Scattered speculations on the US ruling class

This is the text of a talk I gave at a virtual conference sponsored by the Havens Wright Center for Social Justice at the University of Wisconsin, February 13, 2023. The other panelists were Ho-fung Hung and Göran Therborn. It draws heavily on my Jacobin article on the ruling class and Harper’s magazine article on the WASPs but updates them to the lamentable present.

In preparing these remarks, that old Gayatri Spivak title came to mind, “Scattered speculations on the question of value.” I don’t mean to cite any more of that article, something I haven’t read for at least thirty years, but scattered speculations are the spirit of what follows.

If you read my article on the US ruling class in Jacobin, you know that I think it’s a pretty debased formation, with few ambitions beyond making as much money in as short a time as possible. Its political wing looks puny next to its ancestors. Its empire is in decline and its industrial prowess, with a few exceptions, is no longer the envy of the world. We’re one of the few countries in the world where life expectancy is declining. Mass shootings have become totally routine; in the first 42 days of this year, we had 66 of them. On a grander scale, the US is having a hard time adjusting to China’s rise alongside its ebbing. I’m not saying the US as an imperial capitalist society is on the verge of collapse; these things take time. But it’s underway.

The quick version of my historical analysis is that the WASP elite  that ruled the country from the late 19th century through the 1970s lost its pre-eminence and was succeeded by, well, it’s not easy to say what, except that it’s more mercenary and short-sighted than its predecessor. I don’t mean to romanticize that old formation; they were often appallingly racist, and eager to follow and then eclipse the English at the imperial game. But it had a coherence and a discipline that seems lacking today when accumulating the maximum amount of money in the shortest possible time seems to be the goal.

that ruled the country from the late 19th century through the 1970s lost its pre-eminence and was succeeded by, well, it’s not easy to say what, except that it’s more mercenary and short-sighted than its predecessor. I don’t mean to romanticize that old formation; they were often appallingly racist, and eager to follow and then eclipse the English at the imperial game. But it had a coherence and a discipline that seems lacking today when accumulating the maximum amount of money in the shortest possible time seems to be the goal.

And before going any further, I should offer my definition of the ruling class. It consists of a politically engaged capitalist class, operating through lobbying groups, financial support for politicians, think tanks, and publicity, that meshes with a senior political class that directs the machinery of the state. (You could say something similar about regional, state, and local capitalists and the relevant machinery.) But we shouldn’t underestimate the importance of the political branch of the ruling class in shaping the thinking of the capitalists, who are too busy making money to think much on their own or even organize in their collective interest.

privatizing the private sector

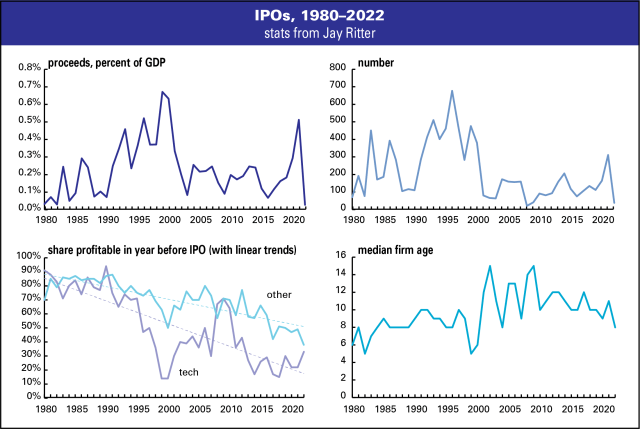

To me, the US ruling class looks deeply split, and not just by region, party, or temperament. It’s also split lines of ownership. In recent decades, we’ve seen then rise of private models of ownership, like private equity and the large private corporation. During the decade of free money, there was an explosion in new venture-capital-financed firms, which, once they hit a billion dollars in valuation, became known as unicorns. There were even deca-unicorns. By Crunchbase’s count, there are currently 1,439 unicorns, valued at almost $5 trillion, based on $850 billion in real-money investment. (Whether those valuations are correct is a good question.) While some of these companies went the usual route of selling stock and becoming public corporations, an unusually large number didn’t, and even of those that did, waited a long time before doing their initial public offering. (See graphs below; data from Jay Ritter.) In the late 1990s dot.com bubble, there was a rush to go public. It seemed that many financiers and entrepreneurs had decided they didn’t want the scrutiny that came with having numerous outside stockholders.

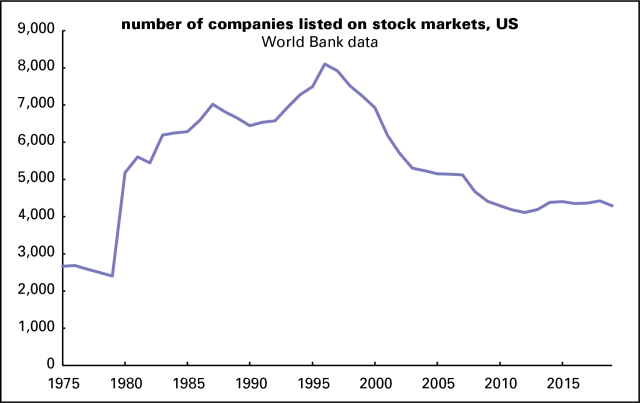

They’re not alone in this. According to World Bank stats, the number of public companies in the US fell by almost half between a 1996 peak and 2019, the last year they have available. Much of that decline came from takeovers, but private equity firms have also taken thousands of public companies private over the last few decades. And there were many fewer IPOs as well.

A good deal of business support for right-wing politics comes out of this branch of the owning class (and I include hedge funds in this category as well). Not only do they hate regulation, as owners of private businesses, they don’t have outside shareholders causing trouble. It feeds nicely into the authoritarian social Darwinism that characterizes the milieu. The notorious Charles Koch, CEO of the second-largest privately held company in the US, has not only showered billions of his own money on the mission, but he’s organized rich fellow thinkers into doing the same. Many of them—Koch himself, but characters like Harold Hamm, fracking billionaire and friend of Donald Trump—are in dirty industries and fight climate science and the euthanasia of the carbon sector. Steve Schwarzman, head of private equity firm Blackstone, was a Trump advisor and loyalist until it became untenable. Blackstone itself is a public company, at least in name, but Schwarzman holds 42% of the voting rights and outside shareholders have little say in how the company is run. Though he defended Trump after the Charlottesville race riot, he’s since turned on him, but still supports Republican candidates generously. Private equity is driven by an asset-stripping strategy; Koch, Hamm, and Co. are driven by a nature-stripping strategy. It’s not a long-term plan.

Schwarzman is not alone among right-wing moneybags in opposing Trump, though he’s late to the party. Along with Koch, who never liked him, entities like the Club for Growth are trying to block him from getting the 2024 nomination, but while Trump’s star has faded some, he still has a lot of loyalists and the MAGA mass base isn’t likely to get excited by anyone the money wing comes up with. This looks to be a split between private capital and the regional petite bourgeoisie that provided something of a mass base.

A few words about that mass base. Since the 2016 election, analysts have talked about much of Trump’s support coming from the white working class. That’s misspecified. Though they may code as working class to metropolitan elites, a lot of those supporters don’t have many scratches in the cargo beds of their giant pickup trucks. As a 2019 paper by Thomas Ogorzalek and collaborators put it, they’re nationally poor and locally rich—a provincial petite bourgeoisie, lawyers, accountants, car dealers, contractors. That has long been a base for right-wing politics, but it’s a larger and richer stratum than it was in the heyday of the John Birch Society. Those sorts were heavily represented in the Capitol riot of January 6, 2021. The Congressional Freedom Caucus is their political representative.

The center-left has nothing like that. It has some billionaires, but they’re not organized like the Koch Network and its cousins, nor do they have anything like that ideology or an ideological distribution system. Koch, via his advisor Richard Fink, followed the Mont Pèlerin Society’s model of political influence, starting with peak intellectuals like Friedrich Hayek and Milton Friedman, spreading out and down through think tanks, and then to the pundits and publicists who try to sell their line to the masses. As Burton Yale Pines of the Heritage Foundation put it back in the 1980s, “Our targets are the policymakers and the opinion-making elite. Not the public. The public gets it from them.”

and on the center-left…

Center-left politics lacks any of the energy or drive of the right’s. Its vehicle, the Democratic Party, is haunted by a structural contradiction: it’s a capitalist party that has to pretend otherwise, carefully, for electoral purposes. For the first time in decades it has a leftish wing and the leadership isn’t happy about it. In early February, 109 Democrats in the House of Representatives voted for a Republican bill “denouncing the horrors of socialism” and attributing 100 million deaths to it, more than the 86 who voted against it. (Ten years ago, you probably couldn’t have gotten that many “no” votes, but ten years ago the bill probably would never have been introduced.) The party reshaped its primary calendar to lead with South Carolina, one of the most conservative states in the country, which is likely to put any leftish candidate at an early disadvantage. Sure, Senate majority leader Chuck Schumer goes to fundraisers for DSA-affilitated candidates, but he’ll be on the scene to defend the means of production against expropriation if and when it becomes necessary.

To some degree, Biden has bent to the influence of that internal party left. The pandemic relief bill was very generous, and the infrastructure and climate legislation, while well short of what it should have been, is far from trivial. Biden and the Congressional Democrats passed a bill to subsidize the domestic chip industry (essentially giving them the money they spent on stock buybacks over the last decade to do real investment), a form of industrial policy which would have been poison to 1990s Clinton Democrats. Largely overlooked in the general discourse, the legislation offers a big kick to unionization as well. As the New York Times put it recently, “Tucked into all of those laws were measures to give unions the power to effectively tell employers: You must pay union-scale wages and use union apprenticeship and training programs, so you might as well hire union workers.”

But there looks to be limited support for these reindustrialization and climate schemes among the big bourgeoisie. When I interviewed the political scientist Alfredo Saad-Filho about Brazil last week, he said that that country’s bourgeoisie no longer has a national project. Once it wanted to industrialize, to develop Brazilian technology to a world level. Then it tired of that and just wanted to speculate in finance and real estate and loot the Amazon. Last time he was president, 2003–2010, Lula promoted industrialization, a policy that was reversed when the right wing took over; he plans to do it again. But it has almost no bourgeois constituency. It all sounded very familiar to me.

It reminded me of the famous passage from The Class Struggles in France, where Marx described how “the finance aristocracy, in its mode of acquisition as well as in its pleasures, is nothing but the rebirth of the lumpenproletariat on the heights of bourgeois society.”

woke capitalism

This split within the bourgeoisie is pronounced on climate. On the class’s center-left, there’s Lawrence Fink, head of BlackRock (which got its initial funding from Blackstone—it’s a small world), the world’s largest money manager, with $10 trillion under its flag. Fink has made a big deal out of using his investment clout to promote what in the trade is called ESG, environmental, social, and governance standards. (Governance refers to how corporations are run, not public policy.) It’s very weak tea. A couple of years ago, an alumnus of BlackRock’s ESG program, Tariq Fancy, wrote a multipart polemic denouncing it as pure hot air, a sales gimmick concocted by bankers who travel the world in private jets talking about how bankers could save the climate. But they can’t.

A large portion of BlackRock’s capital is invested in index funds that arrange their holdings to match standard market measures like the S&P 500. (I’ll have a bit more to say about these in a bit.) Since both theory and practice have proved that it’s nearly impossible to beat the market unless you’re George Soros or Warren Buffett, index funds have come to dominate the investment landscape. But by definition that means that BlackRock is limited in how much of the stocks of malefactors it can sell. It could lobby their CEOs, but since the firm couldn’t punish it by selling the stock, the CEOs have no incentive to listen. It can sell stock of carbon emitters in actively managed funds, but it doesn’t look to have done much of that.

As ineffectual as this all may be, it has enraged the right, which is now on a campaign against “woke capitalism,” or what the irrepressible Marjorie Taylor Greene calls “corporate communism.” Republican states are withdrawing pension assets from BlackRock management, and Florida Gov. Ron DeSantis is making ESG into one of the fronts in his war on wokeness. (The Republican campaign against is ESG is facing some pushback from bankers though.)

Some of this is political posturing, of course, and some of it emerges from the right’s view of non-fossil sources of energy as unmanly, but it also reflects the party’s heavy financial reliance on the carbon sector. It’s long been a voice for dirty industry, but it has only gotten more dedicated to the cause as the Dems make more gestures in a climate-friendly direction. No other conservative party in the rich world approaches the GOP’s level of climate cretinism. But Fink’s climate activism, if you can call it that, is unusual in Corporate America. And if you think, as I do, that capitalists lack a spontaneously developed politics and must often be organized in their own long-term interests by the political class, then Biden’s weak leadership and low approval ratings aren’t up to the task.

capitalist self-abolition

I mentioned index funds earlier; let me develop that some. I got interested in ruling class studies when I was writing my book Wall Street, specifically around the question of who runs large corporations. The answer is not self-evident. By the mid-1990s, when I wrote most of the book, the so-called shareholder revolution, which broke out in the late 1970s and early 1980s, was well along in its work of transforming how corporations are run. In the late 19th and early 20th centuries, as the form of the modern public corporation was taking shape, financiers had the upper hand. They supervised mergers and dominated corporate governance. But with the 1929 crash, they fell into disrepute, and in the early decades after World War II, financial operators had almost no influence over management. It was the era of John Kenneth Galbraith’s new industrial state, when a technocracy allegedly took precedence over pre-Crash doctrines of profit maximization. Corporations were still mighty profitable in the 1950s into the late 1960s or early 1970s, but shareholders had become vestigial to how firms were run. Share ownership was dispersed among millions of individual shareholders, who couldn’t have come together to speak with anything like one voice. In the early 1950s, households owned over 90% of stock outstanding; pension funds, under 1%, and mutual funds not much more. By the late 1970s, the household share slipped under 60%; pension funds’ share to almost 20% and mutual funds another 3%.

With the intellectual leadership of finance professors like Harvard’s Michael Jensen, and the monetary leadership of investment shops like Kohlberg Kravis Roberts, the era of managerial dominance came to a brutal end with a round of takeovers and shareholder-forced restructurings. The technostructure was replaced with an intensified devotion to profit maximization, specifically in the form of maximizing stock prices. The growth in institutional ownership, replacing the individual ownership made takeovers easier to negotiate and management easier to lobby.

To Jensen and the practitioners of Jensenism, corporate managements were too complacent and not focused enough on getting profits and stock prices up. The point of unwelcome takeover attempts was to wake up the laggards—and make some money by slimming them down and putting the squeeze on their workers.

As the 1980s turned into the 1990s, pension fund activism replaced hostile takeovers as the prime mode of enforcing the corporate order. The pension fund share of stock ownership hit a high of 27% in 1986 and the household share under 45%. The pension fund share would decline as employers cut back on pension coverage, but now the household share is under 40%, and mutual funds are over 20% and pension funds, 10%. While the ultimate beneficiaries of pension and mutual fund assets are individuals—disproportionately better-off ones, of course—the money is run by professional managers who are economically and politically part of the financial aristocracy.

So entrenched is the practice of maximizing stock prices that firms have been devoting a huge share of their resources over the last few decades to buying their own stock to boost its price. One of the central achievements of the shareholder revolution was to transform managerial pay from a regular paycheck into something dependent on the stock price. The point was to get CEOs to think like shareholders, and not princes of their own realm. It has worked. Nothing shows this alignment of interests like the fact that since 2000, big firms have spent just over half their operating profits on buying their own stock; this makes both shareholders and CEOs, who are paid based on the stock price, very happy. Before 1982, buybacks were largely illegal; now they’re approaching a trillion dollars a year in the US. Keynes was, no doubt, something of a starry-eyed liberal when he wrote (in the wake of the ’29 crash) that the point of investment was to defeat the dark forces of time and ignorance, but it’s now hard to believe that was even once a pleasant myth.

The fight over control of big corporations between shareholders, meaning professional money managers, and top management, over the last several decades was an interesting intra-family squabble. As every Marxist schoolchild knows, the capitalist class owns the means of production, but when you look at the matter closely, the who and how of that aren’t self-evident. And there’s a new wrinkle. As I said earlier, index funds of the sort that BlackRock runs—and along with BlackRock, there are two other giants, Vanguard and State Street—now own about a quarter of the stock represented by the S&P 500 index, a category that is almost synonymous with Corporate America. Among the rationales for making stock prices so central at the outset of the shareholder revolution 40 years ago was that they were supposed to serve as real-time grades on corporate performance because they reflected the wisdom of the crowd, which would buy winners and sell losers. So, a low price relative to profits or underlying assets was a sign of chronic underperformance that invited the discipline coming from takeover artists (or, as Alan Greenspan once called them, unaffiliated corporate restructurers). But index funds can’t sell, which compromises the alleged signaling mechanism. And managers of index funds, who seem like sitting ducks for replacement by ChatGPT, have no incentive to lobby management and management has no incentive to listen, as I said earlier. So, what does ownership mean here? What function, even by the standards of bourgeois finance, do shareholders serve? Maybe it’s time to revive Marx’s observation that the joint stock company marks “the abolition of the capitalist mode of production within the capitalist mode of production itself.” I’ll concede there are some details to work out here though.

off to the bunkers

I’ll conclude by returning to a theme I brought up earlier: the shrunken time horizon of the US ruling class. The current motley crew looks nothing like the set who planned the post-World War II order. They emerged from—or recruits were assimilated to—an ethnically and socially homogenous WASP aristocracy who felt themselves above quotidian distractions and rank commercial temptations. Of course, it was all in the interest of long-term accumulation under US guidance, but it was all successfully planned and executed (at least until things started slipping some in the 1970s). Now with the US in a long process of imperial decline, our planning elite seems fragmented and lost. You have Republicans criticizing Biden for not having shot down the Chinese balloon quickly enough, and Democrats acting as if it was an act of heroism. Our rulers don’t act like they have any good idea about coping with the rise of China, except with bellicose and one hopes ineffectual gestures, because God knows, we don’t want bellicose gestures to lead to an actual war.

And we have a capitalist class that has apparently given up on the future—incapable of dealing with the climate crisis, a truly dire threat, but also consuming capital rather than investing it. Net investment—net, that is, of depreciation—by both business and government—has been falling relative to GDP for decades. The vast flow of free money and 0% interest rates from the Federal Reserve has been channeled into an impressive set of bubbles: the most extended valuations of stocks in US history, crypto, unicorns, housing. It used to be normal to have one particular asset lead the way in a speculative orgy, whether it was stocks in the late 1990s or housing in the following decade. Now we’ve got multiple and serial bubbles that have only been partly deflated by the Fed’s tightening moves of the last year. And Wall Street is dearly hoping the central bank will reverse those moves in a few months and resume the cheap money flow. The bond vigilantes of the 1980s and 1990s, always on the lookout for an inflation that needs to be crushed, have largely disappeared.

I’ll give the last word to Etienne Balibar, who has diagnosed the affliction precisely. “We realize now that our ruling class is no longer a bourgeoisie in the historical sense of the word. It does not have a project of intellectual hegemony nor an artistic point of honor. It needs (or so it thinks) only cost-benefit analyses, “cognitive” educational programs, and committees of experts. That is why, with the help of the pandemic and the internet revolution, the same ruling class is preparing the demise of the social sciences, humanities and even the theoretical sciences.” The bourgeoisie no longer has any civilizational project, national or otherwise. Live for today, and if the water rises, they can just move inland. Or to their underground bunkers.