About that stock panic

Stock markets have stabilized, at least for now, after a few days of what the press likes to call “turmoil.” What does it all mean?

There’s no doubt that stocks have been due for a comeuppance for some time: they’re very expensive. Since stocks represent claims on corporate profits, present and future, the conventional way to value them is by measuring their price against those underlying profits (or “earnings” in Wall Street lingo, since to the owning class, profits from capital are just like wages for labor: as they like to say, they put their money to work). Ideally they’d be measured against future profits, but no one knows what they are, so the next-best thing to do is measure them against past profits.

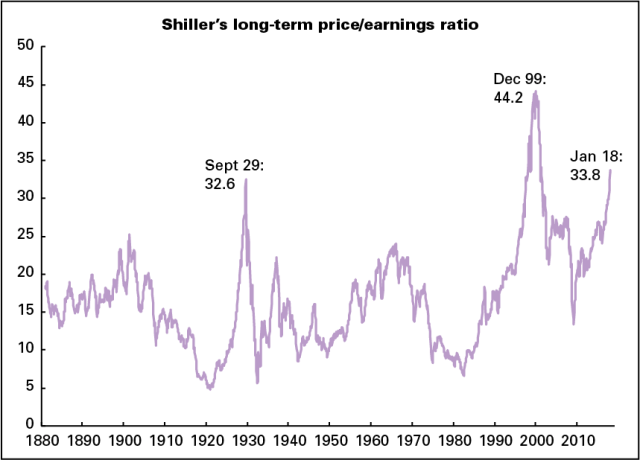

The standard measure for that is the price/earnings (PE) ratio—the price of a stock (or a stock market index) divided by corporate profits per share (or total profits of the stocks in the index). Since the late 19th century, the PE ratio for the broad stock market has averaged 16; since 1950, it’s averaged 18. It’s now 27. But PE’s can be volatile. To adjust for that, Yale economist Robert Shiller invented a longer-term measure, which adjusts profits for inflation and measures current prices against their ten-year trailing average. The century-plus average is 17; since 1950, it’s 19. It’s now 33. As the graph below shows, Shiller’s PE is higher today than it was at any point in a history that begins in 1881 except for the climax of the late-1990s bubble. It was lower in 1929 than it is today.

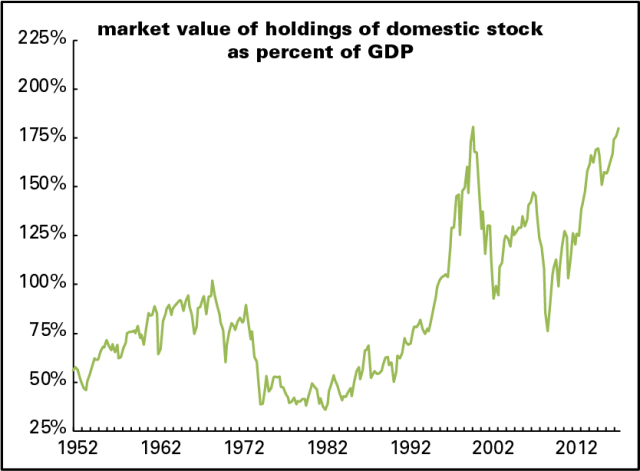

Another valuation technique is comparing the value of all stocks outstanding to GDP. That is now only a hair below its 2000 peak (see graph below).

And what about profits? Profits recovered far more quickly and dramatically than wages after the end of the Great Recession. In the first three years after that miserable event came to a formal close (2009–2012), corporate profits after taxes rose 55%. Meanwhile what corporations paid their employees rose just 12%. Stocks became quite rationally exuberant, celebrating the rise in profits and its likely continuation. Over those three years, stocks (measured by the S&P 500) rose 85%, taking them close to where they were before the financial crisis hit. The momentum in profit growth slowed (and that in wages and salaries picked up), but that didn’t stop stocks from rising further, surpassing the 2007 high in 2013, and then adding another 56% through the election of Trump. All that despite the fact that, as the graph below shows, corporate profitability peaked between 2012 and 2014 and has been edging down since.

Stocks paused for a week or so after the election as traders sussed out what this unexpected turn of events might mean, but as soon as it became clear that whatever his idiosyncrasies, Trump meant tax cuts and deregulation. So it was back to the races. Stocks added another 29% between November 2016 and January 2018, taking us to the extreme valuations described above. Rational exuberance was succeeded by the less rational kind.

strong economy?

Since Trump has been bragging for months about the stock market’s strength, the selloff is a marketing challenge for him. His administration weighed in with the customary reassurances, with both White House flack Raj Shah and Treasury Secretary Steven Mnuchin pronouncing the “fundamentals” of the economy “strong.” (You might think that officialdom might be reluctant to repeat the sort of language used by Herbert Hoover in 1929 and John McCain in 2008, but no.)

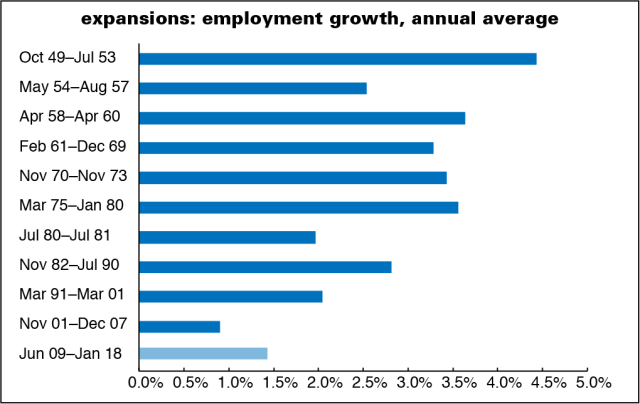

When people say the economy is strong they mean that unemployment is low and we’re adding 180,000 jobs a month. But millions have dropped out of the labor force. If the same share of the population were working now as at the 2006 pre-recession peak, 8.4 million more would be employed. As the graph below shows, this is the second-worst expansion for job growth out of eleven.

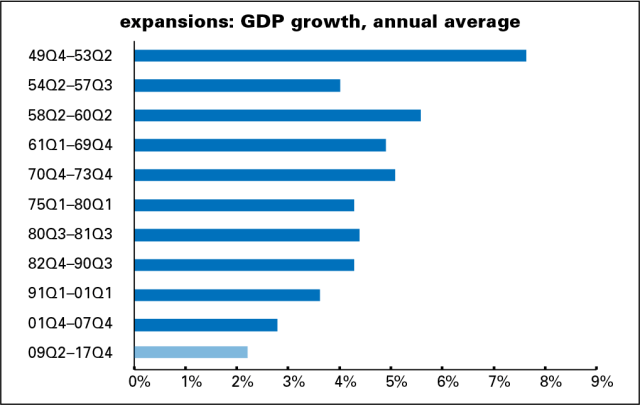

And by the most conventional measure of all, GDP growth, this is the slowest expansion since quarterly GDP stats begin in 1947. It’s now the fourth expansion in a row to be slower than its predecessor. Though the 1970s are mocked as a time of economic misery, growth was twice as fast between 1975 and 1980 as it has been since 2009.

Another standard measure of the strength of an economy is the growth in productivity—the value of output per hour of labor. It is quite weak, hovering close to 0. The politics of productivity are complicated. Productivity can be boosted through speedup and other forms of brutalizing labor. And productivity gains could all be captured by bosses in the form of higher profits and not by workers in the form of higher wages. But slow productivity growth puts a lid on income growth over time, and by the most orthodox of standards is a sign of a sickly loss of economic dynamism.

A major reason productivity growth is so weak is that corporations have been stuffing their shareholders’ pockets with cash rather than investing it in buildings and equipment. Since 2012, nonfinancial corporations have made net investments—net meaning after allowing for the depreciation of existing assets—of $2 trillion. Over the same period, they distributed $6 trillion to shareholders in the form of dividends, stock buybacks (intended to boost share prices), and takeovers. Instead of providing investment funds to businesses (which is what most people think it does, but it really doesn’t, and never has very much), the stock market has served as an instrument of value extraction for the last 35 years. It’s as if the owning class has given up on the future and just wants to load up on private jets and Roederer Cristal. In that sense, the current administration, which is full of asset-strippers, starting with Trump, is the perfect representation of this version of capitalism.

the selloff

The spark for the selloff came from last Friday’s monthly employment report, which showed a pickup in wage growth in January. (As this post shows, the pickup all came from upper-tier workers; the bottom 80% didn’t participate.) This was read as a sign of inflationary pressures that would drive the Federal Reserve to push up interest rates more aggressively than they might have otherwise. Higher rates are generally bad for stock prices and make it more expensive to be a professional speculator operating on borrowed money.

Through the Great Recession and its aftermath, there’s been more worry about deflation than inflation, and the normally inflation-averse Fed was looking for a bit more of it as insurance against a deflationary spiral. But as the unemployment rate kept falling, alarm about a tightening labor market—when the labor market is tight, not only can wages rise, but workers can develop an attitude problem—fueled increasing fears of incipient inflation. That inflation never really arrived—until, in a lot of eyes, that January spike in wage growth. Of course, one month’s numbers don’t mean all that much, but a lot of market players were just looking to be spooked.

It’s not only rising interest rates that are worrisome. To fight the 2008 financial crisis, the Fed and its central bank comrades around the world drove interest rates to record-low levels and promised to keep them there for a long time. But in addition to that they injected vast gobs of money into the financial system, a process called quantitative easing (QE). In the U.S., the Fed bought $3.6 trillion in Treasury and mortgage-backed bonds; other central banks around the world did similar things. Those purchases flooded the markets with money, which was supposed to stimulate the real economy by encouraging lending, but it didn’t do much of that. (Word is that former Fed chair Ben Bernanke thought that what the slumping economy needed was more fiscal stimulus—spending and/or tax cuts—but since those were politically impossible, QE was the only game in town.) It did, however, stimulate the financial markets mightily. Aside from providing money managers more cash to play with, the Fed’s guarantee that interest rates would stay very low sent investors searching for higher yields, great news for riskier assets like stocks (and more exotic assets like Silicon Valley startups).

This is all now going into reverse. The Fed is allowing the bonds it bought to mature and isn’t buying new ones; its assets have been declining slowly. It’s not sucking money out of the markets, but it’s not pumping in a trillion a year anymore, either. And the likely trajectory for interest rates is modestly higher this year and beyond. Markets love easy money (as long as workers aren’t getting a piece of the action), and they were always going to have to get use to harder money. The wage spike made it seem like money was going to get harder more quickly than they’d thought.

meaning

How much does this matter? It’s quite possible the market could recover. The selloff was intensified by algorithm-driven trading; that could turn around. But at some point high valuations will revert to the mean, or worse, and that is often not a calm process. Higher interest rates breed bear markets and, eventually, recessions.

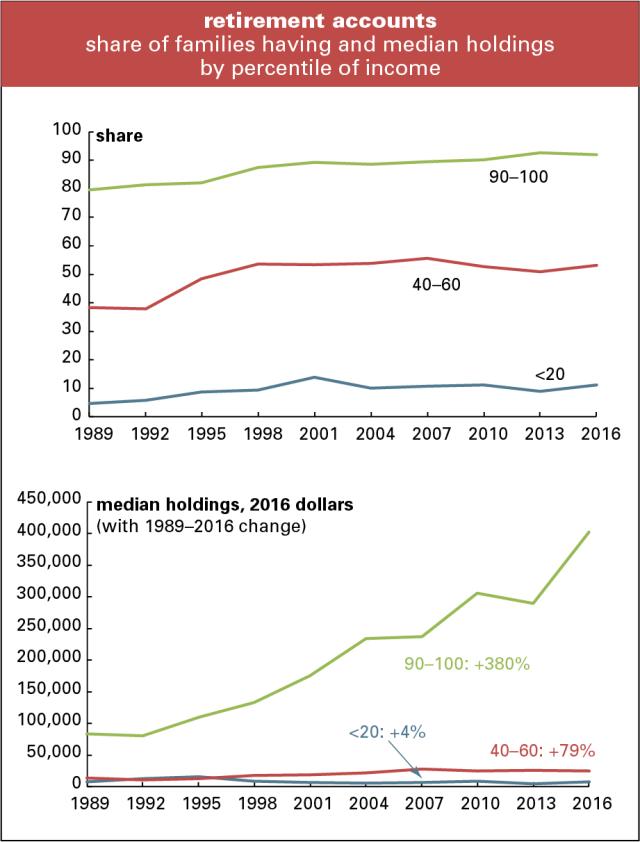

For most people, the direct, immediate effects of the stock selloff are minor. Though Trump kept urging people to check their 401(k)’s for proof of his excellence, only half (52%) of the population has a retirement account, and of those that hold one, its median value is $60,000. (These numbers come from the Fed’s triennial Survey of Consumer Finances.) More broadly, only about half the population (51%) owns stock, either directly or through a mutual fund; the median holding is $40,000. People in the middle of the income distribution own $15,000 worth of stock.

As the graphs below show, even retirement accounts, which are supposed to be more “democratic” than the stockholdings of the rich, skew massively upwards. Among the richest tenth, 92% have retirement accounts; among the poorest fifth, just 11% do. The top tier’s median holding is $403,000, up 380% from 1989; the bottom’s, is $7,800, up 4%.

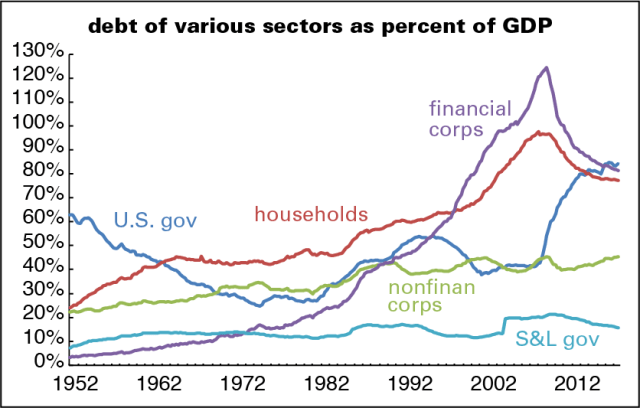

But a stock market crash can do damage if it’s deep enough, or if it’s a symptom of problems in the credit system. The market tanked during the 2008 financial crisis, but the reason that we lost almost nine million jobs during the recession was the implosion of the credit system. Banks wouldn’t lend and even solvent individuals and businesses didn’t want to spend, much less borrow. The driving force of the crisis was the unwinding of the mortgage boom, made worse by all the clever financial products it spawned. Things don’t seem so dire now (though you never know).

As the graph below shows, household debt, mostly mortgages, soared during the mid-2000s boom, as did that of the financial corporations that made and repackaged those mortgages. That went into reverse after the crisis and hasn’t gotten going again. Aside from the federal government, the only major sector that has been bold with debt since the crisis has been nonfinancial corporations, who’ve been borrowing despite all the transfers to their shareholders reported above. (Some of that borrowing goes to fund the transfers—stock buybacks and takeovers—which doesn’t seem prudent.) No doubt there are some stinkbombs hidden in the financial system—derivatives we won’t understand until months after they blow up, say—but overall the credit system doesn’t look as vulnerable to a total meltdown as it did then.

But what hasn’t happened is coming up with a new model for the economy. With the Reagan years came a war on labor—the busting of unions, the repression of wages, the war on our meager welfare state—a war whose gains were consolidated in the Clinton years, as the Democratic party was turned into a pure business party. With household incomes under pressure, people used credit cards and mortgages to fund the semblance of a middle-class standard of living. The financial crisis busted that model apart. Household incomes are still under pressure, but money has been far less easy for the middle and lower ranks than it has been for the upper. Slow growth and popular rage are the result.

When stocks were falling hard, left social media lit up with predictions (laced with hope) that this was It—It being the crisis that was finally going to wake people up and foment rebellion. That’s not the way things usually work. The U.S. got more civilized in the 1930s thanks to the New Deal but you can’t say that about Germany. Crises often drive people to the right not to the left.

I don’t think a rerun of the 2008 meltdown is in the cards. But whether you measure by conventional indicators, like GDP and productivity growth, or more humane ones, like the capacity to deliver a decent and stable standard of living to people with less than six-figure incomes, this economy is anything but strong. Signs of wage increases should not be occasions for panic, but when the economy is organized around the needs of the top 10%, they are.

Bosses getting raises, working stiffs not

Stock markets have been swooning, in no small part because last Friday’s U.S. employment report showed that average hourly earnings (AHE)—the average wage, excluding benefits, received by private sector workers—rose smartly in January. This prompted fears that inflationary pressures are mounting, wages will eat into profits, and the Federal Reserve might raise interest rates more aggressively than had been thought as recently as last Thursday. Or, as the New York Times put it in a headline, with its patented mix of dullness and alarm:

What these scaremongers aren’t telling you is that it’s only bosses that are getting the raises.

Here’s a graph of the yearly growth in AHE.

You may notice that this series begins in March 2007. That’s because the Bureau of Labor Statistics (BLS) only started reporting hourly earnings for “all workers” in March 2006. It has been reporting monthly AHE stats for “nonsupervisory” or “production” workers since 1964. Nonsupervisory workers—defined by the BLS as “those who are not owners or who are not primarily employed to direct, supervise, or plan the work of others”—are about 82% of the private sector workforce, a share that has hardly changed over the last 53 years.

Most Wall Street analysts have been focusing on the all worker series, because it’s broader, and because many of them have a hard time thinking about more than one thing at a time. And if you’re looking to alarmed about something, you can find a rising trend in the graph above. Yearly wage growth (not adjusted for inflation) hit a post-recession low of 1.5% in October 2012; in January 2018, it rose to 2.9%, the highest in almost nine years. Yes, the number is noisy, but there’s no mistaking the rising trend.

But those who’ve been panicking about a wage explosion haven’t bothered to look at the nonsupervisory series. That has shown no rising trend at all over the last two years. AHE for nonsupervisory workers were up 2.4% for the year ending in January—just as they were in December, and less than September 2017’s 2.6%. In January 2016, the gain was 2.4%. In other words, for more than four out of five private sector workers, there’s been no acceleration in wage growth—which, by the way, is barely ahead of inflation.

The BLS doesn’t report AHE for supervisory workers. But since we know the nonsupervisory share of the workforce and the all-worker and nonsupervisory AHE numbers, we can estimate what the supervisory wage looks like with some middle-school math. Here’s a graph:

For the year ending in January, supervisory wages were up 3.9%, compared with 3.0% in December. Over the last three months, supervisory wages are up 6.4% at an annual rate. (In January, nonsupervisory wages averaged $22.34, and the lbo-news estimate of supervisory earnings was $47.35.) In 2015 and 2016, both series moved pretty much together, but the boss sector began pulling ahead of the bossed in early 2017, and the gap has been widening since.

The series does bounce around a lot, and it’s quite possible that some of the January spike will be reversed in February. But the central point is this: the alarming acceleration in wages is not a mass phenomenon. It’s for the $95,000 a year set, not the $45,000 crew.*

*Yearly earnings are based on 2,000 hours a year times the relevant hourly wage.

Fresh audio product

Just uploaded to my radio archive (click on date for link):

February 1, 2018 David Palumbo-Liu on the right-wing attacks on him and on academic freedom (the Stanford Politics article on the Thiel network is here) • Jodi Dean on how to think about Trump

Fresh audio product

Just added to my radio archive (click on date for link):

January 25, 2018 Vijay Prashad on Syria, Trump, and the state of the global left • Jennifer Cohen of Miami University on feminism and economics (the NYT article is here)

Fresh audio product

Just added to my radio archive (click on date for link):

January 18, 2018 Sandra Cuffe on Honduras after a stolen election and waves of official violence • Alexander Main on U.S. policy towards Latin America under Trump • Janet Capron, author of Blue Money, on drugs and prostitution (without regret) in 1970s NYC

Janus risk

Chris Maisano reminded me on Facebook of something I forgot to mention in today’s union density post—the forthcoming Supreme Court decision in the Janus case. I appended this to the closing paragraph of the original:

A major threat to that [getting union density up]: the forthcoming Supreme Court decision in the case of Janus v. AFSCME, which would make public sector union dues optional. Should the Court decide against the union, which is almost certain given the configuration of the cast of robed ghouls, many workers would stop paying dues and not bother to join the union, and the “public” line will, as they say on Wall Street, accelerate to the downside.

Shocker: unions hold their own

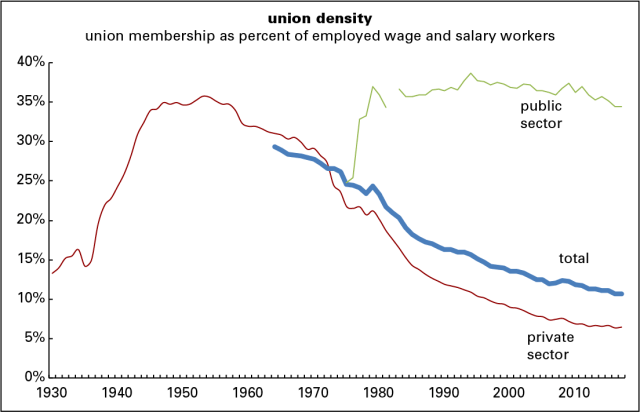

Unions had a pretty good year in 2017: they didn’t lose any ground.

According to the latest edition of the Bureau of Labor Statistics annual survey, released this morning, 10.7% of employed wage and salary workers were members of unions, unchanged from last year. There was a mild uptick in the share of private-sector workers represented by unions (aka union density), from 6.4% to 6.5%. Density was unchanged at 34.4% for public sector workers—mildly surprising, given the war on labor being conducted by Republican governors and legislatures across the country.

As the graph below shows, 2017’s flatness is a bit of stability amidst a long-term decline; we saw similarly unchanged density readings in 2013 and 2015. While the rate of decline has slowed from the rapid rates of the 1980s and 1990s, density for private-sector workers was down 1.0 percentage points from 2007 to 2017; for the public sector, it was down 1.5 points. Declining density is not new to the public sector—it peaked in 1994 at 38.7%, 4.3 points above last year’s reading—but the pace of slippage has accelerated over the last five years or so.

Declining union density is bad for at least two reasons: it’s bad for working-class power and for living standards. Yes, most unions are weak subordinates of the Democratic party establishment, serving as little more than ATMs and get-out-the-vote operations for boring candidates who do little for their labor supporters once elected. But they do serve as a brake on the political class’s most barbaric instincts, which is why politicians like Scott Walker and moneybags like the Koch Bros. (who funded Walker’s anti-union drive in Wisconsin) have it out for them.

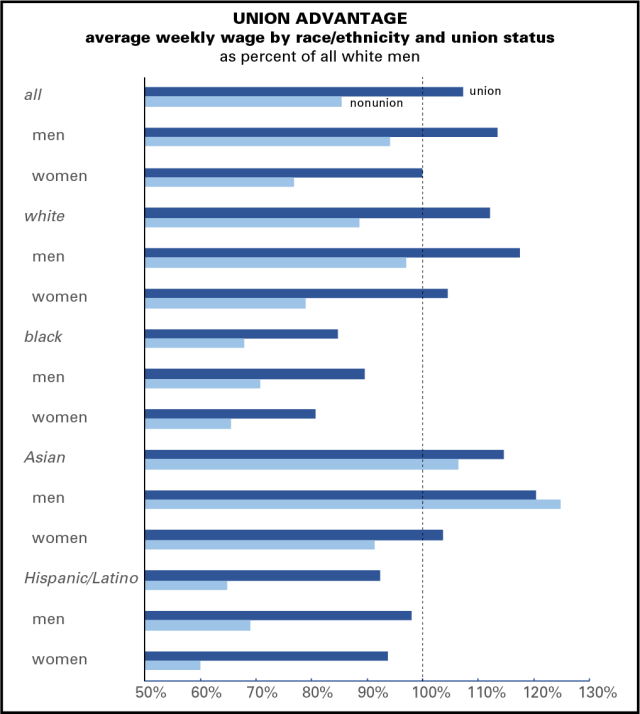

And, as the graph below shows, unions bring higher wages—especially for workers who are neither white nor male.

For example, black men who are not in unions earn 71% as much as all white men (union and nonunion); with a union, that rises to 89% as much. For black women, the numbers are 65% for nonunion and 81% for union. For what the BLS calls Hispanic or Latino workers the union boost is even sharper: from 69% of white men for nonunion men to 98% for unionized ones, and from 60% for nonunion women to 94% for union. Unions also narrow gender gaps. Nonunion women of all races/ethnicities earn 82% as much as men; that rises to 88% for unionized women. Unions add 21% to the average weekly wage for men, and 30% for women. In other words, unions reduce inequality along all the familiar demographic axes—and make it harder to pit workers against each other.

