fresh audio product: Saudi Arabia and British meltdown

Just added to my radio archive (click on date for link):

October 20, 2022 Annelle Sheline of the Quincy Institute explains why Saudi Arabia cut its oil production dramatically • James Meadway, former adviser to Jeremy Corbyn’s Labour Party and now director of the Progressive Economy Forum, explains why Britain is in economic and political crisis

Fresh audio product: Brazil elections and right-wing women leaders

Just added to my radio archive (click on date for link):

October 6, 2022 Forrest Hylton on the Brazilian elections • Dorit Geva on why women leaders are prominent on the far right these days (papers here and here)

Fresh audio product: Ukraine and abortion

Just added to my radio archive (click on date for link):

September 29, 2022 Anatol Lieven on the horror in Ukraine and diminishing chances for peace • Anne Rumberger, author of this article, on the history of the Christian right’s attitudes toward abortion (they weren’t always against it)

Fresh audio product: remembering Barbara Ehrenreich

Just added to my radio archive (click on date for link):

September 22, 2022 a memorial to Barbara Ehrenreich, who died at 81 on September 1, featuring three BtN interviews with her from 2004, 2005, and 2009

fresh audio product: child poverty, more on Chile, and the politics of grievance

Just added to my radio archive (click on date for link):

September 15, 2022 DH on child poverty: how much was it down? • another view of the Chilean constitutional referendum, this from Mario Pino • Arielle Angel, editor of Jewish Currents and author of this article, explores the problems with organizing your politics around grievance

Fresh audio product: Chilean constitution, student debt relief

Just added to my radio archive (click on date for link):

September 8, 2022 Chilean political activist Antonia Atria explains why that country’s voters rejected a proposed new constitution • Juliana Fredman, a public interest lawyer in the Bay Area, analyzes Biden’s student debt relief plan

Fresh audio product: Mark Fisher and climate austerity

Just added to my radio archive (click on date for link):

August 25, 2022 Matt Colquhoun talks about Mark Fisher on the reissue of his essay collection Ghosts of My Life, and Matt Huber, author of this review, criticizes the climate austerity camp

Underscoring the “con” in semiconductors

Well that didn’t take long.

Just nine days ago I wrote about how Washington was picking up the check for the semiconductor industry’s aggressive stock buyback programs, distributing billions in subsidies to an industry that could have funded itself if it hadn’t chosen to shower its shareholders with cash. And despite the passage of the wittily named CHIPS Act, which was supposed to encourage real investment in research and production, they’re turning the taps on the cash shower on again. The Financial Times reports:

On the same day that Congress passed the law, Intel, which is expected to be the biggest beneficiary of government grants, sliced $4bn from its capital spending plans for the rest of this year, although it said that it was still committed to a “strong and growing dividend” for its shareholders.

Meanwhile, Micron, which celebrated President Joe Biden’s signing of the legislation last week with the announcement that it planned to invest $40bn in the US by the end of the decade, was forced just a day later to say it would cut its capital spending “meaningfully” next year because of the downturn.

OK, business is slowing. But investment—in real things, not financial assets—is supposed to be governed by the long view. Clearly it isn’t. Once again, American capitalism proves that shareholder value is the most sacred value of all.

Fresh audio product: nuclear power and the Russian & Ukrainian ruling classes

Just added to my radio archive (click on date for link):

August 11, 2022 Leigh Phillips on why nuclear power has to be part of any serious decarbonization program • Volodymyr Ishchenko on Putin’s invasion of Ukraine as part of a bid to consolidate power, and how the ruling classes of both countries are political capitalists of a sort unknown in the West

Corporate tax whiners

Corporate America is mad that the Inflation Reduction Act (IRA)—which may actually reduce inflationary pressures over the long term, if not now—will raise its taxes. The Financial Times has a nice collection of bleats from their trade associations:

The bill would impose “significant new tax increases and unprecedented government price controls”, the US Chamber of Commerce warned. Its tax provisions would deal “a blow to our industry’s ability to raise wages, hire workers and invest in our communities”, said the National Association of Manufacturers.

The Business Roundtable, which represents blue-chip companies in Washington, estimated that the package would impose $300bn of new costs on industry just as the economy was turning downhill.

The Chamber’s policy director Neil Bradley offered some perspective: “If 2017’s tax reforms were a 10 and Build Back Better [Biden’s original plan] was a zero, where is this? I guess I’d say it’s a five. It didn’t cut taxes; it raised taxes, but it’s a lot better than Build Back Better.”

Further perspective was provided by a UBS analyst, who, according to the FT, estimates that the IRA would impose a hit to profits for the 500 blue-chip companies that make up the S&P 500 index of about 1%. Quite the “blow” indeed.

