Capital drought

U.S. corporations are flush with cash. As of the end of the third quarter, they had $1.8 trillion in cash, bonds, and other liquid financial assets on hand—and I’m talking about nonfinancial corporations, not banks or insurance companies. Profits are very high, and firms are gushing with cash flow. But they’re not investing all that much—in things, that is, like buildings and machines. Usually, corporate capital spending tracks closely with cash flow (profits plus depreciation allowances). Firms typically invest all their cash flow, and very often more (borrowing the difference). Over the long term, in fact, capital expenditures have slightly exceeded cash flow by 0.2% of GDP

Not lately, though. Since the economy bottomed in 2009, cash flow has exceeded real investment by 2.6% of GDP. Just as firms are reluctant to hire new workers, they’re reluctant to spend their plentiful cash on expanding operations.

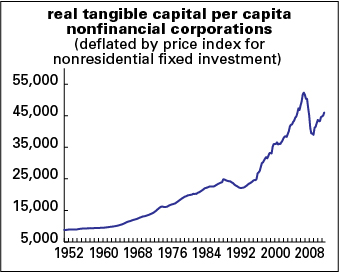

The reluctance to invest comes on top of a sharp cutback in capital spending during the recession. Along with all these numbers I’ve been quoting, the Federal Reserve, in its flow of funds accounts, provides estimates of the total capital stock—a dollar valuation of buildings and equipment owned by the corporate sector. Graphed below is the real value of that capital stock for the nonfinancial corporate sector per capita.

It fell by over 25% during the recession. It’s recovered some since, but remains about 12% below its 2007 peak. We’ve never seen a comparable pattern—sharp decline, weak recovery—since these figures began in 1952. There was a more modest decline between 1988 and 1992, but it was quickly recovered.

This weakness in the capital stock is bad for current growth—if corporations were investing all their cash flow, they’d be spending $300 billion more than they are now, which would add almost 2 points to GDP growth—but also bad for the future. Weak capital stock growth means weak productivity growth, and weak productivity growth guarantees weak income growth for the masses if it’s drawn out over the long term. (Yes, strong productivity growth doesn’t guarantee strong income growth; it could just mean higher profits and higher upper-bracket income. But low productivity growth guarantees low income growth.) According to the textbooks, high profitability and juicy cash flow should encourage investment. But they’re not. Instead, managers are hoarding their cash—the cash that they’re not shipping out to shareholders via dividends and buybacks, that is, a flow that is at near-record levels. (Things haven’t changed much on the shareholder score since this.

The managerial class loves to talk about itself as bold and risk-taking—characteristics which are supposed to justify all that money they make. But they’re being cowardly and tightfisted. What are they afraid of? Why have their animal spirits gone into hibernation?

More on this in the next issue of LBO, out next week.

High productivity growth means more output per person, fewer persons needed for the same level of output, and downsizing. Fewer people working means lower demand and a slowing economy. Fewer people working and fewer people buying will not sustain profits and there is no reason to invest in a shrinking economy but charity. Good Luck to us on that.

Capitalists do not invest for charity but for ROI.

Take away health care and non-productive finance profits and this economy is in the tank.

Lack of demand surely ?? Or do you have another take on it?

I agree. I created a petition asking the FED to use its directed lending power to support its newly affirmed goal or reducing unemployment as it did previously to bail out the banks. It can be found at: http://www.thepetitionsite.com/701/433/300/tell-the-fed-to-act-now-to-foster-economic-recovery-create-jobs-and-restart-the-housing-sector/

But if there is no present investing by the capitalists, wherefrom derives the return? I suspect that they are just waiting for things to worsen (for the rest of us) so that the imposition of a regime even more unpleasant than the present can be shoved down our throats. And that is probably the good news.

Pingback: The Real Culture War II: Utopia, Austerity and the F***** C**** « thecurrentmoment

If Helicopter Ben did actually throw money from a chopper things probably would be a helluva lot better than they are now.

Companies are hoarding cash because there are few profitable areas to invest in. Nothing complicated about it at all. There is no other reason for job creators/worker exploiters as a whole to be piling in on treasuries at zero yield.