Fresh audio product: professor canceled for an article, the lingering effects of the slavocracy in the South, the Confederate diaspora

Just added to my radio archive (click on date for link):

April 25, 2024 Jodi Dean talks about being suspended from teaching at Hobart and William Smith Colleges for writing an article the administration didn’t like • Keri Leigh Merritt on the lingering effects of antebellum Southern society (article here) • excerpts from an interview first broadcast in June 2023 with Samuel Bazzi, co-author of this paper, on the effects of the white migration out of the South after the Civil War on the recipient areas (from a June 2023 interview)

Fresh audio product: Yanis Varoufakis on being banned in Germany, and on the rise of technofeudalism

Just added to my radio archive (click on date for link):

April 18, 2024 Yanis Varoufakis talks about being banned in Germany for supporting the Palestinian cause, and then about the transformation he analyzes in his new book, Technofeudalism: What Killed Capitalism

Fresh audio product: the World Court, the secret history of Jelly Roll Morton

Just added to my radio archive (click on date for link):

April 11, 2024 Heidi Matthews on the World Court and the cases against Israel pending there • Elijah Wald, author of Jelly Roll Blues, on Jelly Roll Morton and the hidden history of early blues

Fresh audio product: Israel expands its war, Zionists appropriate “safety” discourse, the shipping industry and the Baltimore bridge disaster

Just added to my radio archive (click on date for link):

April 4, 2024 Trita Parsi explains why Israel is trying to expand its war to Iran and Hezbollah • Natasha Lennard analyzes the Zionist appropriation of leftish “safe space” discourse • Stefan Yong explores the structure of the global shipping industry in light of the Baltimore bridge disaster

Fresh audio product: Shoah after Gaza, valuing care work

Just added to my radio archive (click on date for link):

March 28, 2024 Pankaj Mishra, author of this article, on the propaganda-induced debasement of the Holocaust • Nancy Folbre, one of four authors of this report, on assigning a monetary value to care work

Fresh audio product: AIPAC, Schumer and ICJ in Israel, why are the youth troubled?

Just added to my radio archive (click on date for link):

March 21, 2024 David Moore on how AIPAC is using GOP contributors’ money to go after progressive Dems • Meron Rapoport on how Schumer and the ICJ are being received in Israel • Jamieson Webster on the social aspects of mental disorder among the young

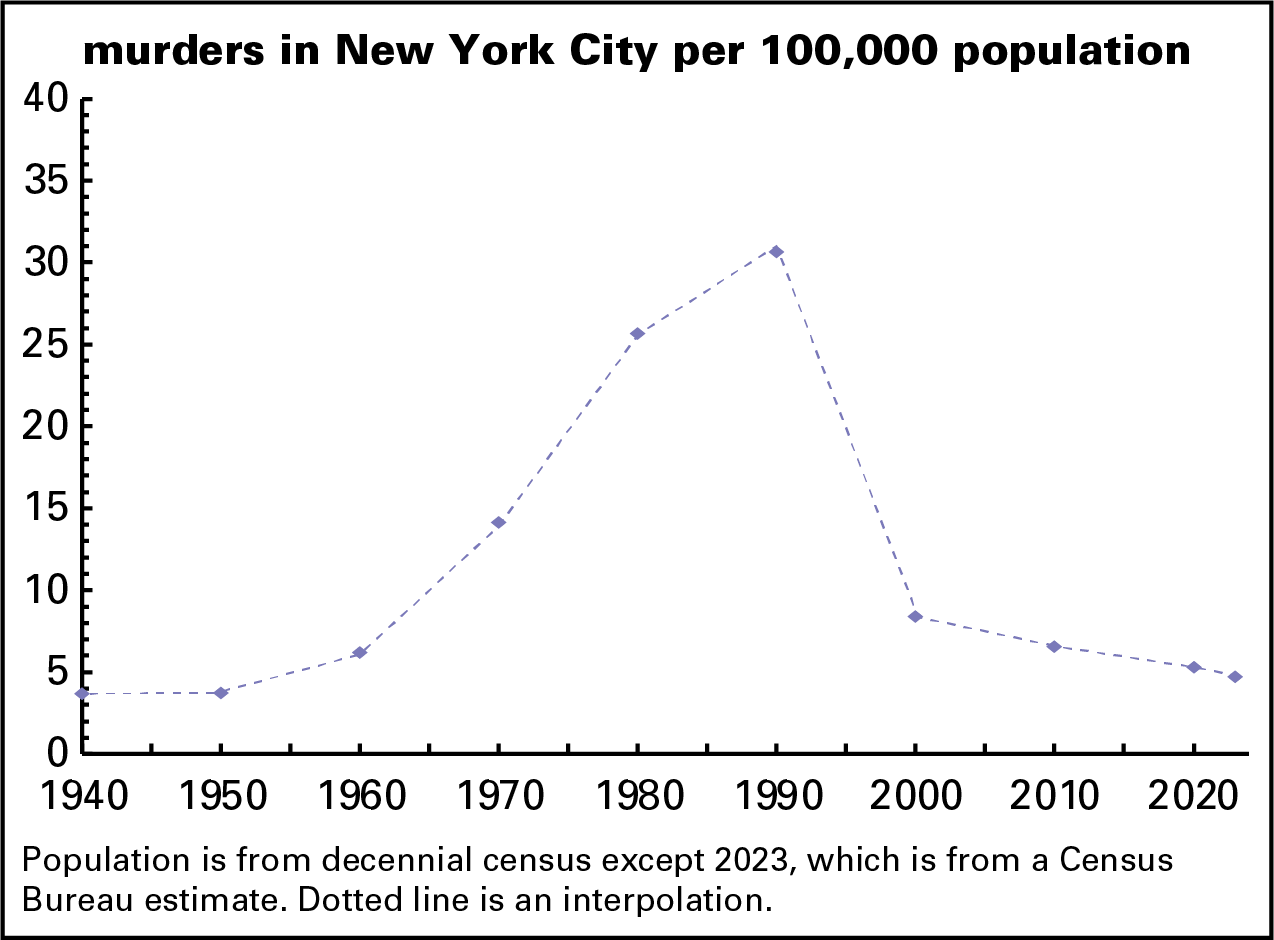

NYC is not a killing field

I have a weakness for the New York Post. Their politics are odious, but damn, they’re very skilled practitioners of the tabloid arts. Right now, though, they’re trying to convince New Yorkers—with some success, alas—that we’re in the midst of a horrid crime wave. Just as I was typing that, I got a notification from the Post on my phone reporting that four students were slashed in a fight inside a high school. The paper is tireless in its fearmongering.

In this campaign, they’re assisted by Donald Trump, who bellowed on his Truth Social platform a few months ago that “MURDERS & VIOLENT CRIME HIT UNIMAGINABLE RECORDS!” (caps in original, of course) in the city.

Fact-checking Trump and the Post are thankless tasks, but it seems worth setting the record straight. Crime is not at record levels—nowhere near it.

Let’s look at murders, the best measure to look at according to criminal justice connoisseurs for getting a sense of overall trends. Murder isn’t only the most serious crime around, the stats on homicide are also the most reliable of all, because few murders are missed and other types of crime are subject to reporting and classification errors. Here’s the history in a graph:

Last year, there were 391 murders in the city, down 11% from 2022, 20% from 2021, and 83% from the all-time peak in 1990. So far this year, murders are down 25% from the same period last year. If that rate is sustained through 2024, we’ll be back to the pre-covid lows. There is just no crime wave, but reactionaries like Trump and the Post want you to think so.

Since the city’s population has changed over the years (though not by as much as you might think), it’s worth looking at the murder rate, the number of homicides per 100,000 people. Here’s what that looks like. At just under 5 per 100,000, it’s down by 85% since the 1990 peak. It’s exceeded by cities that Trump and the Post editorialists no doubt imagine are safer, like Miami (11 per 100,000), Dallas (12), and Houston (also 12). Sad to say, NYC’s peak rate of 31 per 100,000.

Our terrible mayor, Eric Adams, could be making these points, but he doesn’t want to—he’d rather blame migrants for our problems. Besides, doing something about important things like the cost of housing or adapting to climate change might annoy the landlord class that runs the city. Better to stoke fears of our neighbors and of refugees.

Fresh audio product: chaos in Haiti, death of the future

Just added to my radio archive (click on date for link):

March 14, 2024 Robert Fatton explains Haiti’s further descent into poverty and chaos • Steve Fraser, author of this article, analyzes and mourns the death of any sense of a better future

Fresh audio product: empty Northern elites, Ukraine during and after the USSR

Just added to my radio archive (click on date for link):

March 7, 2024 Vijay Prashad on how the North American and European bourgeoisies are a spent force, with nothing to offer the world (article here) • Volodymyr Ishchenko, author of Toward the Abyss, on Ukraine during and after the USSR

Fresh audio product: Black Panthers, Pakistan

Just added to my radio archive (click on date for link):

February 29, 2024 historian Donna Murch, author of Living for the City, takes on some myths about the Black Panther Party • Saadia Toor and Rabia Mehmood on Pakistan

Fresh audio product: the Desi diaspora, finance capital today

Just added to my radio archive (click on date for link):

February 22, 2024 Jeet Heer on Indian Americans in politics and society (article here) • Stephen Maher and Scott Aquanno, authors of The Fall and Rise of American Finance, on the new finance capital

Fitch lecture: 13th annual edition, with Robin D.G. Kelley

on Monday, March 18, at LaGuardia Community College in Long Island City, Queens. Kelley, a distinguished professor of history at UCLA, is calling his talk “From the Waterfront to the Sea: Working Class Democracy and the Question of Palestine.” I’ll be doing the intro.

More info here.

on Monday, March 18, at LaGuardia Community College in Long Island City, Queens. Kelley, a distinguished professor of history at UCLA, is calling his talk “From the Waterfront to the Sea: Working Class Democracy and the Question of Palestine.” I’ll be doing the intro.

More info here.

Fresh audio product: the bankers’ club and how to bust it, the problem with immediacy

Just added to my radio archive (click on date for link):

February 15, 2024 Gerald Epstein, author of Busting the Bankers’ Club, on the finance racket and how to transform it • Anna Kornbluh, author of Immediacy, on our sped-up, unmediated cultural eternal present

Vibecession over

Though I’m certainly not the first to make this observation, it looks like the “vibecession” is over. The term was coined in June 2022 by multimedia economic analyst Kyla Scanlon (drawing on Keynes but also the poetry of Charles Bukowski), who defined it as “a disconnect between consumer sentiment and economic data. So basically, the economy is doing fine, but people are absolutely not feeling fine.” By recent measures, people are starting to feel somewhat finer, if not bounce-off-the-walls fine.

The Conference Board’s consumer confidence index rose 6.8 points in January to its highest level since December 2021. The index is the summary of a monthly survey the organization has conducted since 1967 that asks people questions about the state of the economy, the job market, and their personal finances, both in the present and their expectations for the future. Separate indexes for the present and expectations questions are computed, and then averaged into a composite. The history is graphed below.

January’s rise in the composite was led by its “present conditions” component, up 14.1 points to the highest level since March 2020. Driving the rise were improving evaluations of the job market, as the gap between those reporting “job plentiful” and those reporting them “hard to get” expanded 8.4 points to 35.7 in favor of plentiful—very high by historical standards (higher than 94% of all the months in its 57-year history). Expectations, alas, are more muted.

Gallup agrees on the improvement, though not on its degree. The present component of their economic confidence index rose to its highest level since November 2021 in January, but it’s still negative on balance. (It’s computed as the difference between the share of respondents calling the economy excellent or good and the share calling it poor. Just 5% of respondents in the January survey called it “excellent,” and 22% “good.” Far more, 45%, called it poor. for a net of -18%.) The expectations side, while also net negative, is at its least negative level since September 2021. There’s no graph of these because there are often long stretches between surveys and such a graph would be ugly.

And another: the University of Michigan’s consumer sentiment measure (graph below) was up 9.1 from December on its preliminary January reading, reaching its highest level since July 2021. It was also led by evaluations of the present, though expectations were somewhat loftier than the Conference Board’s counterpart. Sentiment had really been plumbing the depths: in June 2022, the month Scanlon coined the term, the index hit 50.0, its all-time low in over seven decades of history—below the depths of the Great Recession. Not coincidentally, it was also the month of peak inflation.* The sentiment index’s full-year 2023 average was 8 points below the long-term recession average. January’s improved reading was nonetheless still almost 10 points below the average of all business cycle expansions since 1952.

inflation down

Much of this improvement in outlook is the result of the decline in inflation, from 8.9% in June 2022 to 3.3% in December 2023, a fall of almost two-thirds. We hadn’t seen 8.9% in 42 years. December’s 3.3% is above the 1990–2019 average of 2.5%, but not profoundly so.

Along with the decline in actual inflation has come a decline in expected inflation. I’ve long thought that instruments that measure “expectations” are mostly about the present and recent past and have little or no prognostic content. (As the graph below shows, expectations for price increases over the next twelve months generally track the experience of the previous twelve.) Instead, expectations can be read as a measure of a subjective state—in this case, how established inflation feels as a part of life, what the current norm is.

By this measure, inflation’s psychological grasp looks to be slipping. As the graph shows, expectations for the next year have come down along with actual inflation, from over 5% in mid-2022 to 2.9% in January.

That matters a lot—people hate inflation! Liberals and leftists tend to dismiss inflation as a concern of anal-retentive reactionaries, but that badly misreads popular opinion. I made this argument at some length in my long Jacobin article on inflation, but here’s another piece of evidence to add to that: Scanlon cites a Morning Consult poll that found 63% of consumers prefer prices going down to their income going up. Economists natter on about “real” (inflation-adjusted) income, but they may not be giving enough weight to the price part.

partisan coda

Speaking of the Michigan sentiment numbers, the improvement in outlook over the last couple of months crosses partisan lines, but the gap between Democrats and Republicans widened. Partisan gaps have long been visible in the survey, but they were much less dramatic than they’ve been since January 21, 2017. During the Obama years, Dems’ consumer sentiment ratings were about 18 points higher than Republicans’. During the Trump years, the gap more than doubled to 39 points, though it switched parties to favor Republicans. For first three of the Biden years, the parties flipped again, as Dems’ evaluations exceeded Reps’ by 35 points, even though nothing had changed by conventional economic measures. Independents, not surprisingly, split these differences.

Between November 2023 and January 2024, both parties saw strong increases in their evaluations of the economy, but Dems, up 17 points, were more enthusiastic than Reps, up just 15. So the gap widened to 44 points.

Much of the lift to the overall sentiment measure for Republicans—over three-quarters of it—came from expectations, not evaluations of the present; perhaps they’re hopeful about November’s election results.

Otherwise, the end of the vibecession might be good news for the hapless warmonger Biden, who needs some.

* In June 2022, when the sentiment measure was at its record low of 50.0, the unemployment rate was 3.6%. It was also the high for the recent inflation surge: 8.6%. In October 2009, when the unemployment rate was 10.0%, the worst reading of the Great Recession, the sentiment index was 70.6. But there was literally no inflation: for the year ending October 2009, the consumer price index was down 0.2%.

Posted on February 8, 2024 by Doug Henwood

fresh audio product: exhausted humanity faces climate crisis, recessions raise lifespans

Just added to my radio archive (click on date for link):

February 8, 2024 Ajay Singh Chaudhary talks about his new book, The Exhausted of the Earth: Politics in a Burning World • Matt Notowidigdo, co-author of this paper, on how recessions increase life expectancy

Share this: