Bloomberg sheds a tear for bankers, makes up bogus numbers

Asked to comment on the Occupy Wall Street protests, plutocrat Mayor Michael Bloomberg—#12 on the Forbes 400, net worth almost $20 billion—painted a heart-rending portrait of suffering bankers:

The protesters are protesting against people who make $40-50,000 a year and are struggling to make ends meet. That’s the bottom line.Those are the people that work on Wall Street or on the finance sector.

We need to be nice to them, Bloomberg continued, so they’ll make loans and help the economy recover. No need to dwell on the past—let’s move forward.

Fact-checking the Mayor, who is far from a stupid or ignorant man: According to the Bureau of Economic Analysis, the agency that produces the GDP statistics, the average salary in the finance and insurance sector was $88,118 last year. In the “securities, commodity contracts, and investments” sector, which is what people mean when they say “Wall Street,” the average salary was $204,539. That’s four times the national average. Struggling indeed.

(The ThinkProgress reporter in the linked article only got some spotty and misleading numbers. For the BEA originals, go here: U.S. Bureau of Economic Analysis. Click on the “Begin using the data” button, choose section 6, and then choose table 6.6D. There’s no direct link to that table, thus the roundabout route.)

Shaking a fist at the NYPD

There was a demonstration this afternoon organized by my friends Penny Lewis and Alex Vitale, among others, in front of NYPD headquarters to object to the nasty treatment of the Occupy Wall Street protesters and years of repression of dissent in what was once a rambunctious city. (Here’s the event’s Facebook page.) Since Giuliani and continuing through Bloomberg, the cops have used “quality of life” pretexts—keep the traffic moving!—to limit marches. And they’ve spied on organizers, arrested protesters en masse, and generally made peaceful dissent very difficult. The fact that a senior cop was videotaped pepper-spraying penned-in people who’d done nothing violent now seems to have the force on the defensive, thank god. But the longer the OWS protest goes on, the risk of more brutality rises.

When I got there, about a half hour after scheduled starting time, Penny was addressing a small crowd.

It was a spirited gathering, and Penny was terrific, but I was a little worried that the demo would turn out to be an anticlimax. Still, the cops were ready—on the ground

and in the air.

Any gathering in New York is guaranteed to have an aerial audience like this—there were at least three helicopters hovering overhead.

But then there was kerfuffle at the entrance to Police Plaza (through the Manhattan Municipal Building, a borough hall on a rather grand scale). People began chanting “Let them in.” I was too far away to see if the police were blocking the way, but if they were, they didn’t for long as a large throng of reinforcements came in from the main OWS site at Zuccotti Park.

Soon, Police Plaza was filled with a giant, noisy crowd. This is what the area where the white-shirted cops were standing in the photo above looked like about seven minutes after that photo was taken.

(That’s Rev. Billy with the preacherly pose in the center, and Greg Grandin, the Latin America scholar at NYU, in the green shirt, front right.)

Still, despite the size of the crowd, and the fact that there was no permit for the demo, the cops just stood back. There was a line of them in front of the entrance to police HQ, but they just stood around. Earlier, they’d looked a bit taken aback by the influx. Who knows what they’ll do if all this continues, but for now, free speech had the upper hand in lower Manhattan.

There were union signs and the usual crop of protest slogans, but there was also one odd image crafted presumably by a critic of quantitative easing:

But that was just an amusing curiosity. The overwhelming tone was spirited, determined, and thoroughly inspiring. As I’ve said before, who knows where this is going, but right now it’s exciting. It didn’t hurt that this particular demo had a very clear message—stop beating people and let people speak freely. But with the original OWS encampment persisting, and cities across the country joining in, I thought of Wallace Stevens’ line about searching “a possible for its possibleness.”

The Occupy Wall Street non-agenda

I’m not here to disparage Occupy Wall Street; I admire the tenacity and nerve of the occupiers, and hope it grows. But I’m both curious and frustrated by the inability of the organizers, whoever they are exactly, or the participants, an endlessly shifting population, to say clearly and succinctly why they’re there. Yes, I know that certain liberals are using that to malign the protesters. I’m not. I desperately hope that something comes of this. But there’s a serious problem with this speechlessness.

Certainly the location of the protest is a statement, but when it comes to words, there’s a strange silence—or prolixity, which in this case, amounts to pretty much the same thing. Why can’t they say something like this? “These gangsters have too much money. They wrecked the economy, got bailed out, and are back to business as usual. We need jobs, schools, health care, and clean energy. Let’s take their money to pay for them.” The potential constituency for that agenda is huge.

Why instead do we see sprawling things like this (A Message From Occupied Wall Street), eleven demands, each identified as the one demand? Or this: The demand is a process? A process that includes this voting ritual: Select Below and Vote to Include in the Official Demands for #Occupy Wall Street.

Why the emphasis on multiplicity and process? I think it’s a living instance of a problem that Jodi Dean identified last November—a paralysis of the will, though one disguised as a set of principles:

Once the New Left delegitimized the old one, it made political will into an offense, a crime with all sorts of different elements:

- taking the place or speaking for another (the crime of representation);

- obscuring other crimes and harms (the crime of exclusion);

- judging, condemning, and failing to acknowledge the large terrain of complicating factors necessarily disrupting simple notions of agency (the crime of dogmatism);

- employing dangerous totalizing fantasies that posit an end of history and lead to genocidal adventurism (the crime of utopianism or, as Mark Fisher so persuasively demonstrates, of adopting a fundamentally irrational and unrealistic stance, of failing to concede to the reality of capitalism).

An agenda—and an organization, and some kind of leadership that could speak and be spoken to—would violate these rules. Distilling things down to a simple set of demands would be hierarchical, and commit a crime of exclusion. Having an organization with some sort of leadership would force some to speak for others, the crime of representation.

But without those things, as Jodi says, there can be no politics. “It is instead an ethics. Is it any surprise, then, that under neoliberalism ostensible leftists spend countless hours and pages and keystrokes elaborating ethics? The ethics of this or the ethics of that, fundamentally personal and individual approaches that obscure and deny the systems and structures in which they are embedded?”

Occupiers: I love you, I’m glad you’re there, the people I talked to were inspiring—but you really have to move beyond this. Neoliberalism couldn’t ask for a less threatening kind of dissent.

1930s phantasms from the right: how to make up stories with numbers

Economists Harold Cole and Lee Ohanian have a piece in the Wall Street Journal that deserves a prize for the devious use of statistics. They want to argue that fiscal stimulus is bad, and the New Deal only made the Depression worse. This is a familiar argument on the right—and I even heard it once from a Marxist economist—but it’s just not true.

Here’s the prize-eligible statement:

But boosting aggregate demand did not end the Great Depression. After the initial stock market crash of 1929 and subsequent economic plunge, a recovery began in the summer of 1932, well before the New Deal. The Federal Reserve Board’s Index of Industrial production rose nearly 50% between the Depression’s trough of July 1932 and June 1933. This was a period of significant deflation. Inflation began after June 1933, following the demise of the gold standard. Despite higher aggregate demand, industrial production was roughly flat over the following year.

Here’s a graph of the Fed’s industrial production index for the period:

Crucial months are marked. July 1932 is the phantasmic trough of the recession named by Cole and Ohanian. Note that there was little recovery at all in industrial production between July and March 1933—the official Depression trough, so designated by the arbiter of these things, the National Bureau of Economic Research. March 1933 also the month that Roosevelt took office and declared a bank holiday, ending a four-year run on the banks. A month later, he severed the dollar’s link to gold and made it clear that the U.S. government was determined to put an end to deflation. Though the alphabet soup of New Deal programs was yet to come, the break with previous orthodox economic policy was clear. And industrial production began a sharp recovery.

August 1936 [note: I’d originally, and wrongly, said April 1936] is marked because that’s when the Fed began to double reserve requirements for banks, a policy move that Milton Friedman indicted for causing the relapse of Depression in 1937. (Though widely accepted, that argument has been disputed in a paper by Charles Calomiris et al, but that’s not relevant to the politics of this, given Friedman’s right-wing credentials.) Keynesians have also pointed to a marked tightening of fiscal policy, announced in 1936, for the return to slump.

In other words, stimulus worked as advertised, and so did austerity.

Cole and Ohanian grudgingly concede that unemployment declined between 1933 and 1937, but they don’t let on by how much. Here’s the history, from the NBER (official BLS monthly unemployment stats don’t begin until 1948):

The unemployment rate fell by more than half between the May 1933 peak (two months after FDR took office) and the July 1937 low. They want to minimize this, but a decline of that magnitude is remarkable.

They also want to minimize the broad economic recovery that occurred in the mid-1930s. But real GDP rose 30% between 1933 and 1937, an average of almost 7% a year. Again, nothing to sneeze at.

As Irving Fisher wrote in his classic paper, “The Debt-Deflation Theory of Great Depressions”:

Those who imagine that Roosevelt’s avowed reflation is not the cause of our recovery but that we had “reached the bottom anyway” are very much mistaken…. According to all the evidence, debt and deflation, which had wrought havoc up to March 4, 1933, were then stronger than ever, and let alone would have wreaked greater wreckage than ever, after March 4. Had no “artificial respiration” been applied, we would soon have seen general bankruptcies of the mortgage guarantee companies, savings banks, life insurance companies, railways, municipalities, and states. By that time the Federal Government would probably have become unable to pay its bills without resort to the printing press, which would itself have been a very belated and unfortunate case of artificial respiration. If even then our rulers should still have insisted on “leaving recovery to nature” and should still have refused to inflate in any way, should vainly have tried to balance the budget and discharge more government employees, to raise taxes, to float, or try to float, more loans, they would soon have ceased to be our rulers. For we would have insolvency of our national government itself, and probably some form of political revolution without waiting for the next legal election.

If you think stimulus is a bad idea, make that argument. But don’t make up stuff about the past.

Visiting the occupiers of Wall Street

Occupying Wall Street

We—my wife Liza Featherstone and son Ivan Henwood and I—paid a visit to the Occupy Wall Street protest yesterday afternoon. Here’s an illustrated report. I also did a segment for my radio show. Audio for that is at the bottom of this entry.

The big media have largely ignored the OWS protest (though if you’re part of a certain kind of network on Facebook, you can’t miss it). Called first by Adbusters with only the most minimal agenda, it’s taking on a life of its own, as people trickle in from all over. And I do mean minimal—the agenda is supposed to evolve spontaneously. When I talked with one of the organizers last week, she told me that they merely hoped “to build the new inside the shell of the old,” and though that sounds seductively wonderful, I’m not sure how robust such an approach can really be.

Or, to quote the event’s Facebook page, named in the now-ubiquitous hashtag fashion (#OCCUPYWALLSTREET):

we zero in on what our one demand will be, a demand that awakens the imagination and, if achieved, would propel us toward the radical democracy of the future

I don’t think that has Lloyd Blankfein trembling in his shoes. Not that I know what could make him tremble, aside from a few quarterly losses for Goldman.

When we got to Wall Street, a band of what appeared to be several hundred were conducting the “closing bell” march, joining in the traditional observation of the end of the trading day on the New York Stock Exchange. The dominant chant was: “Banks got bailed out, we got sold out.” Here’s glimpse of what it looked like, from the corner where George Washington was inaugurated for the first time.

It’s not often you see a quote from Ronald Reagan at an event like this, but the politics of the participants looked like a mixed bag, a topic I’ll return to.

This being New York, a healthy contingent of cops was on the scene.

At the corner of Wall and Broadway, things dispersed some, with some of the crowd (including us) heading towards the base camp, Zuccotti Park at the corner of Broadway and Liberty, not far from the “Freedom Tower” (under construction). Here’s what the park looked like from the Broadway side.

Within, one quickly encountered familiar iconography, e.g., this U.S. flag with corporate logos in place of the stars (photo by Ivan Henwood).

Posters promoting the event, exhibiting that Adbusters style that’s a reminder that Judith Butler was so right to say that you have to inhabit what you parody.

The crowd was a mix of locals and migrants. I chatted with people who’d come from Missouri and Maine to express frustration and show solidarity. (They’re on the audio segment.) The woman from Maine was unemployed for a year and willing to stay as long as anyone else is there—through January, if that’s what it takes. But I also talked with locals from Brooklyn and Queens. Onlookers and passers-by were neutral to friendly—there were no jeers except some aimed for a lone and odious anti-Semite.

A celebrity local: the original pie-wielding Yippie Aron “Pieman” Kay.

Principles were being worked on in standard “consensus” fashion, which apparently means writing comments on pages taped to a wall. (The type is readable if you click on the pix to enlarge them.)

“Vauge” indeed.

Signs were being made constantly.

I asked the guy who made the “utopian experiments” sign what he had in mind. (The interview is on the audio segment.) He said he wanted to see a rebirth of 1960s-style “intentional communities,” though more entrepreneurial this time, capable of supporting themselves through green business and cyberschemes. Aside from this apostle of green entrepreneuriship, I overheard others talking about how Wall Street stifled small business—as if small business didn’t pay worse and support more right-wing politicians than big business. It was a very mixed bag ideologically. It seems like the latest iteration of American populism, which hates Wall Street and internationalization but loves small business and the local. Of course, livestreaming the proceedings on the web (see here) depends on a huge technical infrastructure, but no one thinks about that at these events.

I was skeptical of this at first, and I still am. There’s no agenda at all. It’s mostly about process—meaning consensus. There’s no organization to speak of. But maybe people will just keep trickling in and it will grow and persist and something good could come of it. Word is that some buses will be coming in from Wisconsin soon. At some point, though, I fear the NYPD will stop putting up with a semi-permanent occupation of a small park. I hope not. But if you’re listening to this, and are in a position to head to lower Manhattan, check it out. Zuccotti Park, at the corner of Broadway and Liberty St.

Give the NYPD something to watch.

Here’s the report on the event from my radio show. For the full show, click here. This is just a six-minute excerpt.

Occupy Wall Street: audio report

All photos by Doug Henwood except the corporate logo flag, by Ivan Henwood.

The housing boom (cont.)

Matt Yglesias responded, sort of, to my comments (“Was there a housing boom? Yes.”) from yesterday, countering his curious assertion that there was no building boom in the mid-2000s, by conceding that there was a boom in construction employment after all. But he refuses to give up on the argument that there was no building boom. A few more words on this topic before laying it to rest.

Yglesias graphs construction employment as a percentage of the civilian labor force with a line marking the average:

Before proceeding, a little overview to the employment stats. (No doubt CAP has a generous research budget, so if they want to send along a tuition check on their fellow’s behalf, that would be dandy.) Yglesias seems not to know that there are two surveys behind the monthly employment figures—one of about 60,000 households and one of about 300,000 employers (known as the establishment or payroll survey). He’s dividing construction employment from the establishment survey by the civilian labor force from the household survey. That’s unusual. The reason that the two surveys are rarely combined this way is that the concepts underlying the two are significantly different. The definition of employment in the household survey includes agricultural workers and the self-employed, who are not counted in the payroll survey.

Even odder is the use of the labor force as the denominator, since it includes the unemployed as well as the employed. (The labor force consists of those who are working or actively looking for work. The first set are the employed; the second, the officially unemployed. The unemployment rate is the number of unemployed divided by the labor force.) It would make more sense to use total employment as the denominator, but not the household version. My analysis yesterday took construction employment as a share of total employment from the establishment survey, which is the right way to go about this.

All that geekiness aside, Yglesias’ graph does show a marked elevation around 2005–2006. When I reproduce his numbers, I see construction employment as a share of the civilian labor force peaking at 5.4% in the spring of 2006, which is more than 20% above its long-term average. It also stayed above that average for 138 consecutive months, easily eclipsing the previous record of 75 consecutive months in the late 1960s/early 1970s. (And it was a lot further above average in the recent period than it was 40 years earlier, too.) His commentary doesn’t acknowledge the extent of the employment boom, but at least he walks back his earlier assertion, as they say in DC.

But he just won’t give up on the claim that there was no building boom, and grasps instead at remodeling. To reprise a couple of points from yesterday’s post: 1) As a share of GDP, residential investment—that is, the building of new houses and work done on older ones—hit a peak of almost 60% above its long-term trend in the mid-00s. And, 2) between 2001 and 2006, residential investment accounted for 12% of GDP growth, twice its share of the economy. If “60%” and “twice” don’t sound like big numbers, then I don’t know what does.

The Bureau of Labor Statistics also reports finer detail on construction employment (from the establishment survey), though data for most of the subcategories begins rather recently, making long-term comparisons impossible. Still, residential construction as a share of total employment peaked at 24% above its long-term average in 2006 (it’s now 30% below). Single-family contractors peaked at almost 30% above average; it’s now almost 40% below. And residential remodeling peaked at about 25% it average; it’s still slightly above that average now. A lot of the boom in mortgage debt mid-decade came from people borrowing against their inflated home equity values and using the proceeds to spiff up the kitchen or add a wing to the house. But clearly there was a lot of new building going on—much of it McMansions and other bloated structures, whose size is missed in a simple tally of starts.

Finally, the four major housing bubble states—Arizona, California, Florida, and Nevada—saw their total employment rise by 9% from the 2003 trough to the peak in 2007; the other 46 states gained just 6%. And the Bubble Four got hammered in the recession, with employment falling by almost 10%, compared with just over 5% for the other 46. The Bubble Four contributed 35% of the employment loss during the recession, nearly twice their 19% share of employment going into the downturn. The housing bubble had a lot of spillover effects, notably the use of home equity lines of credit to pay for everything from wide-screen TVs to dental work. But the direct effects of the building boom were considerable—as are those of the building bust.

Does productivity = unemployment?

There’s a controversy aflame in the left–liberal blogosphere around a revelation in Ron Suskind’s new (and apparently error-riddled) book, Confidence Men. (Brad DeLong has the page.) Suskind reports on tense high-level meetings within the Obama administration as it became clear that the StimPak wasn’t really working. Unemployment was drifting higher, and the Keynesian faction—Christina Romer, then chair of the Council of Economic Advisors, and later Lawrence Summers, then resident wise man—was calling for more stimulus. Obama said no. It was politically impossible, but Obama also argued that the productivity revolution has made workers obsolete. Against that, a few hundred bill in further stimulus—which would be DOA in Congress in any case—would do little.

Romer and Summers (who, it hurts to say, has been looking pretty good recently) argued that productivity need not create unemployment. After Obama supported an orthodox briefing by former OMB head (and inexplicable sexpot to some) Peter Orzag (who also recently said that we need less democracy to have a sensible fiscal policy), Romer objected, urging a more expansive fiscal policy. Obama cut her down in what Suskind calls “an uncharacteristic tirade.” A few months later, with unemployment now over 10%, Summers essentially made Romer’s earlier argument, and Obama listened “respectfully.” After the meeting, Romer said to Summers, “Larry, I don’t think I’ve ever liked you so much.” He told her that the feeling would pass—but then noted that Obama had been a lot more “generous” with him than her. When you’re on the wrong side of Larry Summers on feminist issues, you’ve got a serious problem.

Matt Yglesias assures us that his conversations with administration officials report that Summers and Romer won the productivity=unemployment argument eventually, and convinced him that the problem was low demand, not high productivity. But Yglesias himself also reports on an interview that Obama gave in June in which he blamed ATMs for high unemployment. And airport self-check-ins too. Stuff like that, that any globetrotter sees. So apparently Obama still believes that there’s only so much gov can do because all these business geniuses are using machines so cleverly.

Respectable Keynesians argue that the problem is demand, which is a cyclical argument more or less, while the productivity story is more structural. But maybe both sides are right in a way. Productivity is way up but wages are flat. Workers have seen little of the productivity revolution.

The canonical tech-driven productivity acceleration took hold around 1995. From then until the cyclical peak year of 2007, productivity growth averaged 2.6% a year—4.3% in manufacturing. Compensation, which includes fringe benefits (see graphic caption), rose 1.7% a year—and 1.5% in manufacturing. Direct pay overall rose 0.9% a year—0.3% for factory toilers. During the recession, productivity growth slowed, employment collapsed, and wages rose modestly. In the “recovery years” of 2010 and 2011, productivity growth—this time not from a tech revolution but from sweating a shrunken workforce harder—has resumed growing at a 2.6% pace (2.1% is the very long-term average, by the way). But both compensation and direct pay have fallen by an average of 0.3% a year.

If workers were paid better, there wouldn’t be so much of a demand problem, would there? But then we stumble upon a contradiction: the entire recovery in corporate profitability that began in 1982 came from squeezing wages and workers. The trajectory of profit expansion is very uplifting—returns are roughly double what they were in the early 1980s:

After the profitability collapse of the 1970s, things began to turn around as the Volcker recession and the PATCO firing transformed capital–labor relations. Corporations enjoyed dramatically improving returns from the early 1980s through the late 1990s. Profitability took a major hit in the early 2000s recession, with the bursting of the tech bubble, but it recovered, only to stumble again in the 2007–2009 recession. But it’s staged a remarkable recovery. In the second quarter, nonfinancial firms were more profitable than they were at any time since 1997, in the frenzy of the dot.com moment.

For most of the last 30 years, much of the working class was able to borrow what it wasn’t earning to make ends meet. Household debt rose strongly:

Mortgage debt rose from 41% of after-tax income in 1983 to 100% at the 2007 peak. It’s since come down hard, and the economy and political mood show it. Consumer credit—auto loans and credit cards and such—went from 16% to 25%. It’s come down too.

So here’s the demand problem: there’s no longer an endless supply of easy credit to make up what’s not in the paycheck. The greatest product of the productivity revolution is the production of profits, which has enabled a vast upward distribution of income and wealth. No one really wants to touch that one. So what’s a capitalist order under no serious political challenge to do except dither and squabble?

Was there a housing boom? Yes.

Matt Yglesias, striking that contrarian tone beloved of bloggers (something you’d never find here, of course!), declares that there was no housing boom. Or, more precisely, though there was a boom in house prices, there was no boom in construction.

To make this point, Yglesias uses one on those ubiquitous St. Louis Fed graphs, this one of the history of housing starts since 1970. Sure enough, it sorta supports his point.

But this is only a very partial view. Here’s a fuller one.

First of all, the boom wasn’t just about new houses—there was a lot of renovation and expansion of existing housing stock. That sort of thing, as well as new construction, is included in the category residential fixed investment in the national income accounts. As the graph below shows, this rose strongly in the late 1990s and early 2000s:

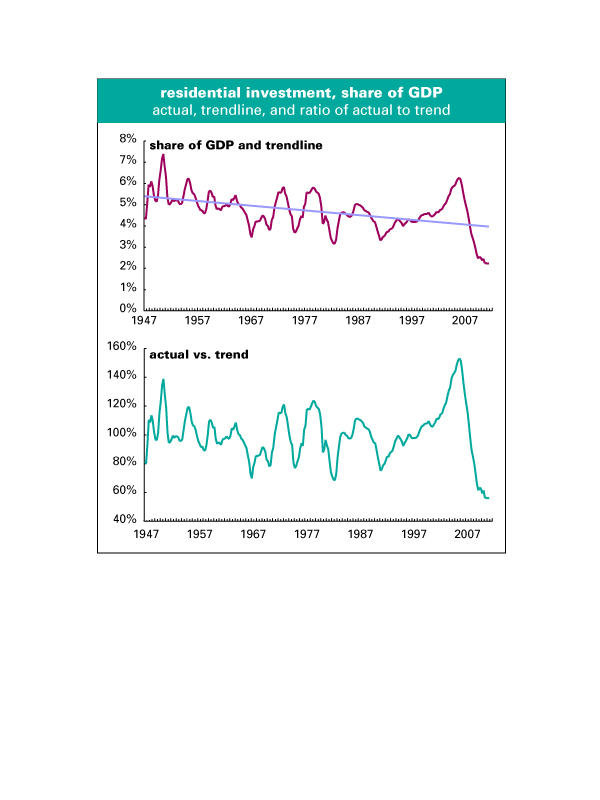

But note the blue trendline on the upper graph: housing’s share of the economy, despite cyclical ups and downs, has been in a steady decline since the highs of the early post-World War II years. The late 90s/early 00s boom was a sharp departure from that downtrend. The lower graph shows the relationship of the actual level to that underlying trend—when it’s above the 100% level (dotted horizontal line), it’s above trend. At the peak in 2005, the housing share of GDP was almost 60% above trend, a record by a comfortable margin. It was also above that trendline for a long time—from 1998 to 2007. Most earlier soujourns above trend were less than half that long. It’s since fallen dramatically, to almost 50% below trend, and it’s likely to stay there for some time.

Construction’s share of employment tells a similar story—

—that is, a declining trend from the mid-1950s through the mid-1990s, followed by a long spike, and then collapse. At the peak in 2006, construction’s share of total employment came close to matching its all-time high, set in 1956, during the post-World War II building boom.

And finally, this boom came despite a low level of household formation among those aged 25–44. The boom in younger household formation in the 1950s and 1960s drove that building boom. But this time around, the building wasn’t to accommodate a population bulge, but to satisfy a lust for more space, often far from town. Between 1973 and 2007, the size of the average house increased by almost 50%, while average household size fell by 15%.

So yes, there was a building boom. Between 2001 and housing’s 2006 peak, residential investment accounted for 12% of GDP growth, twice its share of the economy. And it’s led the way down, too. And it’s helping to keep us here.

Fitch memorial this Sunday

A reminder that the memorial to the wonderful Bob Fitch, who died in March (my remembrance of him is here), is this Sunday, 4–6 PM, at the Brecht Forum, 451 West St (between Bank & Bethune), Manhattan.

New radio product

Freshly posted to my radio archives:

September 10, 2011 Mike Lofgren, former Congressional staffer and author of this spirited farewell to his long-time party, describes the furious insanity of the GOP • Jonathan Kay, author of Among the Truthers, and Kathy Olmsted, UC–Davis prof and author of Real Enemies: Conspiracy Theories and American Democracy, on conspiriacism, esp the 9/11 kind

Me on Al Jazzera English

I’m going to be on Al Jazeera English around 9 AM New York time discussing Obama’s jobs plan, such as it is.

Watch here.

Me & Graeber on the TV this weekend

A reminder: my chat with David Graeber about his new book, Book TV this weekend:

- Saturday, September 3rd at 12pm (ET)

- Saturday, September 3rd at 7pm (ET)

- Monday, September 5th at 7am (ET)

New radio product

Just added to my radio archives:

September 3, 2011 David Cay Johnston on how corps and the megarich get away with paying almost no taxes (his Reuters column on GE is here) • Adolph Reed on the Dems, the inflated threat of the Tea Party, and the diminishing usefulness of race as a political category

New radio product

Just posted to my radio archive:

August 27, 2011 Mark Brenner, director of Labor Notes, reflects on the state of labor as Labor Day approaches • Alexander Cockburn, occasional Nation columnist and co-editor of Counterpunch, on the media and the media criticism racket

Graeber & me on the TV

My interview of/conversation with David Graeber about his book Debt: The First 5,000 Years will be on C-SPAN 2’s BookTV on Saturday, September 3 at noon and 7 PM and again on Monday, September 5, at 7 AM.

Here’s the C-SPAN page: Debt: The First 5,000 Years – Book TV.

{kind=link}