Admittedly, the nonunion/union figures compare workers across a variety of occupations, sectors, and regions; a more rigorous analysis would control for those differences to isolate the union effect alone. (There’s a version of that here.) But even after controlling for those things, you’d still find a substantial union wage advantage of 10% or more—not to mention far better health, retirement, and vacation benefits and greater job security, things not captured by weekly wage stats.

There are good reasons employers hate unions, which is why we need to get those union density graphs pointing upwards. A major threat to that: the forthcoming Supreme Court decision in the case of Janus v. AFSCME, which would make public sector union dues optional. Should the Court decide against the union, which is almost certain given the configuration of the cast of robed ghouls, many workers would stop paying dues and not bother to join the union, and the “public” line will, as they say on Wall Street, accelerate to the downside.

Sources: 1930–1999, Barry T. Hirsch and David A. Macpherson; 2000–2017, BLS

Market timing, lbo-news style

As I’m typing this, bitcoin is having another terrible day, trading at $10,050, down 11% from yesterday and 48% from its all-time high of $19,290. (For the latest price, click here.) Of course, it also had a spectacular upward run. On August 17, 2010, when the cryptocurrency’s price history begins, it was worth $0.08. Four-and-a-half months later, January 1, 2011, when the chart just below begins, it was worth $0.30, a gain of 290%. A year later, January 1, 2012, it traded at $5.20, a gain of 1,633%. Five years later, January 1, 2017, it had tacked on another 19,087%, taking it to $998.

But it was only warming up, which is why that 1,297,338% move from $0.08 to $998 looks so trivial next to what followed. (In dollar terms, that is. The right edge would look much less dramatic on a logarithmic chart, which would be all about percentage changes, but that would be a lot less fun.) BTC had a very good year in 2017, peaking on December 17 at the above-mentioned $19,290, a gain of 1,833% for the year, and 25,084,146% since birth. If you’d bought $1,000 worth of bitcoin at its birth, it would have been worth over $250,000,000 at its all-time high (so far)—though if you tried to sell it, the price probably would have collapsed. This is not a deep market.

But this overture has distracted from the real point of this post: celebrating lbo-news’s market timing. The graph below is a close-up of the bitcoin action since October 2017, with three crucial dates marked on the graph: the date the first article on BTC was posted here, the all-time high, and the date the second BTC article was posted here. The posting dates bookend the high almost perfectly. Unlike our president, who seems to think that everything good that happens is his doing, lbo-news will claim no credit for bitcoin’s fall.

Fresh audio product

Just added to my radio archive (click on date for link):

January 11, 2018 Kaveh Ehsani on the reasons behind the protests in Iran • Franklin Zimring, author of The City That Became Safe, on the reasons behind the record-breaking decline in crime in NYC

Pacifica to file for bankruptcy?

Pacifica update: Bill Crosier, the network’s interim executive director (they’ve all been interim for years, since they can’t formally choose a permanent one) has decided to call for a bankruptcy filing, reminding directors who try to obstruct the move they could be personally liable for a breach of fiduciary duty. It wouldn’t surprise me if half the board members don’t know what that means.

[Weirdly, Facebook won’t let me post the resolution itself, just Crosier’s email.]

Subject: Bankruptcy motion – It’s time

Date: Wed, 27 Dec 2017 21:45:43 -0600

From: Pacifica Executive Director <ed@pacifica.org>

To: Pacifica National Board <pnb@pacifica.org>

Cc: Sam Agarwal_Pacifica_CFO <sagarwal@pacifica.org>, Ford Greene <fordgreene@comcast.net>

Dear PNB Directors,

Attached is a resolution for authorizing to file for Chapter 11 Bankruptcy and Reorganization. As is clear, we have exhausted all options at this time to secure a loan or to pay the ESRT [Empire State Building] judgment or to secure a forbearance agreement. Three attorneys have told us, in very clear terms, that Pacifica’s assets are in imminent danger of being liened or seized, some of which may happen today.

We have no written forbearance agreement of any kind with ESRT. They have a judgment against us and have filed in every state where we operate. Now that we are at this point, we must file chapter 11 to protect Pacifica’s assets, so we can continue operations.

All directors have a fiduciary responsibility to protect the Foundation’s assets. This decision has been blocked and delayed for a long time and cannot be delayed any further. Time has run out. Various delinquencies and financial distresses cannot be ignored. So, I urge my colleagues to do the right thing. Still, we can salvage and come out of this crisis. But later, we will not be able to do so. Waiting until Jan. 8 will be too late, as that’s when all the California properties will be at risk. Our other assets, including our bank accounts, are already at great risk of seizure.

As this issue is of critical importance to Pacifica, I am copying all Local Station Boards, the National Finance Committee, Audit Committee, and General Managers and Business Managers to keep them informed.

Please note that any attempt to block or unnecessarily delay this motion will be taken very seriously. As a follow up to our meeting with the California Attorney General Charitable Trusts Division, the officers would forward the outcome of this motion to their office with voting results. Directors may be held personally responsible for conscious disregard of their duties. Damages now can be very clearly specified and it will be the loss of property, interest and legal costs.

I’m sorry to have to put this so bluntly, but this is very important – perhaps the most important thing the PNB has had to do, to protect Pacifica.

Now is the time. We cannot wait any longer.

Bill Crosier

William G. (Bill) Crosier

Interim Executive Director

Pacifica Foundation

1925 Martin Luther King Jr Way

Berkeley CA 94704-1037

510-316-9783

The motion:

*Pacifica Bankruptcy Motion*

WHEREAS, on October 4, 2017, the Honorable Gerald Lebovits of the Supreme Court of the State of New York, granted summary judgment in the amount of $1,819,687.52 with interest and reserving attorney’s fees and court costs, in favor of plaintiff, in /ESRT Empire State Building (Empire State) L.L.C. v. Pacifica Foundation, Inc./, Case No. 656145/16, for the failure of Station WBAI to stay current on its lease payments for its broadcast antennae located on the Empire State Building in New York, New York;

WHEREAS, on November 16, 2017, the Clerk issued Judgment (“Judgment”) in the amount of $1,839,586.19 in /ESRT Empire State Building L.L.C. v. Pacifica Foundation, Inc/., reserving attorney’s fees and interest;

WHEREAS, on December 7, 2017, Empire State filed its Application for Entry of Judgment on Sister State Judgment in Los Angeles County Superior Court, Case No. BS 171750 and on December 12, 2017, personally served the same on Pacifica Foundation’s National Office, 1925 Martin Luther King Way, Berkeley, California (“National Office”);

WHEREAS, on December 7, 2017, Empire State served on the National Office and filed its Request to File Foreign Judgment in Superior Court of the District of Columbia, Case No. 17-0008138, in the amount of $1,839,586.19 at the rate of 9% interest;

WHEREAS, on December 11, 2017, Empire State served on the National Office and filed the Notice of Filing of Foreign Judgment in the District Court of Harris County, State of Texas, Case No. 2017-80997, in the amount of $1,839,586.19;

WHEREAS, Empire State has taken the steps necessary to start to execute its $1,839,586.19 Judgment in the states of New York, California, Texas and Washington D.C.;

WHEREAS, Pacifica Foundation owns real property free and clear and five broadcast licenses, but does not have sufficient operating capital and reserves to pay the Judgment;

WHEREAS, Pacifica Foundation maintains real property and bank accounts in the states of New York, California, Texas and Washington D.C. which are at risk for being levied upon, liened against and seized;

WHEREAS, Empire State may execute its Judgment on bank accounts owned by Pacifica Foundation at any time;

WHEREAS, Empire State can record an Abstract of Judgment in California on Monday, January 8, 2018, which will become effective against real property in California;

WHEREAS, if Pacifica Foundation fails to file a petition for bankruptcy reorganization pursuant to Chapter 11 of the U.S. Bankruptcy Code on or before Friday, January 5, 2018, in California, and Empire State records an Abstract of Judgment on Monday, January 8, 2018, it will create a Judgment Lien which will become effective as against real property Pacifica Foundation owns and unnecessarily and unduly compromise Pacifica Foundation’s position in bankruptcy court;

WHEREAS, the recordation of an Abstract of Judgment in California will trigger the creation of a Judgment Lien that will entitle Empire State to add interest and attorney’s fees to its Judgment Lien and otherwise improve its position and damage Pacifica’s assets;

WHEREAS, for close to six months Pacifica Foundation has requested Empire State to sign a Forbearance Agreement in writing whereby Empire State would promise for a time certain not to execute its judgment and otherwise increase its legal advantage over the Pacifica Foundation by promising not to record an Abstract of Judgment or take any other steps to perfect a Judgment Lien or enforce the Judgment for the forbearance period, and Empire State has refused and continues to refuse to do so;

WHEREAS, Pacifica Foundation has failed to make any further monthly antennae lease payments to Empire State since May 2017 and will continue such failure into the foreseeable future;

WHEREAS, as of December 1, 2017, Pacifica Foundation’s monthly payment to Empire State is $60,991.16 and will continue to increase in amount every month thereafter until the lease expires in 2020;

WHEREAS, Pacifica Foundation cannot afford to make the ongoing and continuing monthly Empire State lease payments for the location of the WBAI broadcast antennae;

WHEREAS, Pacifica Foundation has failed to fund the retirement plan for its employees since FY2015 and owes said plan approximately $750,000

WHEREAS, due to Pacifica Foundation’s lack of compliance in funding its retirement plan for its employees, on December 12, 2017, the Newport Group, Inc., the manager of the plan “disengaged” effective immediately;

WHEREAS, Pacifica Foundation has mismanaged its fiscal responsibilities for a period of many years that has resulted in the accumulation of millions of dollars of debt;

WHEREAS, Pacifica’s Foundation’s credit rating is damaged, flawed and poor such that it can become eligible for cash loans only on the riskiest and most harsh terms for which it has no articulated plan for repayment and which necessarily would be secured by real property that Pacifica owns;

WHEREAS, the Pacifica Foundation has an ongoing duty to submit yearly independent financial audits to the California Attorney General Charitable Trusts Division on a timely basis;

WHEREAS, the failure of Pacifica Foundation to timely submit yearly independent financial audits to the California Attorney General Charitable Trusts Division will result in the revocation of its tax-exempt status;

WHEREAS, the Pacifica Foundation cannot operate without remaining a non-profit corporation with a valid tax-exemption in good standing in the State of California;

WHEREAS, on May 22, 2017, the California Franchise Tax Board revoked the Pacifica Foundation’s tax exemption for failing to timely submit yearly independent financial audits, which status was subsequently reinstated when Pacifica Foundation submitted its independent financial audit for FY2015 to the California Attorney General Charitable Trusts Division in August 2017;

WHEREAS, Pacifica Foundation has a fiduciary duty to protect its assets, not to expose its assets to undue and unnecessary risk and to exercise sound fiscal management looking into the future;

WHEREAS, the Pacifica Foundation has no other present means by which to protect its assets from imminent levy, lien and seizure;

WHEREAS, the most effective way for the Pacifica Foundation to effectively protect its assets is by filing a petition for bankruptcy reorganization pursuant to Chapter 11 of the U.S. Bankruptcy Code on or before Friday, January 5, 2018;

WHEREAS, in order to file a petition in bankruptcy and to successfully do the work that is necessary to a successful use of bankruptcy protection, the National Office in Berkeley, California must gather information from the member radio stations in New York, Washington D.C., Texas and California;

WHEREAS, the National Office and bankruptcy counsel will have to work in close and continuing cooperation and that physical proximity best facilitates such ongoing cooperation;

WHEREAS, bankruptcy specialists, Reno F.R. Fernandez III, Philip E. Strok, and Pacifica General Counsel Ford Greene continue to advise and recommend Pacifica Foundation to file a petition for bankruptcy reorganization pursuant to Chapter 11 of the U.S. Bankruptcy Code on or before Friday, January 5, 2018;

WHEREAS, in order to accomplish the continuing work that submitting yearly independent financial audits requires, to continue to exercise accountable fiscal responsibility across the Pacifica Foundation’s radio network and to gather the foundational documents, records and financial data that maintaining a bankruptcy filing will require, Pacifica Foundation must authorize the hiring of additional employees to assist CFO Sam Agarwal;

NOW THEREFORE, it is hereby moved that the Pacifica National Board authorize its Executive Director William G. Crosier and/or Chief Financial Officer Sam Agarwal to employ the law firm of MacDonald Fernandez LLP to file a petition for bankruptcy reorganization pursuant to Chapter 11 of the U.S. Bankruptcy Code on or before Friday, January 5, 2018;

NOW THEREFORE, it is hereby moved that the Pacifica National Board authorizes Chief Financial Officer Sam Agarwal to employ two contractors to assist in discharging the tasks set forth herein above.

Pacifica death watch: this time it’s really real

Because WBAI is broke, almost listenerless, and run by idiots, the station didn’t pay its transmitter bill to the Empire State Building for a long time, and is now $3 million in arrears. The ESB has sued and wants to seize Pacifica’s assets, which would include KPFA and KPFK’s bank accounts and buildings.

Because the Pacifica board is staffed by idiots, the network is not filing for bankruptcy or taking any other meaningful measures to protect itself. The rational thing to do would be to sell WBAI’s frequency (at 99.5, it’s on the commercial section of the radio dial), because the station is braindead and pointless, and the proceeds could save the rest of the network. But that doesn’t seem to be happening.

There’s a high risk that KPFA — where Behind the News originates — will stop broadcasting on January 12. I don’t know what that means for the future of BtN, but aside from that, the loss of KPFA would be tragic.

It’s taken years to get to this point. If you wanted to destroy the network, you couldn’t have done any better than make Tony Bates the WBAI program director and Berthold Reimers the general manager. And you couldn’t have done any better than staff the board with people who have no idea of how to run anything. It would be premature to type “RIP,” but it’s not too soon to make what delicate people call “arrangements.”

A note on the topic from the KPFA manager follows.

I’ve held off writing this depressing message as long as I could in an effort to gather as much information and analysis possible while working with current and former LSB members in trying to protect KPFA’s interests in this grim situation we find ourselves in.

Because of Pacifica’s critical financial condition and the PNB’s lack of strategic action or courage the prognosis for the network’s future is shadowy.

*The Imminent Threat*

Come *January 12th *KPFA’s money and property may be seized by the Empire State Realty Trust because of a 1.8 million dollar debt of our sister station WBAI.

If this happens we will cease broadcasting because we will be unable to operate the station. At that point, our building and our bank account will no longer be under our control. Needless to say, this is a terrible position to be in, especially for management when there is *still* no plan of action to articulate from the National leadership to the staff.

*How Did This Happen?*

• WBAI owes the Empire State Realty Trust 1.8 million dollars in delinquent transmitter rent. [Plus more delinquent rent since April, not covered in the suit.] ESRT filed in court against Pacifica on November 23rd, 2016. Their monthly rent is currently at $53K per month escalating each month.

• On October 4 a judge found in favor of ESRT making it possible for them to file in all states where Pacifica has properties, allowing them to seize money and property.

• The idea of a signal swap for WBAI was ignited and brokers were hired.

• The PNB voted to give IED the authority to begin preparation for Chapter 11 bankruptcy protection, but he and many others on the PNB thought to sell properties (like our two adjacent buildings) and others could cover the debt. The other idea was a high-interest loan that so far has never been secured. All of these instead of the signal swap in New York.

• Then the PNB rescinded the bankruptcy resolution. Also, KPFA and KPFK signals were added for signal swaps.

• ESRT judgment filed in California on December 6th to seize property and money from KPFA and K. It is a 30-day waiting period that ends January 12h.

• Then the PNB voted to allow some prep for Bankruptcy.

• At PNB meeting 2 weeks ago California’s Deputy Attorney General, Julianne Mossier spoke at the meeting and made it clear that the board needed to vote to take action immediately and that anyone who obstructs for any personal reasons were liable for not carrying out their fiduciary duties.

• The board ignored her plea, but set up an emergency meeting about moving ahead with bankruptcy the following Monday but no action was taken.

• The clock is ticking…

*What is Being Done?*

I want to thank all the LSB members who have worked so diligently this year negotiating with the PNB in good faith to move the network in a positive direction while also protecting KPFA’s interests.

Because of the imminent threat of a lien on KPFA’s bank account, we have disbursed in advance (what is legally allowed) our payroll account to Dec 31 st., medical benefits till February and all of our essential bills are paid. In the first week of January, we will process advance payroll for January and pay another month of medical. I’m sorry to say that is all management can do. There still is no playbook for a month or two months down the road.

What is the PNB doing? The governance structure of Pacifica, our historic culture of the usual political infighting, etc., has led to disagreement and paralysis. Unless action is taken pretty immediately we may cease to exist. You deserve to understand where things stand. I could wait no longer.

Much respect,

Quincy McCoy

General Manager

Fresh audio product

Just added to my radio archive (click on date for link):

December 21, 2017 DH on bitcoin • Yanis Varoufakis ties up some loose ends on Adults in the Room, and then discusses the need for a progressive internationalism

Is Bitcoin the future of money?

This originally appeared in The Nation, April 30, 2014, issue. With Bitcoin now having migrated from obscurity to headlines (though I said “all over the headlines” then, it’s really broken into the bigtime now), I thought I’d repost it here, since it’s behind a paywall. My BTC 0.05 would be worth $862.50 as I’m posting this, but I sold it, alas.

Is Bitcoin the future of money

Doug Henwood

What’s being touted in some circles as the future of money looks hardly more peaceful than its past. Bitcoin, a formerly obscure cyber-currency, is now all over the headlines with reports of bankruptcies, thefts and FBI lockdowns. If our fate is to buy and sell in bitcoins, this instability is troubling. But despite the headlines, the triumph of Bitcoin and related cyber-currencies is a lot less likely than recent commentary would suggest. One cause of all this hype? The number of people who understand what Bitcoin is seems almost immeasurably small—and that probably includes some of its users.

Money, it should be conceded, is not a simple topic. Most people understand how gold, which is something of a primal money, is mined, refined and shaped into coins. It is rare, pure, easily divisible and has been cherished over the centuries. Paper money is more complex. From 1900 through 1971 (with the exception of during World War I), the US dollar was backed by gold, meaning its value was legally defined by a certain weight of the metal. That ended in 1971, when Richard Nixon shocked the world by breaking the link to gold and allowing the dollar’s value to be determined by trading in the foreign exchange markets. The dollar is valuable not because it’s as good as gold, but because you can buy goods and services produced in the United States with it—and, crucially, it’s the only form the US government will accept for tax payments. Among the Federal Reserve’s many functions is allowing the issuance of just the right quantity of dollars—enough to keep the wheels of commerce well greased without slipping into a hyperinflationary crisis.

But Bitcoin (capitalized as a concept, lowercased when referring to units of the currency, according to American Banker) is another animal entirely. It is the first and most famous of a large and growing family of so-called “cryptocurrencies.” Others include Litecoin, Feathercoin, Songcoin (“designed for The Music Industry”), Auroracoin (Iceland only) and Dogecoin (“the fun cryptocurrency”)—but Bitcoin is by far the largest. Its origin is traced to a 2008 paper written by the pseudonymous Satoshi Nakamoto. Newsweek recently claimed to have located the real one, but he promptly denied all, so the whole thing remains quite mysterious.

According to its semi-official definition, a crypto-currency is “a peer-to-peer, decentralized, digital currency whose implementation relies on the principles of cryptography to validate the transactions and generation of the currency itself.” (While that is one dense slab of prose, to be fair to the cryptoids, it wouldn’t be easy to define the dollar succinctly either.) What this means is that Bitcoin and the rest are electronic currencies created and transferred by networked computers with no one in charge. The role of cryptography is not merely to guarantee the security of the transaction, but also to generate new units of the currency, which are “mined” by having computers solve complicated mathematical problems. Once solved, new coins are created and their birth—with digital signatures guaranteeing authenticity and uniqueness—announced to the rest of the system. The creator earns the value of the new coins when they enter the system.

Trading is done via exchanges, which communicate with other exchanges, but there is no central authority. Some trading is done online, but you can also buy bitcoins for cash in person.

The mining requires enormous amounts of computing power, though specialized processors have been developed to reduce power consumption, which in turn produce many tons of carbon. Even the most ephemeral coin has material roots.

That’s the technology of bitcoin; but is it money? The classic economist’s definition holds that money is a store of value, a unit of account and a medium of exchange. You go to the store and find that a can of tomatoes is priced at $3—a unit of account, which the store will book as revenue once it’s sold. You take $3 out of your pocket or via your debit card—you draw down the store of value (cash on hand or in the bank) and use it as a medium of exchange. The value of the US dollar is that everyone in the United States, and beyond, recognizes the currency as fulfilling these tests of money. The dollar is valorized by the goods and services that it can buy.

Bitcoin has serious problems in all three respects. From the beginning of 2013 through early February 2014, the price of a bitcoin has varied from $13.40 to $1,203.42—a ratio of 90 to 1. Its average one-day change (ignoring whether it was up or down) was 4.3 percent. In just one day last April, Bitcoin lost 48 percent of its value relative to the US dollar—and that came the day after it lost 33 percent. But by November 2013, Bitcoin had shaken off this case of nerves and risen 1,405 percent off that crash low. By contrast, the ratio of high to low in the Federal Reserve’s broad index of the US dollar’s international value was just 1.07 to 1. Its biggest one-day move was under 2 percent; its average one-day change was 0.3 percent. (The dollar’s biggest daily change was less than half of Bitcoin’s average daily change.) Yes, inflation has steadily eaten away at the dollar’s value, but in relatively steady and predictable ways over the decades. It does not gyrate by almost 50 percent in a day. So much for a store of value.

Almost no one accepts payment in Bitcoin, nor do any businesses of note keep their books in Bitcoin; it fails both as a unit of account and a medium of exchange. And its short history—the first bitcoins were minted in 2009—has been turbulent. The US government seized funds from Mt. Gox, then the largest Bitcoin exchange, in May 2013, and just this past February, Mt. Gox collapsed from an undetermined mix of theft, fraud and mismanagement, leaving hundreds of millions of dollars in losses in its wake. There have been many other reports of thefts, frauds and hackings, which Bitcoin partisans dismiss as mere growing pains. But with no regulator, no deposit insurance and no central bank, this sort of thing is inevitable—it’s just tough luck. Introduce regulators and insurance schemes, though, and Bitcoin will lose all its anarcho-charm.

Keynes once called gold “part of the apparatus of conservatism” for its appeal to rentiers who loved austerity because it preserved the value of their assets. Bitcoin serves a similarly totemic purpose for today’s cyber-libertarians, who love not only the statelessness of it as money, but also its power to subject the institutional banking system to “disruption” (one of the favorite words of that set). And like gold, Bitcoin is deflationary. There’s a limit on how many bitcoins can be produced, and it gets more difficult to produce them over time until that limit is reached. Of course, new cryptocurrencies could arise. But the existence of the limit reflects the deflationary sympathies of the libertarian mind—in a Bitcoin economy, creating money to ease an economic depression would be impossible. Which is not to say that only libertarians love Bitcoin.

* * *

To catch a glimpse of cyber-libertarianism in its natural habitat, I ventured to a December 19 holiday party organized by Cryptos.com, a business incubator for Bitcoin startups; BitcoinNYC, a meetup group; and Halfmoon Labs, which builds trading platforms. I was hoping to find some wildly anti-statist libertarians, and my hopes were further stoked by the first person I saw upon entering—a tall, skinny man with a red bow tie, the very picture of an Ayn Rand adept.

But it was not to be. Though the air wasn’t free of libertarianism, most of the partiers I talked with were interested in running Bitcoin-related businesses or speculating in the currency. Many had day jobs in tech or finance. It was mostly male (but not overwhelmingly so) and mostly white. Only one person was wearing Google Glass. From national surveys of unproved rigor, your typical Bitcoin enthusiast is a 30-ish libertarian white male—though the same survey finds 39 percent of the fan base leftish in some sense. The group at the holiday party, probably because of its business-y skew, was somewhat more diverse.

Cryptos.com founder Nick Spanos worked two cellphones. When I introduced myself and turned on my iPhone voice recorder, Spanos was not cooperative: “I don’t talk to reporters I don’t know. Turn the thing off.” After I did, he told me the place was filled with Bitcoin millionaires—ten of them under 21. When I asked what kinds of businesses they were in, he replied: “All kinds.” That was the end of the interview—a cryptopromoter for a cryptocurrency.

Another partier, Marshall Swatt, the chief technology officer at Coinsetter, a Bitcoin trading platform for institutional investors, was more helpful. Swatt told me that, after building trading platforms for established Wall Street institutions, he was looking for something more entrepreneurial. When I asked him whether Bitcoin was money or a trading asset, he said it was an open question. (In late March, the IRS ruled that Bitcoin is an asset, not a form of money, and that mining and trading gains are subject to income tax.) Bitcoin would need to develop a large consumer market to be taken seriously as currency. Swatt thinks it will: Virgin Galactic, Richard Branson’s scheme to take tycoons into space, accepts Bitcoin. But that’s by nature a small market. To get taken seriously, Swatt would love to see Bitcoin adopted by Google, Amazon, Facebook and Apple. Asked to explain its appeal, Swatt replied that it’s an “extremely well-crafted device,” secure and mobile. Unlike many Bitcoin enthusiasts, Swatt doesn’t talk trash about gold or fiat currencies—he sees it as a complement to state money. It’s deflationary like gold, but like money (and unlike gold), it’s easy to use. He predicts a trillion-dollar volume in Bitcoin someday, though with the supply so tightly limited, that would send the value of a single coin through the roof.

* * *

Bitcoin’s limitations as a currency may be why most of the world’s central banks have tolerated it. States are fond of their monopoly over money. Federal Reserve chair Janet Yellen said in late Feburary, right after the Mt. Gox collapse, that the Fed lacked the authority to regulate Bitcoin because it’s outside the banking system. The Danish central bank stated in a press release: “Bitcoins are not money in a proper sense as there is no issuer behind them. Instead, bitcoins display the characteristics of a commodity to which users attach value. Unlike precious metals such as gold and silver, bitcoins have no actual utility value, bearing closer resemblance to glass beads.” The bank found the market too small to worry about; all the risks are on a small number of participants. And the market is very small: the value of all bitcoins outstanding is $5.9 billion—0.05 percent the size of the US money supply (by the Fed’s M2 definition).

Two Goldman Sachs economists, Dominic Wilson and José Ursua, largely concurred with the Danish evaluation. “We would argue that Bitcoin and other digital currencies lie somewhere on the boundary between currency, commodity and financial asset. Our best definition would be that it is currently a speculative financial asset that can be used as a medium of exchange.” But they also make an important point: the peer-to-peer technology behind Bitcoin could become a model for moving money around without third-party verifiers, like banks.

Bitcoin is not without friends on Wall Street. Gil Luria of Wedbush Securities is following it; he describes the recent volatility as “extended price discovery,” which is a way of saying that no one knows what it is, what it will be or what it’s worth. His firm is selling his Bitcoin research for payment in bitcoins.

* * *

The political cast of the Bitcoin universe is mostly libertarian, but it does have a left wing. These users celebrate Bitcoin’s evasion of state surveillance and policing—which, in the post-Snowden era, is nothing to sneeze at.

Take sex workers, often subjected to outrageous degrees of scrutiny. A Marxist-feminist professional dominatrix who practices in Britain under the name Mistress Magpie is an enthusiastic Bitcoin proponent. She explains her enthusiasm as beginning with her deep techno-geekiness, and adds that Bitcoin is also practical for someone in her line of work—anonymity is important, whether operating in real life or online. Unlike libertarians, who see cryptocurrencies as a possible gateway to a new society, the socialist in Mistress Magpie sees them as a way to operate furtively under capitalism, in a way that might not be needed in a more open socialist society. Even for her, though, Bitcoin doesn’t go far—the majority of her clients are not well versed in digital currencies. Furtive payment is also good, of course, for drugs and other illegal procurements—a sort of anarchic market operating beyond regulation. Though the FBI shut down Silk Road, the online mall of illicit goods, its offspring live on. A friend whose politics are well left of center—and not unusually anti-statist either—loves that he can pay for DMT (a short-acting hallucinogen) using bitcoins in an encrypted transaction.

Apart from anonymity, though, it remains difficult to see what problem Bitcoin solves for people with left-wing politics. The switch to paper money was a response to the crisis of the old gold-centered system, and Bitcoin has managed to replicate many of gold’s bugs with few of its features. Leaving aside the entrepreneurs and speculators, who are simply looking to get rich quick, the political vision of Bitcoin is of a decentralized, stateless world with competing money systems.

Competitive currencies that would end the state’s monopoly over money have long been a dream of the right. In a 1976 paper, Friedrich Hayek argued for allowing multiple currencies to circulate within individual countries; competition would lead to the use of the soundest—meaning most austerity-friendly—currency and put a check on the attempts by governments to inflate their way out of trouble. That would mean no fiscal or monetary stimulus in an economic crisis—just let things run their purgative course. In this view, the New Deal lengthened the Great Depression; had the bloodletting continued after Roosevelt’s inauguration, things would have righted themselves sooner or later. And we should have done the same in 2008 and 2009. Cryptocurrencies would be an advance over the idea of competitive currencies—improvised money systems that could challenge the state monopoly itself.

There are big reasons to think, however, that neither Bitcoin nor any of the myriad cryptocurrencies emerging online will ever pose a serious threat to the state monopoly on money. In the nineteenth century, the United States did have competing currencies: all kinds of little banks issued banknotes that often turned out to be worthless because they were accepted only within a small radius and weren’t actually backed by anything. Some Bitcoiners drag this out as a worthy precedent anyway. But Bitcoin could never establish itself as a currency in any serious way without regulation and some sort of insurance scheme, because investors and consumers would not trust substantial savings to it. But were Bitcoin to legitimate itself through regulation and become a serious money, it’s impossible to imagine that states would tolerate it for long. It would be simple to outlaw cryptocurrencies, enforcing a ban at the point of conversion from state money to cryptomoney without attempting to crack the coin’s infinitely complicated algorithm.

Bitcoiners share with other hard-money proponents a fear of inflation and financial collapse. But there is no inflation, and government money has proved far more stable than its alternatives, either gold or Bitcoin. No bank deposits were threatened during the financial crisis of 2008, because they were FDIC insured; you can’t say that about Bitcoin in its short life. But libertarians—and there are a lot of them in tech and finance, the two parents of Bitcoin—are always worrying about inflation. They worry about it the same way that hedge fund titans see talk of eliminating their tax breaks as a rerun of Nazi Germany.

But maybe I’m just bitter. I bought 0.05 bitcoin on February 5 for $39.72. As of April 24, it was worth $24.79—down 38 percent. Some bulwark against the irresponsible state.

Leave a Comment

Posted on December 22, 2017 by Doug Henwood

Bitcoin, a commentary

When this commentary was broadcast at the beginning of my radio show at noon, Pacific time, December 21, bitcoin was trading at about $15,600. It had a bad Friday, losing almost a quarter of its value, bottoming out at $11,858, before recovering to $14,267 as I’m posting this. I am not claiming cause and effect.

I’m going to indulge in a rare bit of holding forth on my own—on the topic of bitcoin. I thought of having a guest do that, but since I wrote a piece on the topic for The Nation back in 2014 (reposted here with no paywall), and have been keeping up with ever since. Some of what I’m about to say is drawn from that article, but it’s updated with material from the shimmering present.

Bitcoin, once a fairly arcane topic, is now everywhere. The market pundit Robert Prechter, who is a great psychologist of financial markets despite being a devoted follower of Ayn Rand and believing in a piece of superstition called Elliott Wave theory, once argued that in the course of a major bull market there’s something called a “point of recognition,” when the general public gets on board. That means it’s getting late in the run and it’s time for pros to think about getting out (though a serious mania can go on well after John and Jane Q get involved). It sure seems like we’re at the point with Bitcoin, whose price trajectory over the last few years resembles some of history’s great manias, like the Dutch tulip bulb frenzy of the 1630s, the South Sea bubble of the 1710s, and the U.S. stock market orgies of the 1920s and 1990s.

What is going on? Before getting into the details, I should say that money in general is not a simple topic. Most people have a good understanding of how gold, which is something of a primal money, is mined, refined, and shaped into ingots or coins. Slightly less obvious is why it has a monetary status unlike, say, platinum. But it is rare, pure, easily divisible, and has been highly cherished throughout the ages. Paper money is more complex. From 1900 through 1971, the U.S. dollar was backed by gold, meaning its value was legally defined by a certain weight of the metal. That ended in 1971, when Richard Nixon shocked the world by breaking the link to gold and allowing its value to be determined by trading in the foreign exchange markets. The dollar is valuable not because it’s as good as gold, but because you can buy goods and services produced in the U.S. with it—and, crucially, it’s the only form in which the U.S. government will accept tax payments. Among its many functions, the Federal Reserve is supposed to allow the issuance of just the right quantity of dollars—enough to keep the wheels of commerce well-greased, but not so much that things slip off the tracks in a hyperinflationary crisis.

But Bitcoin is another animal entirely. It is the first and most famous of a large and growing family of things called “cryptocurrencies.” Other family members include ethereum, ripple, dash, monero—but Bitcoin is by far the largest. The total value of existing bitcoins is now $261 billion—that’s a third bigger than the total value of Citigroup’s stock, and slightly below the value of Wells Fargo’s stock—real banks with millions of customers, making real money.

The semi-official definition of cryptocurrency is “a peer-to-peer, decentralized, digital currency whose implementation relies on the principles of cryptography to validate the transactions and generation of the currency itself.” (While that is a dense slab of prose, to be fair to the cryptoids, it wouldn’t be easy to define the dollar succinctly either.) What that all means is that bitcoin and the rest are electronic currencies—pure data entires in electronic ledgers—created and transferred by networked computers with no one in charge. The role of cryptography is not merely to guarantee the security of the transaction, but also to generate new units of the currency. New units of cryptocurrencies are “mined” by having computers solve complicated (and pointless) mathematical algorithms; once solved, a coin is created and its birth—with a digital signature guaranteeing authenticity and uniqueness—announced to the rest of the system. Every bitcoin includes a blockchain, an anonymous digital record of the unit’s transaction history. The creator earns the value of the new coin when it enters the system. You can buy or sell bitcoin on online exchanges, and there are even a few bitcoin ATMs scattered about. (The closest one to me in Brooklyn is about 2 miles away; the closest U.S. dollar ATM is at the deli half a block away.)

Mining requires enormous amounts of computing power. According to some estimates, bitcoin’s power use already may equal 3 million U.S. homes, topping the individual consumption of 159 countries. The bulk of this mining goes on in China, where most of the electricity comes from coal, so this is a dirty business. The number of bitcoin in circulation is supposed to top out at 21 million; we’re approaching 17 million now. As the limit is approached, the coin-creating algorithms get more difficult to solve, meaning more computing power is required, and more carbon is generated. Even the most seemingly immaterial of things often have deeply material roots.

I should emphasize that the algorithms used to generate bitcoin are pointless. They serve no useful purpose. To some partisans, that’s a good thing, because if they were tied to some useful purpose, that might confer some intrinsic value upon the currency; best to let its value float freely, limited only by the human imagination.

That’s the technology of Bitcoin; what about it as money? The classic economist’s definition of money is that it is a store of value, a unit of account, and a medium of exchange. You go to the store and find a can of tomatoes is priced at $3—unit of account, which the store will book as revenue when it’s sold. You take $3 out of your pocket or your debit card—you draw down the store of value (the cash on hand or in the bank), and use it as a medium of exchange. The value of the U.S. dollar is that everyone in the U.S. (and beyond) recognizes the currency as fulfilling successfully all these tests of money. The dollar is valorized by the goods and services that it can buy.

Bitcoin has serious problems in all three aspects. Over the last week alone, the value of bitcoin has varied from about $15,000 to $21,000. A year ago, it was worth just over $800. That’s not a very reliable store of value. [Note: it’s now $14,492. But wait a minute—it’ll change. Here is a live quote.]

Almost no one accepts bitcoin, nor do any businesses of note keep their books in bitcoin; it fails both as unit of account and medium of exchange. And its short history—the first bitcoins were minted in 2009—has been turbulent. There have been multiple thefts, frauds, and hackings, which partisans dismiss as growing pains. But with no regulator, no deposit insurance, and no central bank, this sort of thing is inevitable—it’s just tough luck. Introduce regulators and insurance schemes, though, and Bitcoin will lose all its anarcho-charm.

Gold is like Bitcoin in being a stateless form of money, which is why libertarians love it, but it does far better on the store of value measure. The price of gold varies by less than 1% a day—but its price is still more volatile than the much-maligned U.S. dollar. It is a semi-reliable store of value. But gold does little better on the other measures: there’s not much you can buy with it, and almost nothing is priced or accounted for in gold.

Despite that, gold retains an enormous phantasmic appeal—some “objective,” market-determined measure of value, unsullied by state intervention. Keynes called gold part of “the apparatus of conservatism.” That was an old conservatism, the conservatism of rentiers who loved austerity, because it preserved the value of their assets. Bitcoin serves a similarly totemic purpose for today’s cyberlibertarians, who love not only the statelessness of it as money, but also its power to “disrupt.” Bitcoin is part of the apparatus of anarcho-capitalism.

The political cast of the Bitcoin universe is mostly libertarian, but it has a left wing. A paper written a few years ago by Denis “Jaromil” Roio, a hacker, artist, and graduate student, deploys quotations from Michael Hardt and Antonio Negri, Giorgo Agamben, and Christian Marazzi to give Bitcoin a revolutionary spin, creatively reading it as a way for “the Multitude [to construct] its body beyond language.” He does not explain how transforming the monetary instrument will change what is produced or how incomes are distributed.

There’s something to be said for bitcoin’s anonymity—though you have to wonder how impenetrable its veil is to the National Security Agency. For now, it’s a semi-safe way to buy drugs and weapons.

But aside from anonymity—which is nothing to sneeze at!—it’s hard to see what problem Bitcoin solves. The switch to paper money was a response to the crisis of the old gold-centered system. There’s no practical value to Bitcoin—anonymity aside, again—but it does carry political baggage. Leaving aside the entrepreneurs and speculators, who are just looking to get rich, the political vision of Bitcoin is of a decentered, stateless world, with competing money systems.

Competitive money, ending the state monopoly over money, has long been a dream of the right; in a 1976 paper, Friedrich Hayek argued for allowing multiple currencies to circulated within individual countries; competition would lead to the use of the soundest—meaning most austerity-friendly—currency and put a check on governments’ attempts to inflate their way out of trouble. That would mean no fiscal or monetary stimulus in an economic crisis—just let things run their purgative course. In this view, the New Deal lengthened the Great Depression; had the bloodletting continued after Roosevelt’s inauguration, things would have righted themselves sooner or later. And we should have done the same in 2008–2009.

Cryptocurrencies would be an advance on the idea of competitive currencies—improvised currencies that could challenge the state monopoly itself. (Actually we had competing currencies in the 19th century; all kinds of little banks issued banknotes that often turned out to be worthless.) Of course, there is no inflation, and government money has proved far more stable than its alternatives, either gold or Bitcoin. No bank depositor lost a dime in the financial crisis of 2008; you can’t say that about Bitcoin in its short life. But libertarians—and there are a lot of them in tech and finance, the co-parents of Bitcoin—are always worrying about inflation; they worry about it the same way that hedge fund titans see talk of lifting their tax breaks as a rerun of Nazi Germany.

So even though Bitcoin fails as money, it’s acquired a vivid life as a speculative asset. But unlike more conventional speculative assets, its value is completely immaterial. Stocks are ultimately claims on corporate profits, and bonds are a claim on a future stream of interest payments. You can say no such thing for bitcoin. Its only value is what someone else will pay for it later today or maybe tomorrow. And now they’re trading futures on it, which takes speculation into a fourth or fifth dimension.

And what a speculative mania it is. Everyone wants to be part of the action. Bitcoin imitators are sprouting daily. The other day, speculators forked over $700 million to a company, block.one, for a cryptocurrency that doesn’t really exist and, according to its sponsors, has no purpose. The company has disclosed almost no information about itself, and almost nothing is known about its founders. And early on Thursday morning, the Long Island Ice Tea Corp., which sells nonalcoholic beverages, changed its name to Long Blockchain, and its stock price promptly more than doubled. The firm has no agreements with any cryptocurrency promoters, nor does it have prospects for any. The mere name change did the trick.

It’s all nuts, but my guess that it’s not the kind of bubble that will cause broad economic damage when it pops. For that to happen, the bubble would have had to be financed by banks that would be put at risk of failure when things fall apart. That doesn’t seem to be happening. But shirts will be lost. More seriously, this bubble shows that some people have too much money. Our society—and I mean that broadly, since a lot of the money going into bitcoin looks to be coming from Asia—has plenty of cash for speculation and not much for human need.

Share this: