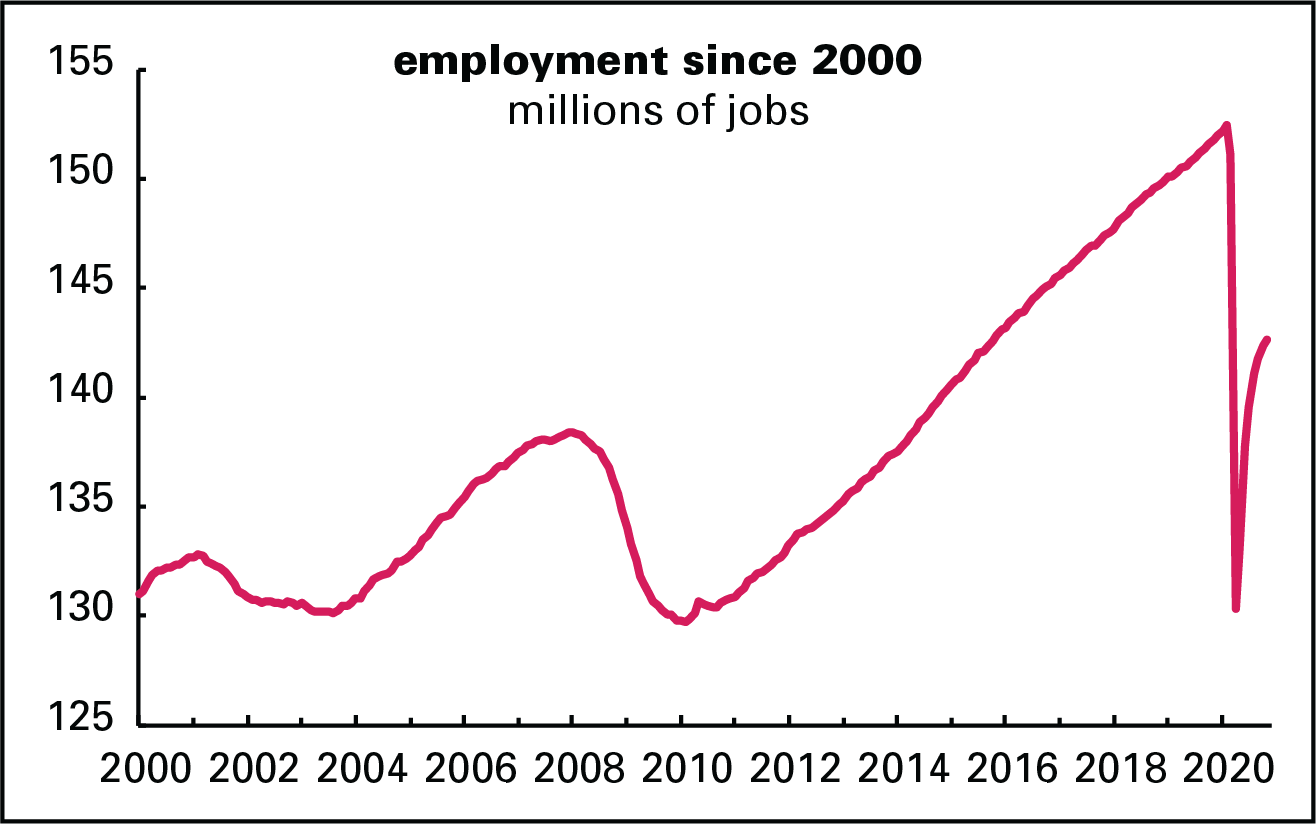

As the graph below shows, the initial drop in jobs took us back to the early 2010 low, meaning the entire comeback from Great Recession’s depths was undone in just weeks. Next to that, the 2008–2010 decline looks mild, though it was anything but. Recovering just over half those jobs takes us back to the late Obama years. Trump will leave office the only post-World War II president with fewer people working than when he took office.

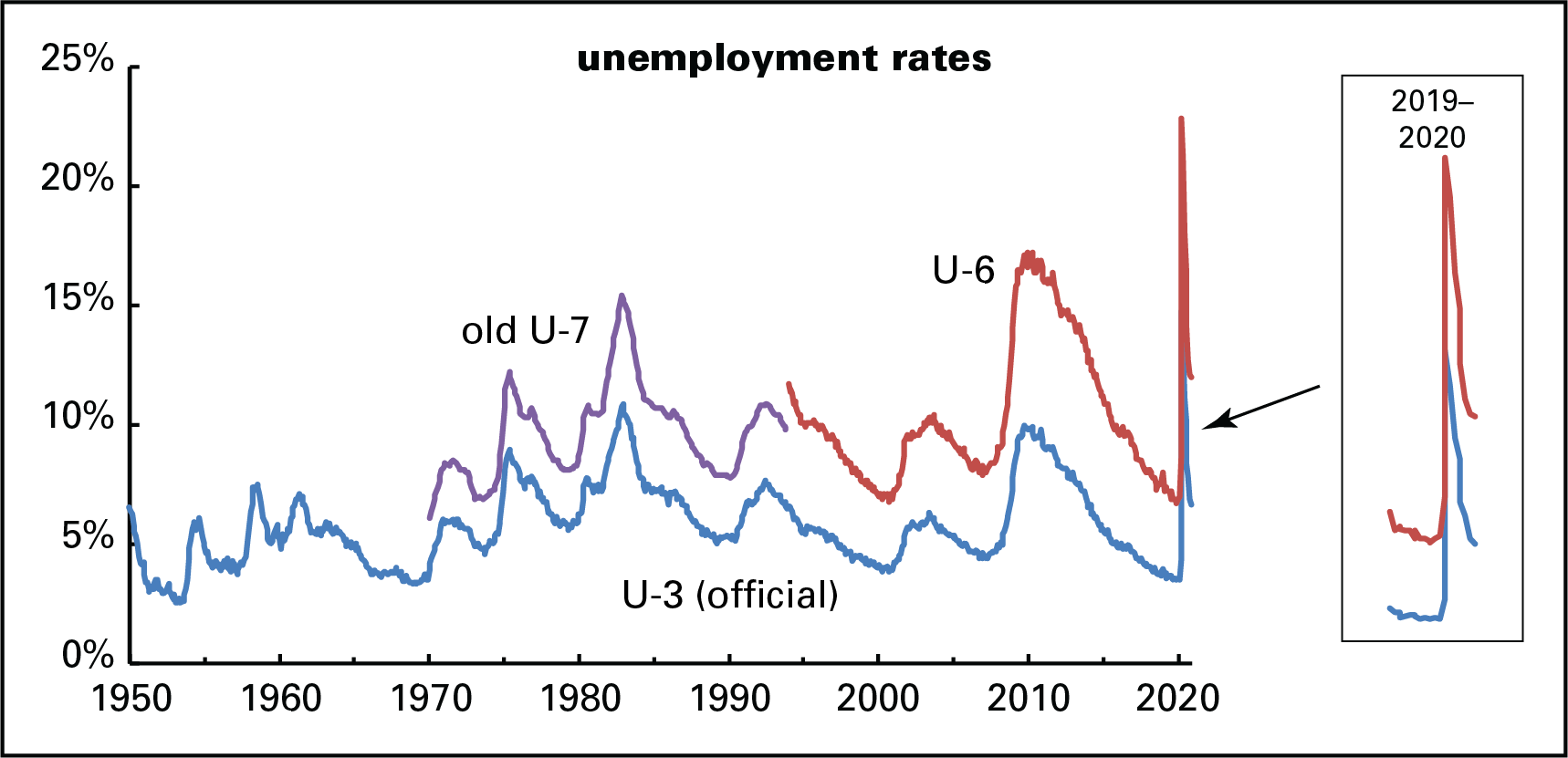

The story is similar for unemployment: a rapid initial drop from April’s 14.7%, the highest since 1940, and well above 1982’s 10.8% and 2009’s 10.0%, to 6.9% in October. November, however, saw just an 0.2 point drop to 6.7%, a number that’s higher than three-quarters of all the months since 1950. (Graph below.) And that’s the official, aka U-3, unemployment rate, which requires you to be actively looking for work. The broader U-6 rate, which adds workers who’ve given up the search as hopeless and those who want full-time work but can only find part-time, was 12.0% in November—down sharply from April’s 22.8%, but down just 0.1 point from October. U-6, and its not-strictly-comparable U-7 predecessor, were higher only during the Great Recession and the early 1980s slump. In other words, even with recovery, unemployment remains near severe recession levels.

Despite the improving overall unemployment numbers, the story under the surface is less encouraging: more workers are reporting themselves as permanent job losers (rather than being on temporary layoff), and we’re developing a serious long-term unemployment problem. The average duration of unemployment in November was 23.2 weeks, higher than at any point before 2009, when the Great Recession was setting records.

Unemployment is an important indicator, but it doesn’t reflect the full picture: if people give up on the job search, they’re not counted as jobless. The participation rate—the share of the adult population either employed or actively searching for work— was 61.5% in November, an improvement from April’s 60.2%, but not that much of one, and a level we haven’t seen since 1978, when there were many fewer women in paid work. (Women were about 40% of the workforce then, and are 50% now.) The low participation rate suggests that a lot of people aren’t trying because things look so miserable.

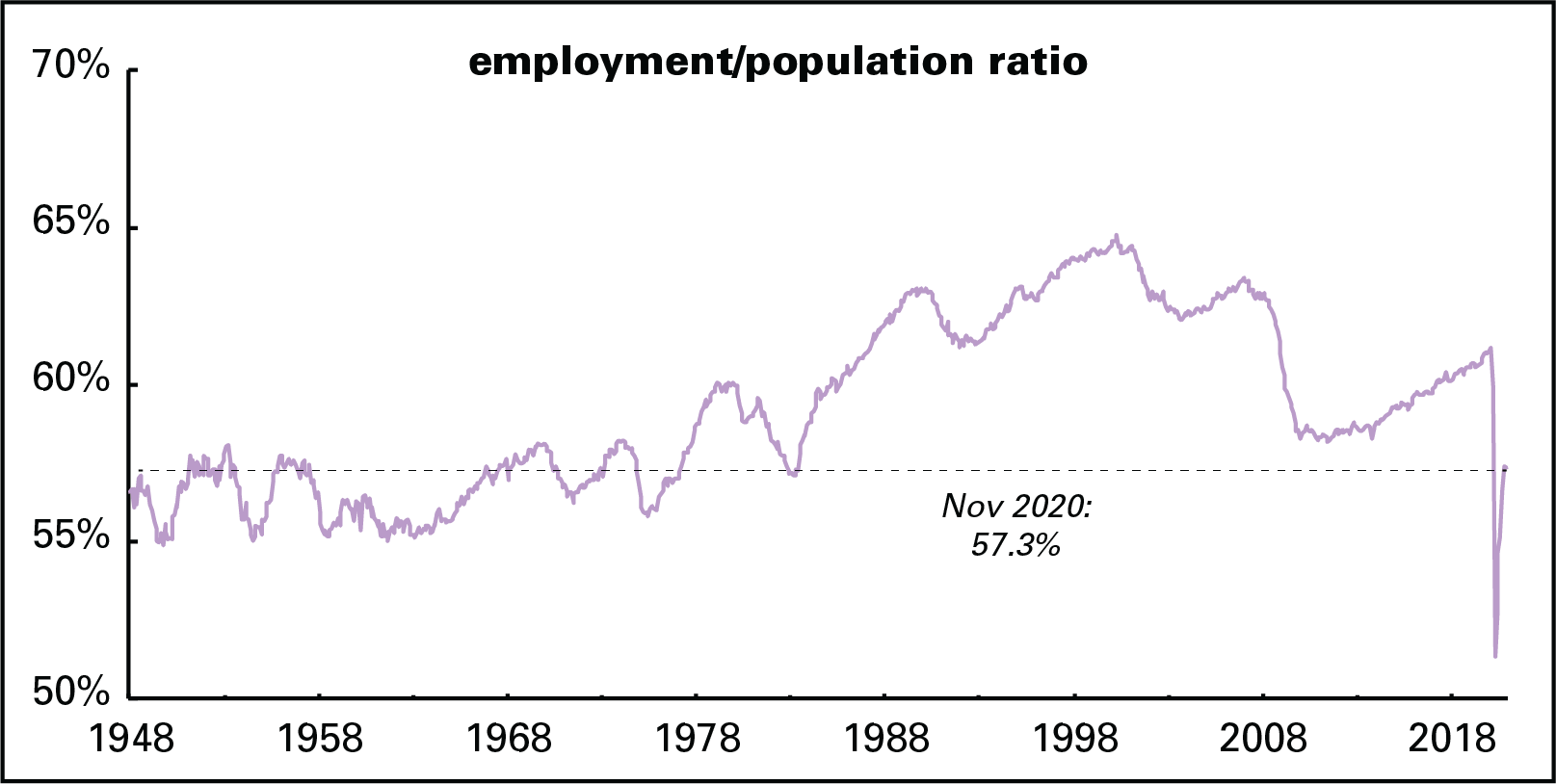

Rather than the unemployment rate, another way of measuring slack in the labor market—as employers think of it: they love a “slack” job market because it means they can more easily dictate terms—is the employment/population ratio (EPOP), the share of the adult population working for pay. As the population ages and boomers retire, the ratio will trend downwards over time. It peaked around 2000, and the expansions of 2002–2008 and 2009–2019 never recovered the ground lost in the recessions that preceded them. But the drop from February to April was fierce, taking the EPOP to an all-time low of 51.3%; it had barely been below 55% in its seven-decade history. It’s recovered to 57.3%, a level it frequented forty to fifty years ago.

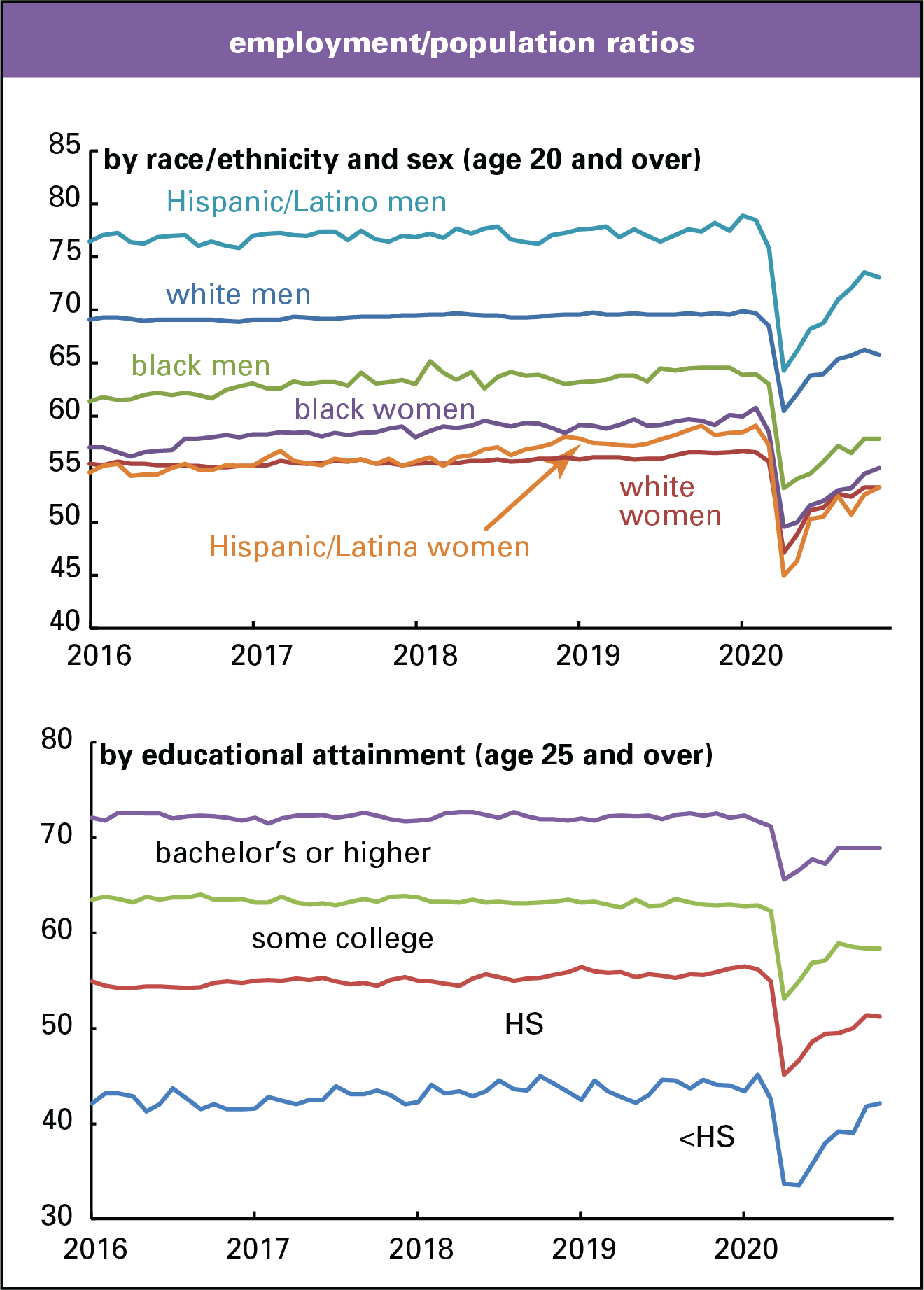

There’s demographic variety under the EPOP’s headline level. Here’s what its recent history by race, sex, education, and age looks like. Several points deserve mention.

• The ranking by race/ethnicity and sex may surprise some. Hispanic/Latino men are employed at a significantly higher rate than white men, which you’d never know if you listened only to Donald Trump. The lowest EPOP is found among white women (though they’re now tied with Hispanic/Latina women).

• Despite everything you hear about the pointlessness of going to college, people with bachelor’s degrees (43% of the workforce) are employed at higher rates than those with only some college (25%), and those with some college more than those with only a high school diploma (25%). Though they’re not graphed, the unemployment rates of people with bachelor’s degrees are more are consistently about half that of those with only high school. And those without a high school diploma, just 7% of the employed, are less likely to be employed than not.

• EPOPs of all demographic groups took a severe hit in the early months of the crisis and have yet to claw back their losses.

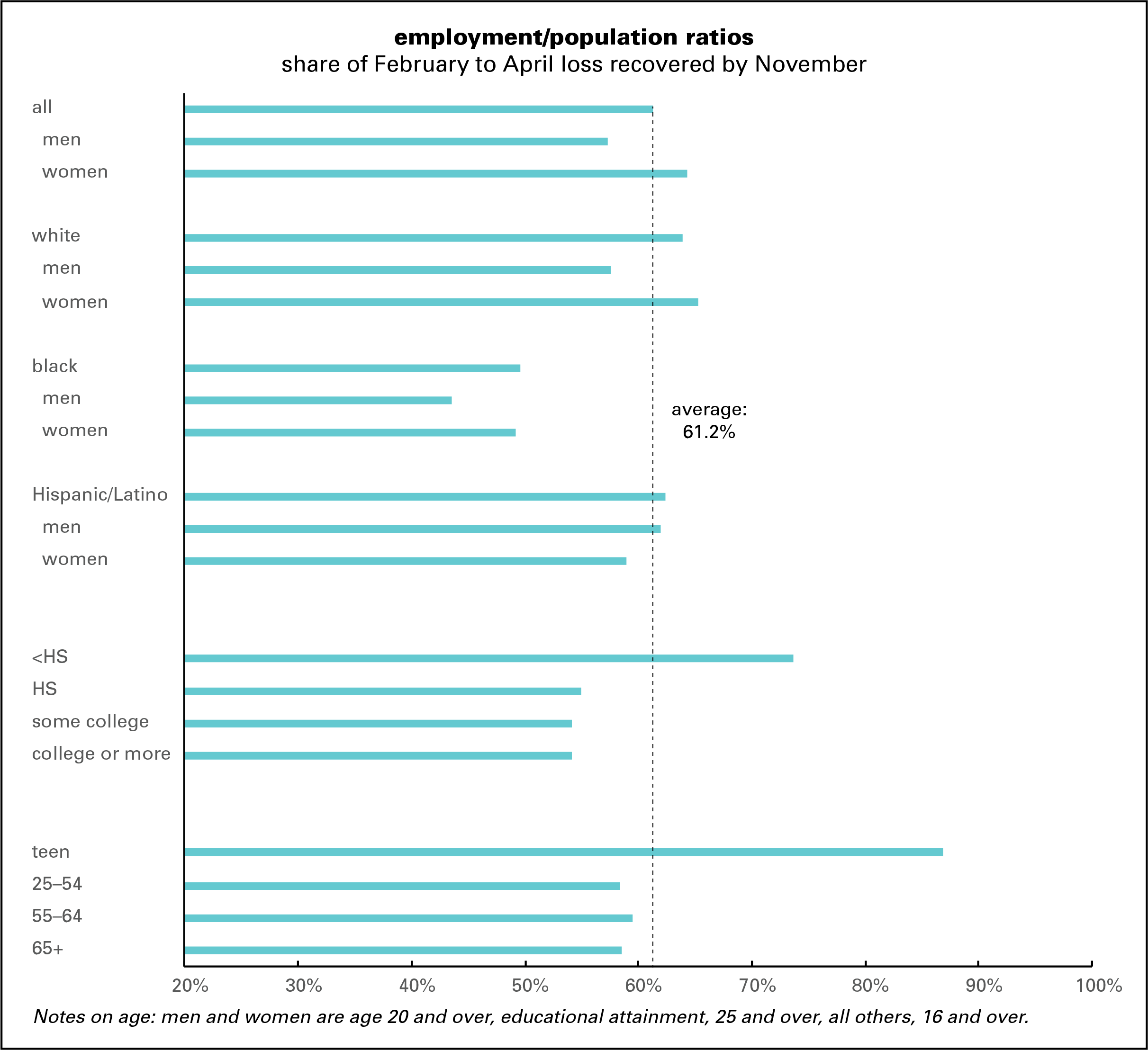

Here’s a measure of how well the various groups have recovered. Men have done more poorly than women, and black people worse than whites or Hispanics/Latinos. Aside from those who didn’t finish high school, education hasn’t had much bearing on the rate of recovery, or age except for teenagers. (Both of those are small groups.) At 43%, black men lag the average by 18 percentage points; if they matched that average, 1.6 million more would be working. For the entire population, if we could get back to February’s EPOP, almost 10 million more would be working.

Yes, there’s been some recovery, but the job market, which is what most people rely on to pay their bills, is still a wreck. The table below is derived from the Census Bureau’s experimental Household Pulse Survey, before the pandemic, 72% of respondents reported having enough of the food they wanted. That fell to 55% in mid-May, recovered into October, and has been sliding in recent weeks to 58% on the latest reading. In numbers, about 20 million people sometimes or often had trouble getting all the food they wanted; now 26 million do. Pre-pandemic, about 175 million could get enough of what they wanted; that’s now down to 125 million, a decrease of 50 million. According to the same survey, 83 million people, or 35% of the population, is finding it somewhat or very difficult to pay their regular bills. Unfortunately there’s no pre-pandemic baseline to compare this to, but it’s almost certainly a deterioration from an inexcusably high number.

food sufficiency

| enough of wanted | enough, but not always what’s wanted | sometimes not enough | often not enough | |

| pre-pandemic | 71.6% | 20.2% | 6.5% | 1.7% |

| 5/12/20 | 54.8% | 34.6% | 8.5% | 2.1% |

| 10/12/20 | 61.4% | 28.3% | 7.9% | 2.5% |

| 11/23/20 | 58.2% | 29.9% | 9.0% | 2.9% |

| change from pre-pandemic | -13.5% | 9.7% | 2.5% | 1.2% |

Housing stress is rising too. CoreLogic, a credit-tracking firm, reports that 6.3% of mortgages were past due in September, up from 3.8% a year earlier, and 3.3% were 120 or more days past due, more than triple September 2019’s 1.0%. Every state is showing a rise in serious delinquency rates. If it weren’t for the forbearance programs enacted in the early pandemic days, foreclosures would be rising, but we’re not there yet.

Renters, who are generally poorer than homeowners, are showing more stress. The Federal Reserve Bank of Philadelphia reports that 4% of renter households, representing 4 million people, are significantly behind on their rent, owing an average of $5,400 each. That number would have been much higher had it not been for the $1,200 payments and $600 weekly unemployment benefits that were part of the CARES Act. Now that those have expired, trouble is rising. If there’s no aid forthcoming, and no significant recovery in the job market, 10% of all renters will find themselves seriously behind on their rent in a few months. A renewal of CARES-style payments would cut those numbers to less than 1%.

COVID-19 is bad enough. If we had a civilized government, we could mitigate its economic effects, but alas we don’t have one of those.