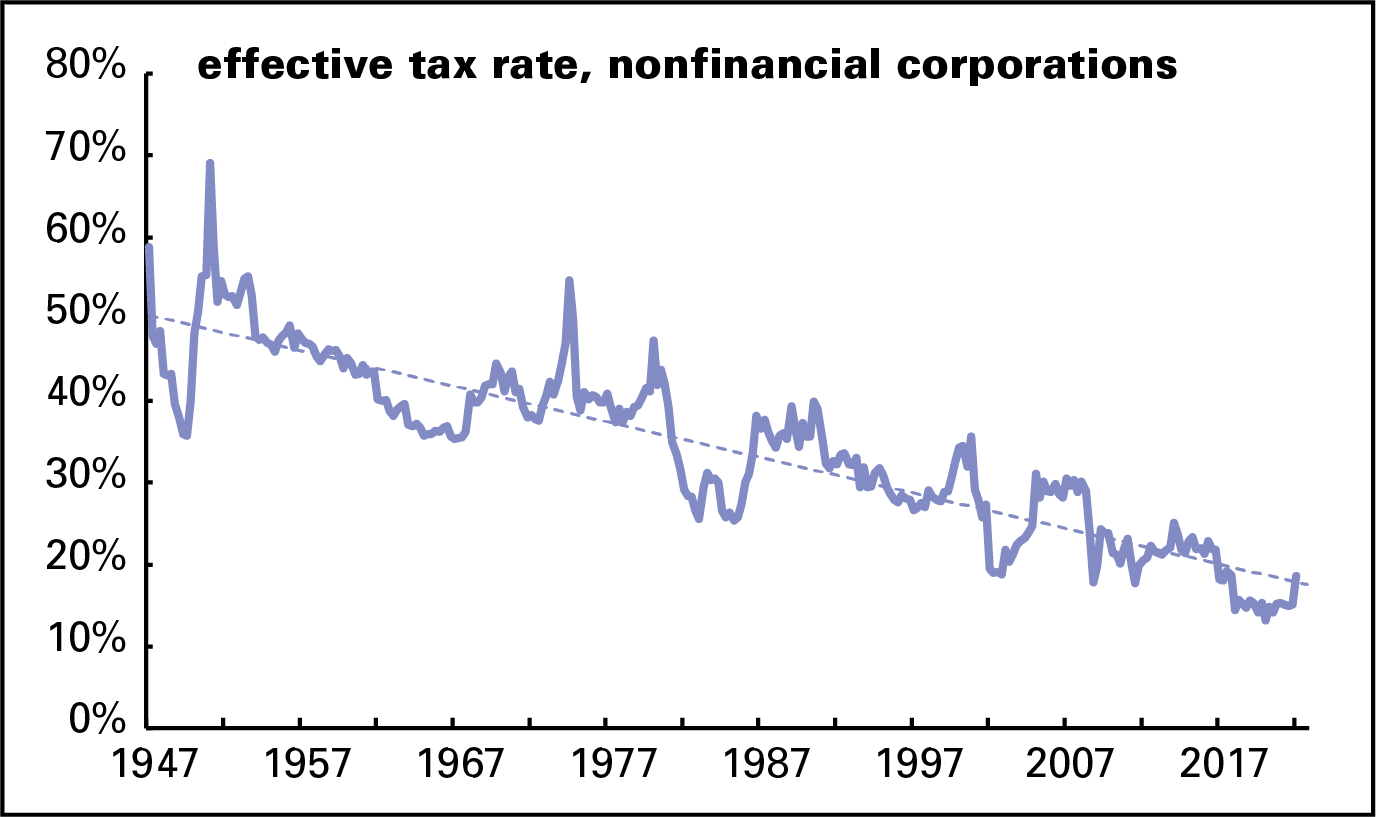

It’s worth looking at why Bradley loves 2017 so much: it brought an enormous tax cut for companies whose tax burden had already been shrinking for decades. Here’s a history of corporate taxes drawn from the national income accounts. The keepers of those accounts adjust profits to match economic reality and not what firms tell their shareholders (sometimes artificially high) or the IRS (as low as possible). As this graph shows, the effective tax rate for nonfinancial corporations—what they pay as a percentage of profits—has been declining steadily since the quarterly accounts began in 1947.

In the 1950s, the rate averaged 50%. It declined with almost every subsequent decade—to 41% in the 1970s, to 31% in the 1980s, and 26% in the 2000s. Bradley’s beloved 2017 cut took the rate from 22% in 2016 to 15% in 2018, saving companies $93 billion in taxes. The effective tax rate popped up a bit, to not quite 19%, in the first quarter of this year, but that’s still lower than any full year between 1934 and 2016.

Taking the corporate tax rate back to 1950s levels, assuming no reduction in profits, would yield almost $620 billion in revenue (not, of course, that that’s likely to happen any time soon). According to cost estimates by the Committee for a Responsible Federal Budget, no friend of social spending, that would more than cover the family benefits in the original Build Back Better (BBB) bill. Taking the effective tax rate back to the average in the first decade of this century would yield almost $200 billion, which would cover the family and medical leave provisions of BBB. Merely taking it back to 2016’s level, just before the Trump tax cuts, would yield over $120 billion, a bit more than the universal pre-K component of BBB.

But we don’t want to make Neil Bradley and his comrades sad.

Productivity stinker

In yesterday’s post about chronically low levels of investment, I concluded that they’ve “given us stagnant productivity growth and a collapsing infrastructure.” This morning, the Bureau of Labor Statistics (BLS) confirmed the productivity part. For the year ending in the second quarter, it was down 2.5%, the worst in the series’ 75-year history.

Productivity sounds like one of those things only the orthodox worry about, but it doesn’t have to be. Its most common form, labor productivity, is a measure of how much a worker can produce in an hour on the job. While that sounds conceptually simple, measuring output is no simple task; few of us are producing “widgets,” that discrete, standardized, and mythical commodity beloved of the homilies in economics textbooks. The standard way of measuring output is its “real” (inflation-adjusted) dollar value (or whatever your national currency is). That may seem like a bit of a kludge, but that’s capitalism for you—it is all ultimately about monetary values.

Output is one thing; how the proceeds of that output are divided are entirely another. Some go to wages, some go to the boss, some go to the shareholders. Over the last couple of decades, the share going to the worker has declined, from about 65% of value-added in the 1960s to around 60% today. But however those proceeds are divided, their growth puts an upper limit on the growth in incomes and with them, material well-being.

Here’s a graph of the history of productivity growth for all nonfarm businesses in the US. Since the quarter-to-quarter numbers can be very volatile, I’ve added a trendline (of the Hodrick-Prescott variety—it’s been criticized as imperfect but what isn’t in this fallen world?).

It looks awful, though the downdraft in the trendline may be partly exaggerated by the record-low reading for the most recent quarter. But if that trendline is approximately right, then the current situation is echoing that of the 1970s, a time of falling real wages and rising inflation. (Sound familiar?)

Real wage growth has been terrible lately. According to the measure published in the monthly employment reports, which excludes fringe benefits, the hourly wage has lost over 5% of its value since December 2020. The compensation measure reported along with these productivity members includes fringes, and has lost about half that much over the same period. In any case, it’s striking that in what is by most measures the tightest labor market in decades, a situation that is suppose to enhance labor’s bargaining power with capital, we’re seeing real wage declines. To put that in perspective, here’s a full history of this compensation measure. It looks awful too.

The spike in 2020 is the result not of pandemic-induced wage increases, but the job losses, both temporary and permanent, experienced by low-wage workers in food service and retail in the early lockdown phase. That drove up the average wage. As that was reversed, the average was dragged down. Those disruptions are now largely complete and the measure is back to reflecting reality (as well as any average can).

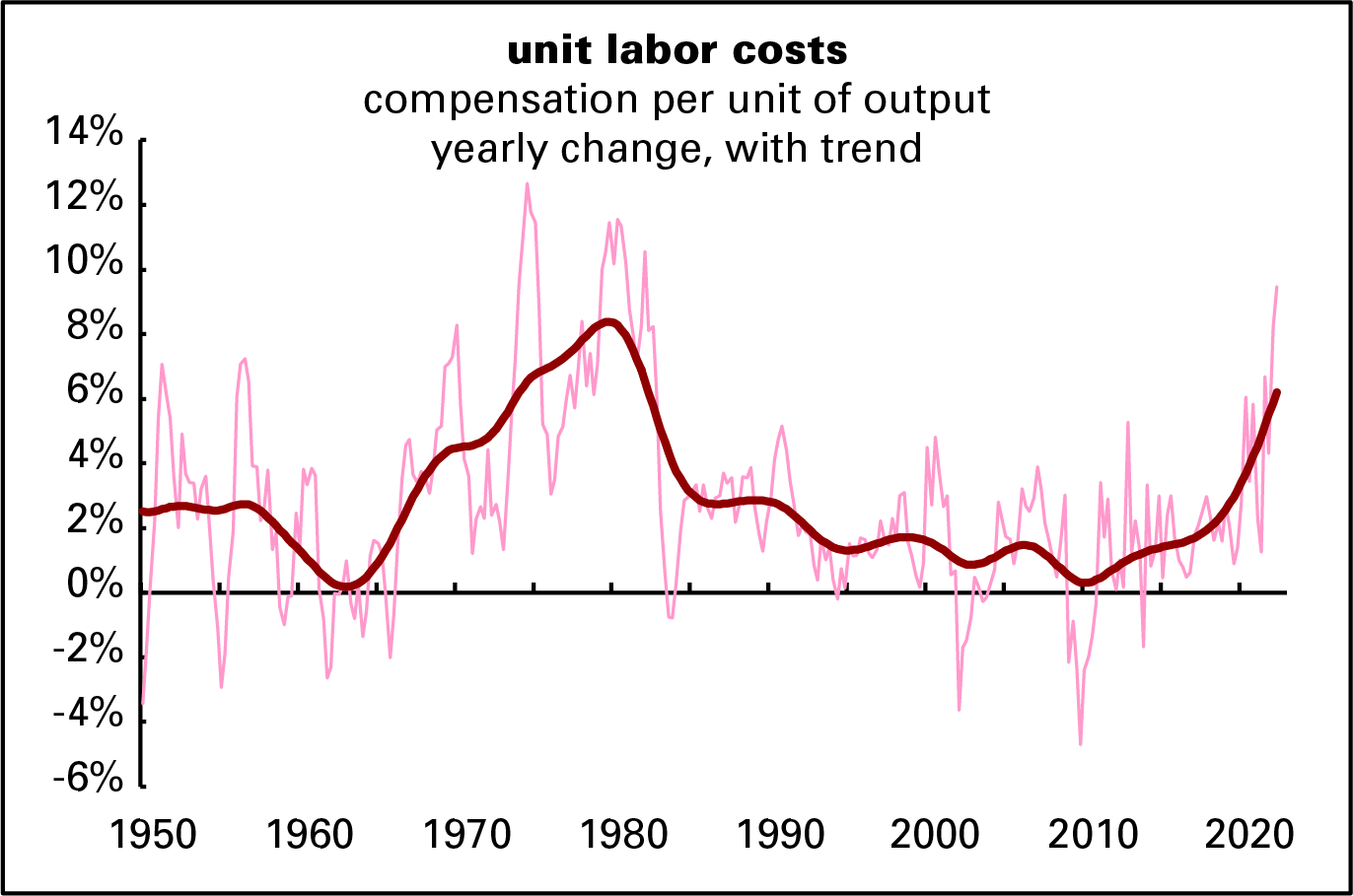

But a lot of this wage story, especially recently, is driven by inflation. Here’s a history of nominal (not adjusted for inflation) hourly compensation. Like the 1970s, the strong nominal wage gains of the last couple of years have been entirely eaten up by inflation.

As a result of strong nominal wage gains and weak productivity growth, unit labor costs—the wage costs of producing a unit of output—have been rising. Again, the only precedent for recent experience is the high-inflation years of the 1970s.

Rising unit labor costs are generally a prescription for sustained inflation. And the idea, common in some precincts of the left, that inflation is a concern mainly of the rich has no basis in fact. Rich people have been doing fine of late, while middle- and lower-income households are struggling to pay for basics.

But instead of blaming greedy workers for the inflation, as a reactionary might, I want to blame low levels of investment. For evidence, look at what happened in the late 1990s. The graphs in yesterday’s investment post show a rise in net investment in the 1990s—from 1992 to 2000, to be precise. These graphs show a sustained acceleration in both productivity and real wage growth over roughly that period—and no rise in unit labor costs. But it was the byproduct of the dot.com bubble, when for a brief time Wall Street welcomed high levels of real investment. When the bubble burst, so did financiers’ interest in boosting capital spending.

Perhaps these are just pandemic disruptions that will peter out over time. But it does seem like the management of Corporate America, and especially its shareholders, have embraced the low-investment, low-productivity model. And the payoff from that is riches for them and high inflation and declining real wages for the rest. Standard austerity programs—fiscal and monetary tightening leading to recession and unemployment—won’t address the underlying problem. An austerity program could lower inflation, but it’s not going to bring about mass prosperity. For that we need higher investment of a sort the system seems incapable of producing.

Washington will pick up the check

Semiconductor firms are about to get showered with cash thanks to a new bill, The CHIPS and Science Act of 2022—CHIPS standing for, cleverly, The CREATING HELPFUL INCENTIVES TO PRODUCE SEMICONDUCTORS Act. Because it involved free money for capitalists, 17 Republicans (out of 50) voted for it despite their habit of voting against almost anything supported by Democrats except money for the Pentagon. Biden is scheduled to sign it on Tuesday, August 9.

It’s a $280 billion package designed to encourage semiconductor manufacturing and research in the US. Pundits and generals have watched with increasing alarm as chipmaking moved from an industry dominated by the US and to a lesser extent Western Europe to a heavily Asian affair, meaning Taiwan, South Korea, and China (the big threat lurking behind all the worry, of course). The covid crisis highlighted how dependent US and European producers—carmakers, computer companies, appliance manufacturers—have become on Asian chipmakers.

The CHIPS Act is supposed to address all that, bringing the industry back home and restoring the Silicon Valley to its rightful place of global dominance. But that’s not all. When she wasn’t stoking war with China (which would require plenty of advanced chips, presumably sourced from countries other than China), Nancy Pelosi took time out to say that the CHIPS Act would create “nearly 100,000 good-paying, union jobs.” One is skeptical.

provisions

Among its provisions is $53 billion in subsidies to the US chip industry to encourage domestic R&D. Of that, $39 billion is a direct subsidy, and the rest is for “workforce development” and speeding up the “lab to fab” pipeline. The bill also includes large tax writeoffs for companies that expand chip facilities in the US, which would theoretically close the cost gap between building here and abroad. Aid won’t be confined to American firms; industry leader Taiwan Semiconductor Manufacturing Co. (TMSC) will be eligible as long as they do the work here.

The Biden administration is touting a plant Intel is building in Ohio—he even devoted 147 words to it in his State of the Union address—as proof of the CHIPS Act’s powers, but Intel has been playing politics with the project. In June, impatient with Congressional dithering on the bill, it canceled a formal groundbreaking ceremony, emphasizing that it’s building plants in countries that have gotten their subsidy act together. (Mercifully, the EU has its own Chips Act.) Intel also said its long-term plans for the site would depend on the continuing flow of free federal cash. (TSMC said its investment plans also depended on adoption of the bill.) On its passage, Intel CEO Pat Gelsinger said, “I’m excited to put shovels in the ground as Intel moves full speed ahead to start building in Ohio,” though I suspect Gelsinger himself won’t be operating any shovels. Intel may be happy, but just last month some smaller firms were complaining that it and the other giants would get all the money and they’d be frozen out.

About $200 billion will be also devoted to basic research in computing, robotics, and semiconductors through the National Science Foundation and other federal agencies. Universities getting grants under the program would be prohibiting from participating in educational partnerships with the Chinese government known as Confucius Institutes. These have been under relentless attack for nearly a decade, as the anti-China campaign ramped up.

Worries have been raised about the return of “industrial policy,” pronounced dead in the 1980s (though the Reagan administration did craft a giant aid package for the chip industry known as SEMATECH). Rather than the return of industrial policy, what’s actually distressing is watching public money go into private coffers with so little coming in return.

The CHIPS Act bars its beneficiaries from using the money to do stock buybacks or pay dividends, though it’s not clear how one set of a few billion dollars can be distinguished from another. It would also deny money to firms expanding in China and other countries deemed unfriendly. Economic warfare is ramping up.

billions in buybacks

Criticism of the bill from the left has largely focused on the quickness of US firms to expand abroad. Bernie Sanders said, “Any company who is prepared to go abroad, who has ignored the needs of the American people, will then say to the Congress, ‘Hey, if you want us to stay here, you better give us a handout.’”

He is right, though that is pretty standard practice in American capitalism. His colleague Sherrod Brown, who might have been relied on for a denunciation, likes the bill because of the Intel plant in his state, Ohio. And few Congresspeople could turn down cash for universities in their states and districts.

It was probably an oversight, but Sanders could also have pointed out how much the likely recipients have already spent on stock buybacks. It’s a small fortune.

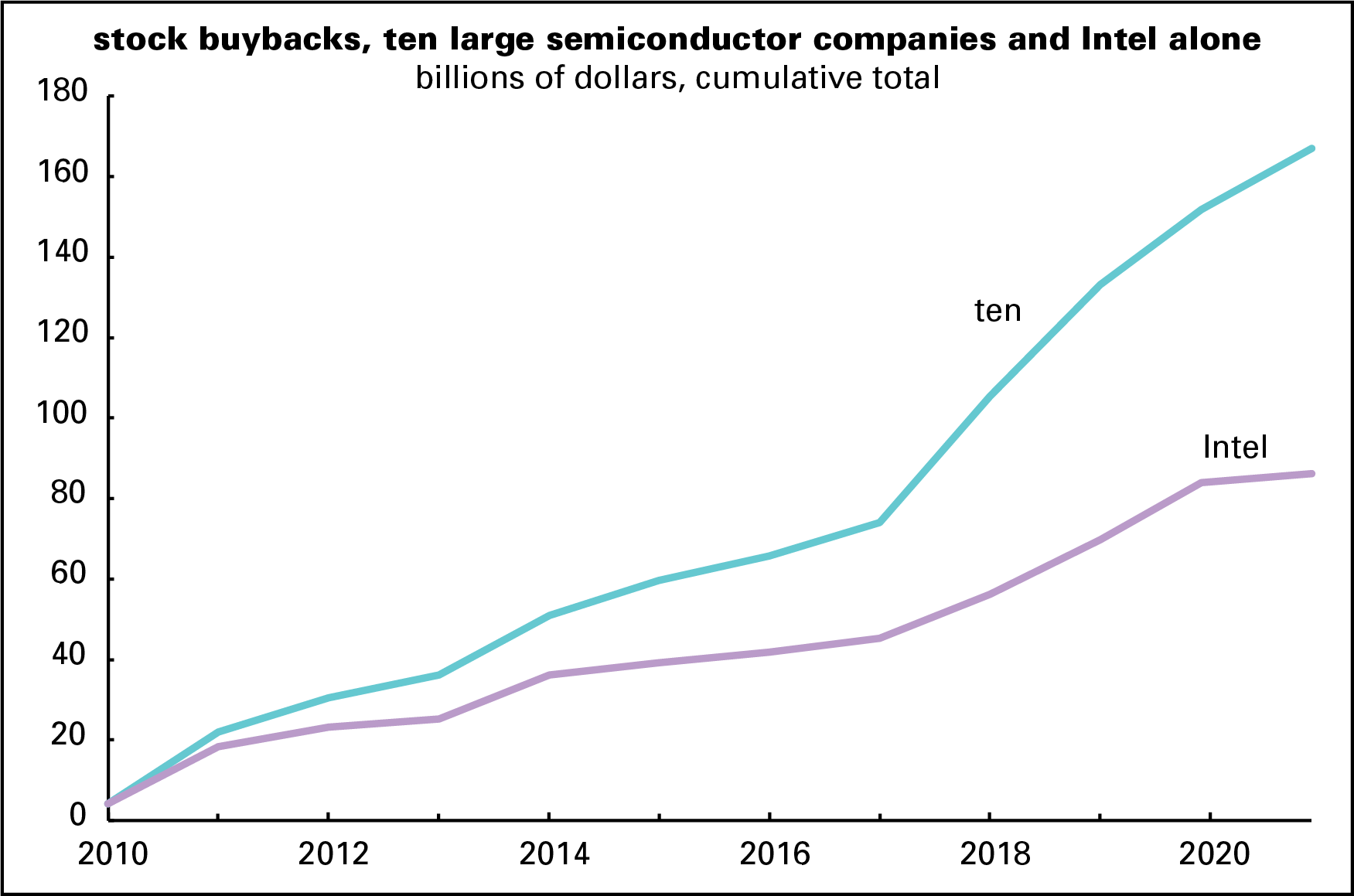

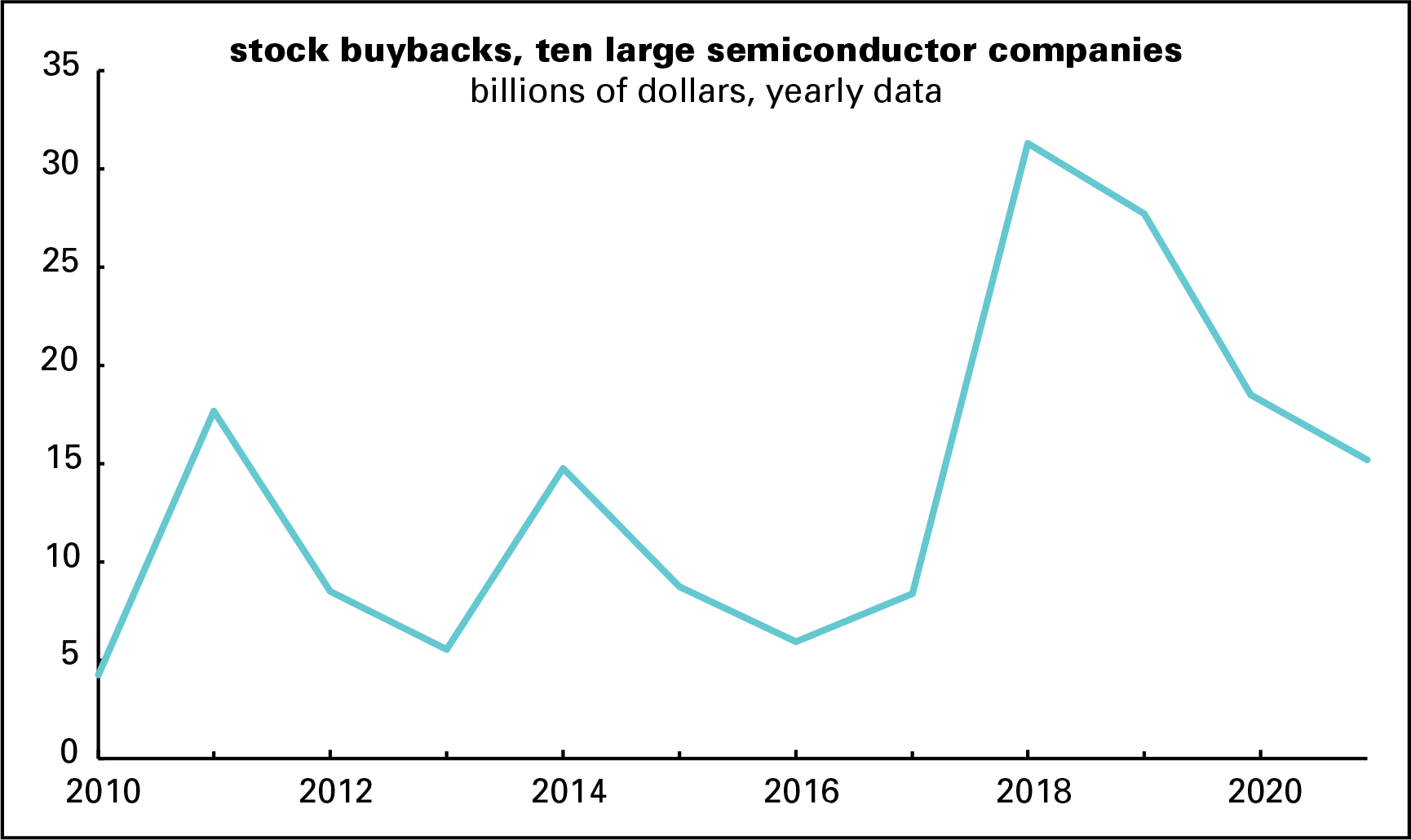

Between 2010 and 2021, ten top semiconductor firms spent $168 billion buying their own stock.* Here’s a graph of the running total of buybacks for those ten firms, and Intel, the biggest chip firm. It alone spent $86 billion over the same period. Both sums vastly exceed the $39 billion the gov is showering on the industry in direct subsidies.

As this graph shows, there was a burst of buyback activity in 2018 and 2019. Probably not coincidentally, 2017 was the year when Trump’s corporate tax cuts took effect. In theory, those were supposed to contribute to a burst of investment; they didn’t. Though the buyback pace eased after covid hit, 2021’s total was still higher than all but one year between 2010 and 2017.

Buybacks do little but boost stock prices, making stockholders happy and fattening CEO paychecks, which are largely based on stock prices. They could have invested the money, but that sort of thing is frowned upon in the higher Wall Street consciousness. Better to “return” the cash to shareholders, as they say, even though they actually provided no cash in the first place. Stockholders just buy their shares from previous stockholders, not the company.

Since Intel is so big, we also looked at its earlier buybacks, starting in 1990. That prehistory adds another $69 billion to the company’s total buying spree, taking the 31-year total up to $152 billion.

As I argue in today’s semi-companion post, the US economy has long been plagued by low and declining levels of net investment, a result of the shareholders-first doctrine of the last four decades. Fortunately for the semiconductor industry, Uncle Sam is effectively picking up the tab for its buyback spree.

* The ten firms are, in declining order of total buybacks, are Intel, Texas Instruments, Applied Materials, Broadcom, Analog Devices, NVIDIA, Micron, KLA, Marvell, and AMD.

Posted on October 17, 2022 by Doug Henwood

Comments on Half-Earth Socialism

[These are my introductory and concluding remarks for my interview with Troy Vettese and Drew Pendergrass, authors of Half-Earth Socialism.]

intro

Hello and welcome to Behind the News. My name is Doug Henwood. Just one segment today, a long interview with the Troy Vettese and Drew Pendergrass, authors of Half-Earth Socialism: A Plan to Save the Future from Extinction, Climate Change and Pandemics, published earlier this year by Verso.

In August, I had the geographer Matt Huber on the show. He was very critical of degrowth economics as an approach to climate change. Among his targets was this book. Huber’s critique attracted some hostile emails and tweets from listeners, as well as from one of the authors, Troy Vettese, who denounced Huber, me, and New Left Review, which published Huber’s critique on their blog, as “sausage socialists.” [Vettese has deleted his account, otherwise I’d provide a link.] I plead guilty; I like both sausage and socialism. Like Huber, I’m what degrowth sorts call, disparagingly, an ecomodernist, meaning I think it’s possible to reconcile a comfortable, technologically advanced life with avoiding climate catastrophe. Many hardcore greens dismiss these as “technical fixes,” as if they were some sort of underhanded trick.

Vettese and Pendergrass have a vision very different from ecomodernism. They think we should turn half the planet over to nature, a project known as rewilding, which would mean moving humans off about 40% of currently inhabited land; that the rich countries need to cut their energy use radically, fossil fuels must be kept in the ground, and nuclear power is unthinkable; and that we all have to become vegans. They imagine that this society will be run by planning, not markets, on a planetary scale.

There are some things I admire about the book. The climate crisis is dire, and weak-ass approaches won’t solve the problem. This is certainly not one of those, even if it’s not mine. It’s also nice to see some utopian thinking, and it’s even nicer to see socialists with ambitious notions of planning. But I have lots of problems with it, starting with its utopianism. Utopias are a nice way of organizing our dreams and enticing people into a political project, but a flaw in utopian thinking is that it often shows not even the vaguest plan for getting there from here. Half-Earth Socialism has a very serious case of that problem.

In one chapter of the book, they spin out a fantasy of someone who wakes up in 2047, after the half-earth revolution has triumphed. The story of how we got there (and I use “we” loosely, given my age) is rather phantasmic. There was a hurricane in the late 2020s that savaged much of the US east coast. As a desperation measure, elites tried geoengineering, sprinkling particles into the atmosphere to reduce the warming power of the sun. That was a disaster, and somehow people woke up, staged a revolution, and embraced the half-earth agenda. If you’re not going to lay out a plan for organizing this revolution, the next best thing to do, from a literary perspective, is just to write as if it happened.

The traveler from the present who wakes up in the future finds himself in western Massachusetts, an area slated for eventual depopulation and rewilding, living communally and doing lots of farm work. Boston’s population has already been greatly reduced. I have to say this life sounds more dystopian than utopian, but maybe that’s just me.

The intellectual pedigree of the book is not without problems (though I wouldn’t go so far as Lord Acton, who said “Few discoveries are more irritating than those which expose the pedigree of ideas”—good ideas can come from unlikely places). The half-earth idea comes from E.O. Wilson, who has earned considerable infamy on the left, perhaps unfairly, for his belief in sociobiology. About that, the authors say: “[Wilson] is a bogeyman for the Left because of his book Sociobiology, which naturalized sexual and cultural differences. Apart from this admittedly reactionary research programme, Wilson is a centre-Left Democrat who thinks that policy nudges and the generosity of enlightened philanthropists suffice to achieve planetary conservation.” Ok, it’s a plausible defense.

More troublesome is the role of Dave Foreman, the co-founder of Earth First! who died on September 19, in the intellectual history of rewilding: he was one of its earliest promoters. Foreman was a reactionary misanthropist who wanted to restrict immigration. In 1987, one of his Earth First! colleagues wrote in the organization’s journal that AIDS might solve the problem of overpopulation. Vettese and Pendergrass vigorously reject that side of rewilding in the book. Since Foreman died after the interview was recorded, I asked them to comment on his legacy. They wrote: “Instead of seeing over-population as the problem, environmentalists should see that capitalism has caused the environmental crisis and therefore only socialism can promise true sustainability. Yet, for this to happen, socialists must too learn to take the environmental crisis seriously and propose a form of conservation that abjures its colonial heritage.” They swear their vision could support the current human population of 8 billion, but they really don’t say how. Though I’m glad they’re not Malthusians, I wish they’d spent more time discussing population issues. Several times in the interview, when I criticize them for not having considered an issue adequately, they defend themselves by saying it’s a short book. It is, but maybe it should have been longer.

I’ll have more to say after the interview. But now I’ll let them make their case. Troy Vettese is an environmental historian and a Max Weber fellow at the European University Institute in Florence. Drew Pendergrass is a PhD student in Environmental Engineering at Harvard (which is where they met and much of the book was written). Vettese speaks first, defending himself by pleading former residence in Williamsburg, Brooklyn.

show

outro

And now I’ll exercise my host’s privilege by getting the last word here. As was clear from my introduction, I had a lot of problems with this book. I’ll list a few more.

Their style of argument is rather biased. They caricature and dismiss things they don’t like or agree with. Vettese said they had a whole section on nuclear power; it’s all of four pages. They spurn dissenting positions as “nonsense,” even those coming from credible sources like the climate scientist James Hansen (who says that nuclear power has saved almost two million lives over the last five decades, by reducing fossil fuel pollution) and the journalist George Monbiot. A lot of my listeners don’t like the pro-nuke position, but that’s not my point here and I’m not going to argue it. Instead of responding to arguments like these, Vettese and Pendergrass banish them, citing only sources that support them as if they were the last word on the topic. That approach no doubt pleases the crowd, but these are complex and controversial issues, and their approach is no way to advance the argument.

But it’s not just nuclear power. Geoengineering is far more controversial even among mainstream experts than their account allows; you can find serious reservations coming out of Harvard, which they portray as the strategy’s Vatican, and the Brookings Institution, an establishment source if there ever was one. An article published by Yale’s environmental program opens by saying geoengineering has to be taken seriously, given the magnitude of the climate problem, but then pivots to its dangers, and suggests large-scale reforestation as a safer alternative. I’m not denying that the scheme has its advocates, but there’s nothing like the elite consensus the Half-Earthers describe. Or direct air carbon capture, an approach of sucking large amounts of carbon out of the atmosphere that’s still in its infancy—when I pointed to lots of young technologies in the field (and who knows if they’ll work out? venture capitalists are not immune to chasing chimeras), Vettese responded by saying we’ve been talking about it for twenty years and it’s still not feasible. Computers were massive, hugely expensive, and slow as molasses twenty years after they were first deployed too. Pendergrass is more thoughtful, but he presents the challenges facing the technology as if they’re immutable, and as if proponents were unaware of them.

As I complained in the interview, they mostly consider mainstream approaches only to dismiss them, rather than engaging with them seriously. I say this not out of any love for mainstream sources, but because they’re not always wrong, and in any case, deserving of serious refutation, given their power and resources. The IPCC, which is made up of some of the world’s most distinguished environmental scientists, thinks other approaches would work, but Vettese and Pendergrass don’t say much about why they’re wrong. They don’t even give a full picture of some of the research they draw on. I quoted the conclusion of a paper by Christian Peters et al., which they cite in the book in support of their fervent veganism: “Carrying capacity was generally higher for scenarios with less meat and highest for the lacto-vegetarian diet. However, the carrying capacity of the vegan diet was lower than two of the healthy omnivore diet scenarios.” As you may have noticed, Pendergrass ignored this and answered a question of his own invention, and then pivoted to “cutting down the amount of meat,” which is not veganism, but which sounds entirely sensible to me for many reasons. (Personally, I adhere to a Leninist strategy on meat: better fewer but better, as he said of party members.) Vettese’s dismissal of the unpopularity of veganism by saying socialism too would poll poorly is belied by actual polls. A Gallup poll from last year had its approval at 38%; an Axios/Momentive poll, also from last year, had it at 41%. That’s a lot different from the poll showing that only about 2% of Americans don’t eat animal products, and 84% of vegetarians and vegans abandon their diet. Like it or not, this is a serious obstacle to their agenda.

There’s something coercive about their rhetorical strategy: if you don’t like our utopia, the alternative is doom. Other options are ruled out, almost by executive order.

I’ll grant them this: the book is a conversation starter. But their vision is seriously lacking in political promise. Given the severity of the problem, we need to find some more appealing approaches.

Share this: