Tough, Shorty

Economics proves that tall people deserve more:

Andreas Schick, Richard H. Steckel

NBER Working Paper No. 16570

Issued in December 2010Taller workers receive a substantial wage premium. Studies extending back to the middle of the last century attribute the premium to non-cognitive abilities, which are associated with stature and rewarded in the labor market. More recent research argues that cognitive abilities explain the stature-wage relationship. This paper reconciles the competing views by recognizing that net nutrition, a major determinant of adult height, is integral to our cognitive and non-cognitive development. Using data from Britain’s National Childhood Development Study (NCDS), we show that taller children have higher average cognitive and non-cognitive test scores, and that each aptitude accounts for a substantial and roughly equal portion of the stature premium. Together these abilities explain why taller people have higher wages.

New radio product

Freshly posted to my radio archives:

January 15, 2011 Mark Ames, author of Going Postal and editor of The Exiled, on Tucson and how the U.S. is like a decaying Russia • Jefferson Cowie, author of Stayin’ Alive: The 1970s and the Last Days of the Working Class, on the politics of that unfairly maligned decade

New radio product

freshly posted to my Radio archives

January 8, 2011 (return after holiday reruns) Tyson Slocum of Public Citizen on the state of energy and climate politics in DC • Lucia Green-Weiskel, author of this Nation piece, on Cancún and Chinese energy and climate politics

New radio product

Freshly posted to my radio archives:

December 18, 2010 Lucas Zeise, columnist with Financial Times Deutschland, on why Germany is taking such a hard line on the eurocrisis • Jodi Dean, keeper of the I Cite blog and author of Blog Theory, on what digital culture is doing to our minds, our politics, and our society

The Jodi Dean interview is unusually good stuff. Consider this a twisting of your arm.

I want to live on their planet

This just in from the right-wing PR machine (quirky capitalization and word breaks in original):

“President Obama has done more favors, more often, for organized labor than any other president, outpacing even FDR and Harry Truman in the lightning speed with which he has rushed to fulfill the union agenda. Calling Obama pro-union is putting it mildly.”

Fred Barnes starts off his latest article in the weekly standard with that scorching comment. Despite not being able to convince Congress to rob workers of their right to a secret ballot, Obama continues to force his Big Labor agenda on the American public by abusing his executive powers. Stacking the NLRB to vote in favor of Big Labor, as well as his constant and vocal support of union bosses are just the tip of the ice berg.

Luckily, the American public remains constantly vigilant, as shown by the resounding defeat Big Labor suffered in a recent Delta Airlines election. Katie Gage, executive director of the Workforce Fairness Institute, has been out on the front lines making sure the public is aware of Obama’s backhanded dealings and able to defend themselves from forced unionization. Would you like to have Katie on your show?

Thanks

Mike

Mike MamassianCRC Public Relations

Really, what planet do Fred, Mike, and Katie live on?

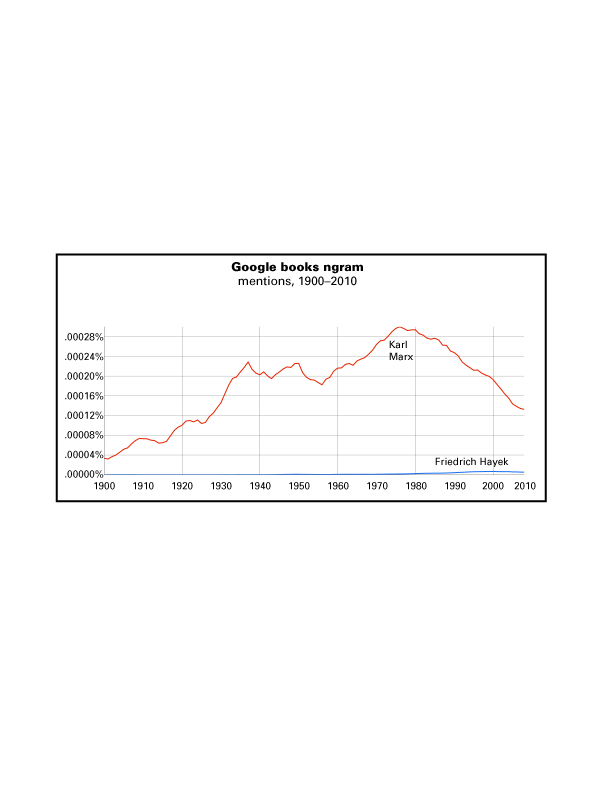

Marx crushes Hayek

Yeah, everyone’s ngram-ing, so why not me? The number of mentions of Karl Marx vs. Friedrich Hayek in a sample of the books in Google’s database. The original Google chart doesn’t scale nicely, so I’ve retouched it some using Adobe Illustrator. But the relative trajectories are unchanged. To see the Google original, click here: Marx vs. Hayek.

They just can’t stop talking about the Old Man, can they? He’s come down some since the mid-1970s, but you’d think that Freddie would have come up a lot more.

BHO, community organizer

Maybe there really is something to Obama’s background as a community organizer after all.

For some reason, I picked Saul Alinsky’s Rules for Radicals off the shelf a little while ago. I got the book years ago, when I thought I might write a piece on the unfortunate influence of Alinsky and community organizing on the American left, but abandoned the project because I couldn’t bear to read Alinsky’s prose. But as it happens, I opened to this passage, titled “Compromise,” on p. 59:

[T]o the organizer, compromise is a key and beautiful word. It is always present in the pragmatics of operation. It is making the deal, getting that vital breather, usually the victory. If you start with nothing, demand 100 per cent, then compromise for 30 per cent, you’re 30 per cent ahead….

I don’t want to enable the liberal trope of “too willing to compromise” about Obama—he’s about 40% conservative, which that critique overlooks. But add on 30% from the compromise, and he’s at 70%.

Music news: Akon’s No Labels anthem

Wow, this is some serious crap:

It only took one conversation with Lisa Borders, one of the founding leaders of No Labels, for Akon to immediately understand the meaning of this movement’s message. Never give up your label, just put it aside to do what’s best for America. With lyrics like “See a man with a blue tie, see a man with a red tie; so how about we tie ourselves together and get it done,” Akon shares his passion for politicians to put the labels aside so we can find practical solutions to our nation’s problems. Akon stayed up all night to create this song and now you can listen to it for free and share the song to help inspire others to put their labels aside.

Hard times all around

From a WSJ article on the shrinkage of Wall Street’s bonus pool this year: “Jonathan Beckett, CEO of yacht brokerage firm Burgess, said demand for weekly yacht rentals in the Caribbean this winter is ‘quite poor,’ in part because of Wall Street.” Lamborghini sales are down too, alas.

Tom Hayden doesn’t like that letter

Tom Hayden didn’t like that open letter to him et al. His response—sent to John Halle, organizer of the letter, but not as I erroneously said at first addressed to him in the polite “Dear John” salutational sense—follows. (The subject heading of the email was, inexplicably, “Weirdness.”) Gotta say, this is a beaut: “I supported Barack Obama for president in 2008, and am glad I did so. At the time I also said progressives should disagree with him on Afghanistan, NAFTA, global warming and Wall Street….” Well, what’s left to support, Cde Hayden?

So I started reading this letter which sounded pretty good and it looked like I signed it, so I read further and discovered that it was to as a member of a group I didn’t know I belonged to called the “Left Establishment.” As I kept reading, it was a vile, toxic diatribe ending with a demand that I, along with the rest of the “Left Establishment”, endorse a demonstration this week in Washington featuring civil disobedience at the White House fence.

To whomever sent the letter, I have to say I’m sorry that I just don’t respond positively to nasty invitations. I hope you can understand. Calm down and tell me who you are before the conspiracy theories mushroom.

Actually, I thought the Dec. 16 action seemed somewhat justifiable in light of current events – the WikiLeaks releases and erupting divisions within the Democratic Party. And I love the people who plan to get arrested. Maybe a big crowd will show up, but not because it was a smart idea to begin with. Mid-December is not the best time to turn out masses of people. But stuff happens, and now many people are boiling.

My personal best to those who are being arrested. They include a former Pentagon official, former CIA agent, a former New York Times reporter, and a mother who lost a son to war and was radicalized as a result. The lesson for me is that people can change from hawks to doves, from spies to whistleblowers, if organizers organize and events reshape their perceptions. That’s the lesson of WikiLeaks, that folk on the inside sometimes come find their situation intolerable and break away from old thinking.

Civil disobedience is a moral expression, and can be a personal healing. Sometimes it ignites a larger movement, or inspires other individuals to step up. We need more of it.

But I also think we need an outside/inside strategy that shifts public opinion more and more against the war. We need to persuade the undecided, not simply to create images of dissent. The peace movement will grow steadily in the months ahead, on its own, but also in its relation to other compelling causes, among them: Wall Street regulation, clean energy/green jobs, and the steady shift towards an unfettered market philosophy over our lives. Civil disobedience can light a flame, but the case for thoroughgoing radical reform must be made on our streets, our workplaces, our religious institutions, and yes, within the Democratic Party – whose overwhelming majority support progressive objectives. Members of the Progressive Democrats of America, and the Congressional Progressive Caucus, are vital elements of our movement.

I would like every person who signed this letter to read it again, and be kind enough to retract their signatures or explain why.

This is not the time to inflict internal damage on a community which is already weak enough. It’s important to get a grip.

The peace and justice community is a fragile form of social ecology, with diversity being an essential quality. Everyone is entitled to a different approach, but there also is an essential unity that can be achieved, unless a malign force is introduced.

I have been working every day since 2002 to end these wars. I will never stop. I supported Barack Obama for president in 2008, and am glad I did so. At the time I also said progressives should disagree with him on Afghanistan, NAFTA, global warming and Wall Street, and I have pursued progressive alternatives every day. I have been so busy on the WikiLeaks crisis since August that I just haven’t had time to drop by the White House and pick up my marching orders.

TOM HAYDEN

Director

Peace and Justice Resource Center

Protest Obama

I’m one of initial signers of this open letter to the left–liberals who enthusiastically supported Barack Obama in 2008, and said many silly things about him back then. Please read and then, if you agree, add your name to the growing list of endorsers.

Here’s an unintentional endorsement: Tom Hayden, one of the addressees, denounced the suggestion that he protest Obama as “vile” and “toxic,” and damaging to the “fragile social ecology” required for the growth of the peace movement. What a strange view of politics—give the imperial warriors free rein, because criticizing them might impede opposition.

Wikileaks: a CIA-Mossad project

My god, there is just no end to lunacy.

I just learned from contested terrain (which cited my comment that the Wikileaks affair proved the conspiracy theory of history to be wrong) that Wayne Madsen thinks (“CIA, Mossad and Soros behind Wikileaks”) that Julian Assange is a CIA agent in the pay of George Soros, with some help from the Mossad. So all that chat about how the woman who accused Assange of some variety of sexual assault is herself a CIA agent—well, forget that. Because Langley is pulling Assange’s strings. And why would Langley want to do that? “To play into fears” of something or other.

No wonder James J. Angleton liked that Eliot quote about the “wilderness of mirrors” so much. Except he really was a CIA agent.

Bill Gates, business genius?

Reading Diane Ravtich’s excellent takedown of (private school grad and college dropout) Bill Gates for his interventions in public education reminded me that the only reason people listen to him is that he’s thought to be some sort of business genius (as if business genius were translatable to pedagogy or anything else). If he’s that rich, he must be smart, eh? But he’s really not such a business genius.

Well, he’s a business genius of a sort, but not of the sort of heroic entrepreneur that’s usually lionized. His first foray into code-writing was a version of BASIC for some early hobbyist machines (written with fellow future megabillionaire Paul Allen). BASIC was originally developed at Dartmouth, a nonprofit educational institution, but Gates was learning how to take the work of others and turn it into his own property.

What really made him rich was having been in the right place at the right time in 1981 when IBM needed an operating system for its new PC. Gates (with Allen) borrowed heavily, to put it gently, from an existing operating system, Digital Research’s CP/M. (For DR’s version of this history—“Microsoft paid Seattle Software Works for an unauthorized clone of CP/M, and Microsoft licensed this clone to IBM”—see here. A less biased, though still damning, look is here.) In other words, another instance of adopting someone else’s work and taking credit for it—this time with the innovation of litigating aggressively and manipulating markets to defend a monopoly position. Because once it secured that monopoly, Microsoft did everything it could to crush competition.

Having secured that early market dominance with MS-DOS, Microsoft became a money machine. It earned monopoly profits with almost no cost of production. But after that, aside from Office, Microsoft has been unable to launch a truly successful product on its own creative juices. Windows—at first, a gussied up version of MS-DOS—was basically lifted from the Mac OS (which Apple itself had lifted from Xerox) and it took years before they got it right. Many Windows releases have been extremely buggy and bloated. Explorer is a crummy browser. Microsoft’s efforts on the web, Hotmail and Bing and the rest, have been disappointing. Their attempt to imitate the iPod, Zune, is a joke. Microsoft has lost money on videogames, despite the enormous growth in that market.

(Some numbers to back that up, from Microsoft’s latest annual report. The profit margin—operating profits as a percentage of sales—on Windows is around 70%. On Office, it’s 63%. Then the numbers fall hard. Entertainment, mainly the Xbox and Zune, has an 8% margin. And the online division, mainly Bing and MSN, lost more money than it took in in revenue.)

So it’s pretty rich for Gates to criticize monopoly and stodginess in public education, given this business history. His father was, among other things, an intellectual property lawyer, which did teach him something about gaining advantage in a world where the innovation of others can threaten monopoly profits. (The University of Washington law school’s Center for Advanced Study & Research on Intellectual Property is headquartered in a building named after Gates Sr.) But there’s nothing terribly admirable about using litigation and market power to become a billionaire. And that sort of personal and business history certainly doesn’t give you the credential to hold forth on education policy.

Clarification on anti-Semitism

I asked here (An apology) why the evil financiers are almost always Jews. This prompted an email from someone saying that it sounded like anti-Semitism. It was most certainly not. It was an ironic (and apparently not successfully so) question about how conspiracy types so often flirt (or worse) with anti-Semitism. Also, a lot of populist critiques of finance traffic in covert or overt anti-Semitism. I should resurrect an old polemic on that topic and post it here soon. Sorry if there was any misunderstanding.

{kind=link}

12 Comments

Posted on January 15, 2011 by Doug Henwood

Radio commentary, January 15, 2011

Against civility

The horrendous shootings in Tuscon have certainly inspired a lot of drivel from the commentariat. They were heartbreaking, but please let’s not draw stupid conclusions from them.

Perhaps most annoying has been the call for a return to civility. Well, no, I don’t feel like being civil. I like being rude. The problem with the rudeness in American political discourse is that it’s often so stupid, not that it’s so rude. The idea that politics can be civil is a fantasy for elite technocrats and the well-heeled. I’m reminded of something that Adolph Reed once said to me, characterizing a mutual acquaintance as the kind of person who thinks that if you could just get all the smart people together on Martha’s Vineyard, they could solve all our social problems. Obviously they couldn’t.

Margaret Atwood once wrote that politics is about “power: who’s got it, who wants it, how it operates; in a word, who’s allowed to do what to whom, who gets what from whom, who gets away with it and how.” There’s no way that could be rendered civil. The field of politics is constituted by vast differences in interests and preferences. Much of the time, we don’t talk about those things directly or explicitly. We talk about them in caricature or euphemism, or take it out on scapegoats.

Some on the so-called left, such as it is, are using Obama’s speech in Tuscon the other day as an excuse for rediscovering their crush on him. On The Nation’s website, always a rich source for high-mindedness, John Nichols wrote this (Don’t Tone It Down, Tone It Up: Make Debate “Worthy of Those We Have Lost”):

Really, John, when was this nation ever innocent? When we were trading in slaves and killing Indians? What act of “healing” will make this nation less divided? The rich and powerful have a lot of money and might and they’re not going to give it up easily.

Elsewhere on The Nation website, Ari Berman actually used the phrase “better angels” to characterize the pres’s rhetorical targets (In Arizona, Obama Appeals to Our Better Angels). (Uh-oh, I said targets.) This reminded me of Alexander Cockburn’s great characterization of the role of the mainstream pundit: “to fire volley after volley of cliché into the densely packed prejudices of his readers.” But clearly it’s not just the mainstream pundit—so too alternapundits. It’s not just that these stock phrases grate on the ears—their use is a symptom that their speaker is evading some complexities.

Share this: