Corporate tax whiners

Corporate America is mad that the Inflation Reduction Act (IRA)—which may actually reduce inflationary pressures over the long term, if not now—will raise its taxes. The Financial Times has a nice collection of bleats from their trade associations:

The bill would impose “significant new tax increases and unprecedented government price controls”, the US Chamber of Commerce warned. Its tax provisions would deal “a blow to our industry’s ability to raise wages, hire workers and invest in our communities”, said the National Association of Manufacturers.

The Business Roundtable, which represents blue-chip companies in Washington, estimated that the package would impose $300bn of new costs on industry just as the economy was turning downhill.

The Chamber’s policy director Neil Bradley offered some perspective: “If 2017’s tax reforms were a 10 and Build Back Better [Biden’s original plan] was a zero, where is this? I guess I’d say it’s a five. It didn’t cut taxes; it raised taxes, but it’s a lot better than Build Back Better.”

Further perspective was provided by a UBS analyst, who, according to the FT, estimates that the IRA would impose a hit to profits for the 500 blue-chip companies that make up the S&P 500 index of about 1%. Quite the “blow” indeed.

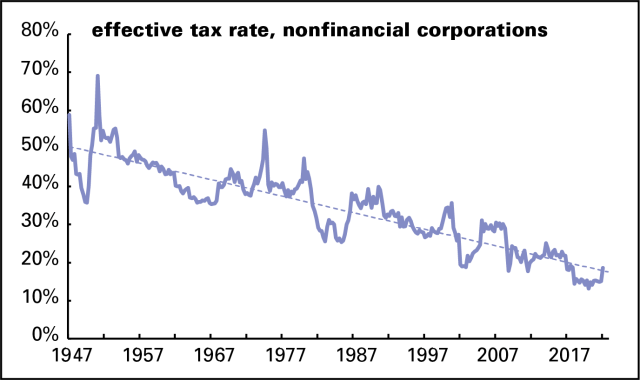

It’s worth looking at why Bradley loves 2017 so much: it brought an enormous tax cut for companies whose tax burden had already been shrinking for decades. Here’s a history of corporate taxes drawn from the national income accounts. The keepers of those accounts adjust profits to match economic reality and not what firms tell their shareholders (sometimes artificially high) or the IRS (as low as possible). As this graph shows, the effective tax rate for nonfinancial corporations—what they pay as a percentage of profits—has been declining steadily since the quarterly accounts began in 1947.

In the 1950s, the rate averaged 50%. It declined with almost every subsequent decade—to 41% in the 1970s, to 31% in the 1980s, and 26% in the 2000s. Bradley’s beloved 2017 cut took the rate from 22% in 2016 to 15% in 2018, saving companies $93 billion in taxes. The effective tax rate popped up a bit, to not quite 19%, in the first quarter of this year, but that’s still lower than any full year between 1934 and 2016.

Taking the corporate tax rate back to 1950s levels, assuming no reduction in profits, would yield almost $620 billion in revenue (not, of course, that that’s likely to happen any time soon). According to cost estimates by the Committee for a Responsible Federal Budget, no friend of social spending, that would more than cover the family benefits in the original Build Back Better (BBB) bill. Taking the effective tax rate back to the average in the first decade of this century would yield almost $200 billion, which would cover the family and medical leave provisions of BBB. Merely taking it back to 2016’s level, just before the Trump tax cuts, would yield over $120 billion, a bit more than the universal pre-K component of BBB.

But we don’t want to make Neil Bradley and his comrades sad.